How Much Can a Retail Bank Owner Make? $55M Year 1 Profit Capacity

This estimates retail bank owner compensation and bank owner distributions from a five-year US retail bank income model Based on the provided assumptions, earning assets grow from $160M in Year 1 to $1825B in Year 5, with pre-provision, pre-tax profit capacity moving from about $55M to about $874M before credit losses, taxes, full staffing, capital retention, and dividends

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it excludes licensing, tax structuring, deposit insurance approval, and guaranteed returns.

Want the Retail Bank model view?

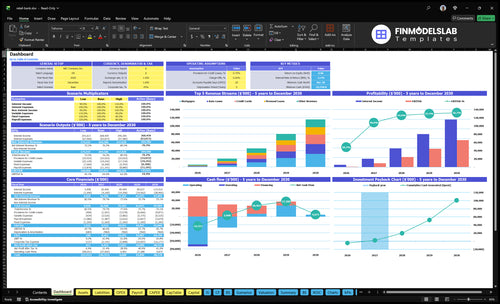

This screenshot shows dashboard, deposit-assumptions, loan-portfolio, interest income/expense, and owner-income cases in the Retail Bank Financial Model Template. Open it.

Owner-income model highlights

Earning assets: $160M-$1,825B

Net interest income: $91M-$987M

Overhead: $105k monthly

Variable expense: 190% to 75%

Planning tool only

Not dividends or approval

How does net interest margin impact bank profits?

For a Retail Bank, net interest margin (NIM), the spread between loan yield and funding cost, is the main profit driver, and a small change can swing cash hard; see How Much Does It Cost To Open And Launch Your Retail Bank Business? for the setup side. In the model, NIM is about 57% in Year 1 and 54% in Year 5, and with $1,825B in earning assets, a 0.50% move is about $91M before taxes and reserves. Loan pricing, deposit competition, borrowed funds at 50%, fraud, payroll, and technology can all cut owner take-home.

What drives NIM

Raise loan yield, keep credit tight

Pay less for deposits and borrowed funds

Watch funding mix every month

Price for spread, not volume alone

What squeezes profit

Deposit competition lifts funding cost

Fraud and payroll hit margin fast

Technology spend lowers take-home cash

Small margin drops can mean $91M

How much deposit base does a retail bank need?

A Retail Bank doesn’t need deposits by themselves; it needs enough low-cost deposits to fund loans and other earning assets safely. In your model, deposits excluding borrowed funds rise from $80M in Year 1 to $145B in Year 5, while loans rise from $100M to $15B and total earning assets rise from $160M to $1825B. Profit comes from earning asset yield, funding cost, fee income, credit losses, and fixed compliance overhead, not deposits alone.

Deposit base

$80M deposits in Year 1

$145B deposits in Year 5

$100M loans in Year 1

$15B loans in Year 5

Profit drivers

$160M to $1825B earning assets

Yield on earning assets

Funding cost on deposits

Credit losses and compliance overhead

Can retail bank owners take profits out?

Yes, Retail Bank owners can take profits out, but only after the bank earns profit and keeps capital, reserves, and liquidity inside the bank. The base model shows $55M Year 1 pre-provision pre-tax profit capacity, but What Is The Current Growth Trend Of Customer Acquisition For Your Retail Bank? matters because growth can raise funding needs before cash is distributable.

What owners can take

Pay owner salary for active work

Declare dividends only from bank income

Keep retained earnings for growth

Separate bank cash from owner cash

What can reduce payouts

Deduct loan loss provisions first

Pay taxes before dividends

Follow board policy and regulators

Cut distributions if credit losses rise

Retail Bank Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six levers that move owner take-home?

1

Earning Assets

$160M-$1.83B

More loans and securities lift net interest income, so this is the main engine for owner take-home.

2

Net Margin

57%-54%

A small move in yield versus funding cost changes profit fast across the whole asset base.

3

Deposit Cost

0.20%-3.50%

Shifting mix toward cheaper checking and savings protects spread income better than paying up for CDs.

4

Credit Quality

Edit

Loan losses and provisions can wipe out spread profit, so this needs an editable control as the book grows.

5

Efficiency

$105K/mo

Monthly overhead at this level decides how much EBITDA reaches owners after growth costs.

6

Fee Income

Edit

Service charges and card fees add profit without much balance-sheet risk, so keep this a separate editable field.

Retail Bank Core Six Income Drivers

Earning Asset Base

Earning Asset Base

The earning asset base is the pool of loans and securities that earns interest. In this model, it rises from $160M in Year 1 to $1.825B in Year 5, with loans growing from $100M to $15B and other earning assets from $60M to $325M. Bigger balances can lift owner profit fast, but only if the bank keeps funding, credit, and concentration risk in line.

Here’s the quick math: more earning assets mean more interest income, which can support higher retained earnings and owner distributions. But if deposit growth lags, the bank leans on pricier funding and the extra asset base can stop helping cash flow. Asset growth is only valuable when it stays liquid and well funded.

