Retail Bank Startup Costs For A $100M Year 1 Loan Launch

Opening a retail bank requires more than ordinary startup spending because the bank must also support regulatory capital, liquidity, deposits, and loan funding In the researched assumptions, the first operating year includes $100M in loans, $90M in liabilities, $105K per month in fixed costs, and at least $830K in visible annual payroll before the listed $110K Compliance Officer role is fully scheduled Those figures are planning assumptions from the model, not vendor quotes or guaranteed approval costs Treat the retail bank startup cost range as three buckets: one-time setup costs, CAPEX, and separate funding needs for capital, liquidity, and early operating losses

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

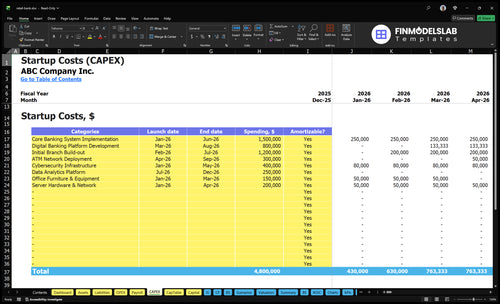

Estimates capitalized startup assets only for a retail bank, including branch build-out, technology, and launch implementation.

!

CAPEX only This calculator covers capitalized startup assets only. It excludes regulatory capital, deposits, loan funding, payroll runway, working capital, debt service, legal filings, marketing, and other operating costs.

How Much Money Do You Need To Start A Retail Bank?

You need more than visible startup spend to start a Retail Bank: the model carries $100M in Year 1 loans, $60M in other interest-earning assets, and $90M in liabilities, so funding must cover capital, liquidity, loan growth, and runway—not just opening costs. Track whether customer growth can support that balance sheet with What Is The Current Growth Trend Of Customer Acquisition For Your Retail Bank?, because approval is not purchased and regulatory capital is separate from the opening budget.

Core funding buckets

Fund $100M Year 1 loans

Hold $60M earning assets

Support $90M liabilities

Separate capital from startup costs

Visible opening costs

Budget one-time startup costs

Add CAPEX and liquidity

Fixed overhead: $1.26M/year

Payroll starts at $830K+

What Hidden Costs Of Starting A Retail Bank Should Founders Expect?

Retail Bank startup costs go well beyond branch buildout: legal review, regulatory consulting, audit readiness, BSA/AML setup, cybersecurity testing, vendor due diligence, training, background checks, insurance onboarding, customer disclosures, and pre-opening payroll. For the owner-income side, see How Much Does The Owner Of Retail Bank Typically Make?. Keep one-time setup separate from recurring costs, and treat working capital before revenue plus capital buffers as their own buckets.

One-time setup costs

Legal review before launch

Regulatory consulting and filings

Audit readiness workpapers

BSA/AML and cybersecurity setup

Recurring monthly costs

$8K monthly professional services

$12K monthly regulatory and compliance fees

$10K monthly insurance

$105K total monthly fixed costs

What Are The Biggest Cost Drivers For Starting A Bank?

Starting a Retail Bank is a fixed-cost game. Regulation, chartering, compliance infrastructure, core banking tech, cybersecurity, branch readiness, insurance, and staffing hit before income does. Here’s the quick math: monthly non-payroll costs in the model total $92K ($20K IT software licenses + $15K data center/cloud + $12K regulatory/compliance fees + $10K insurance + $35K branch rent and maintenance), and Year 1 staffing adds about $940K, or about $2.044M total before growth.

Big fixed cost drivers

$20K monthly IT software licenses.

$15K monthly data center and cloud hosting.

$12K monthly regulatory and compliance fees.

Insurance is $10K; branch rent and maintenance is $35K.

Year 1 staffing load

CEO at $250K.

Head of Lending at $180K and Software Developer at $120K.

Compliance Officer at $110K and Branch Manager at $90K.

Financial Advisor at $80K plus two Customer Service Representatives at $55K each.

Calculate Fuding Needs

Startup cost summary

This table summarizes the bank's main startup CAPEX and the excluded opening cash need used to