Track balance growth by asset type

Measure loans and securities separately, then test how each one funds itself. Track deposit growth, loan-to-deposit ratio, liquidity buffers, capital, and concentration limits before you add more assets. If deposits do not keep pace, owner pay should stay conservative because the balance sheet can grow faster than safe profit.

Use a simple rule: grow the earning asset base only when underwriting stays tight and funding is stable. Watch for asset growth that outpaces deposits, capital, or risk limits. That is the point where reported income can look strong while true cash available for the owner gets tighter.

1

Net Interest Margin

Net Interest Margin

Net interest margin is the spread between interest income on loans and securities and the funding cost on deposits and borrowings. In this model, NIM is 57% in Year 1 and 54% in Year 5, while weighted loan yield moves from 84% to 79%. When that spread shrinks, owner distributions shrink too, even if balance sheet growth stays on plan.

What this hides is rate pressure. If deposit costs rise faster than asset yields, cash available for profit draw drops fast. So the owner should treat NIM as a direct guardrail on take-home pay, not just a bank metric, and stress-test distributions before taking money out of the business.

Protect the spread

Track loan yield, deposit cost, and the mix of core deposits versus borrowed funds every month. The bank’s earnings depend on keeping funding cheap while new loans reprice well. A small slip in spread matters because NIM is the core profit engine, not a side metric.

Watch spread by product.

Stress-test lower-rate cycles.

Hold distributions after review.

Use the modeled decline from 57% to 54% as the warning case. If competition forces higher deposit rates or slower loan repricing, keep more earnings inside the bank for capital and loan-loss needs before raising owner pay.

2

Deposit Cost And Funding Mix

Deposit Mix and Margin

Low-cost core deposits, like checking and savings, are the cheapest fuel for net interest income. In the model, checking costs 0.25% in Year 1 and 0.20% in Year 5, while borrowed funds cost 5.20% and 5.00%. That gap widens margin and leaves more cash for taxes, reserves, and owner draws.

The deposit base excluding borrowed funds grows from $80M to $145B, so mix matters as much as size. If growth comes from higher-rate funding, balances can rise while profit falls. Here’s the quick math: shifting $100M from checking-style funding to borrowed funds adds about $4.95M a year in interest cost in Year 1.

Track Cost, Not Just Accounts

Track balance by funding type, rate paid, retention, and liquidity needs. You need customer checking and savings balances, borrowed funds, and the share of each product that stays on books. Use those inputs to forecast interest expense, not just account count, because expensive funding still squeezes owner income.

Core deposit balance

Borrowed funding balance

Average rate paid

Deposit retention

Liquidity gap

Price checking and savings for stickiness, not headline rate. Push direct deposit, bill pay, and advisor touchpoints so low-cost balances stay longer. If you need borrowed funds, keep them short term and recheck the spread often. Low-cost deposits protect margin; high-rate funding can buy growth but cut take-home income fast.

3

Credit Quality And Loan Losses

Credit Losses and Reserves

Credit quality hits owner income twice: it cuts reported profit and it traps cash in reserves instead of distributions. This model spans mortgages, personal loans, auto loans, credit cards, and student loans, with loans growing from $100M to $15B. As the mix shifts to higher-risk products, provisions and the allowance for loan losses must rise too.

Here’s the quick math: every extra dollar reserved for defaults lowers current profit and retained capital available to pay owners. If delinquencies or charge-offs move up, the bank can still look profitable on paper but have less cash to distribute. One line says it all: profit is not spendable until credit losses are covered.

Track Losses by Loan Type

Measure delinquency, charge-off, and reserve coverage by product, not just in total. Mortgages usually need different loss assumptions than credit cards or personal loans, so the owner should forecast each book separately. That keeps distributions tied to real cash earnings, not a blended number that hides risk.

Watch the allowance against the loan mix as balances scale from $100M to $15B. If riskier loans grow faster, provisions must rise before owner draws do. The key control is simple: do not pay out capital that credit losses may still absorb.

Track delinquency by loan type.

Update charge-offs monthly.

Stress reserves before distributions.

Separate safe and risky portfolios.

4

Fee And Noninterest Income

Noninterest Income

Noninterest income includes account service charges, card interchange income, origination fees, and ancillary services. It lifts owner income because it adds revenue that does not depend on the interest spread, so the bank can support profit even when funding costs move. Since no fee assumptions are provided, keep these as editable fields in the model and test them against deposit margins, loan quality, and customer churn.

The key issue is quality, not just size. Fee growth can improve cash flow and distributions, but customer retention, compliance limits, and reputational risk set the ceiling. Don’t use fee income to cover weak loan performance or thin deposit spreads; that only delays the pressure on profit and owner pay.

Measure Fee Income by Product

Track each fee line by customer count, card spend, account count, originations, and service usage. That shows which fee sources actually add profit after servicing costs. Keep a clean split between recurring fees and one-time fees so you can see what supports steady owner draws and what drops off when volume slows.

Track fee revenue by source.

Test retention after fee changes.

Check complaint and refund rates.

Document compliance review for each fee.

Stress-test profit without fee growth.

5

Operating Efficiency

Operating efficiency

The efficiency ratio is operating expense divided by income. Here’s the quick math: the model carries $105k/month in fixed overhead, which annualizes to $1.26M/year, plus a visible $250k CEO salary. Variable expense rates fall from 190% in Year 1 to 75% in Year 5, so better cost control can lift owner pay fast.

Don’t cut the wrong lines. Compliance, cybersecurity, fraud controls, and risk management protect cash flow and capital, so weak controls can erase the savings from a lower expense ratio. In a bank, a cheaper cost base only helps if it still supports safe growth and steady distributions.

Track the cost mix

Measure the ratio monthly, then split spend into fixed overhead, variable costs, and control functions. The key inputs are income, payroll, vendor fees, branch and tech costs, and control spend. If a cut lowers safeguards, it is the wrong cut.

If the goal is to move from 190% toward 75%, use automation, vendor resets, and simpler servicing flows, but keep audit, fraud review, and cyber defenses intact. That is what protects profit and lets the owner take a steadier draw.

Track monthly efficiency ratio.

Separate fixed and variable costs.

Protect control budgets first.

Test owner pay under stress.

6

Retail Bank Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: Compare low, base, and high retail bank owner income outcomes using assumption-based planning, not promises

Owner income scenarios

Owner income swings with deposit mix, loan yields, credit losses, fees, and payout policy. The same bank can stay near salary in a weak setup or build much more in a strong one.

Low, base, and high owner income cases for a retail bank.

Scenario

Low CaseConservative

Base CaseBase

High CaseUpside

Launch model

The low case assumes slower asset growth, tighter spreads, and heavier losses, so owner income stays close to pay only.

The base case uses the modeled asset path: $160M of Year 1 earning assets and about $1.825B by Year 5.

The high case assumes stronger asset growth, better spreads, and lighter losses, so owner income can move well above salary.

Typical setup

Deposit growth is softer, the loan mix is weaker, fees are thin, and the bank keeps more cash back for credit costs and capital.

The bank runs with $105k monthly fixed overhead, a $250k CEO salary, and the forecast loan and deposit mix in the model.

Deposits scale faster, the loan book earns more, fee income improves, and the bank keeps enough capital while lifting distributions.

Cost drivers

Thin net interest margin

slower deposit growth

higher credit losses

lower fee income

more capital retention

Modeled asset growth

$250k CEO salary

$105k monthly overhead

forecast spread income

standard credit losses

Faster earning asset growth

wider net interest margin

stronger fee income

lower credit losses

lighter capital retention

Owner income rangeBefore owner reserves

Near salary onlyDownside case

Salary plus distributionsModeled case

Salary plus upside payoutsUpside case

Best fit

Use this to stress-test the bank if funding costs rise, loan demand slows, or credit quality slips.

Use this as the working case for budgeting, hiring, and capital planning.

Use this to test what a strong deposit mix and cleaner credit performance could do for owner pay.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions.

In the provided base model, the bank has about $55M of Year 1 pre-provision, pre-tax profit capacity and about $874M by Year 5 That is not guaranteed owner income Actual take-home depends on loan losses, taxes, retained capital, board-approved dividends, and whether the owner also receives a salary

It depends on profitability, capital needs, and risk This model shows net interest income of about $91M in Year 1, but distributions still may be zero if the bank must retain earnings By Year 5, net interest income reaches about $987M before provisions, taxes, and capital retention decisions

Yes, but deposits are not profit by themselves The model has $80M of deposits excluding borrowed funds in Year 1 and $145B in Year 5 Those balances must be deployed into sound loans, securities, and liquid assets while managing funding cost, credit risk, and required capital

The biggest drivers are earning assets, net interest margin, deposit cost, credit quality, fee income, and efficiency ratio In this model, earning assets grow from $160M to $1825B, while NIM stays near 54% to 57% A small margin change on that asset base can move profit by millions

Grow quality earning assets without chasing risky loans or expensive deposits In this model, checking costs only 020% to 025%, while borrowed funds cost 500% to 520% That spread matters Also watch fixed overhead of $105k per month, variable expenses, provisions, and capital retention before planning owner distributions

About the author

Jonathan Bell

First-Time Founder Guide Writer

Jonathan Bell is a Financial Models Lab writer focused on launch budget planning, helping aspiring small business owners estimate startup needs before opening. As a first-time founder guide writer, he explains business costs in simple language and offers simple launch planning insights that help readers compare business opportunities realistically and make grounded real-world decisions.

Choosing a selection results in a full page refresh.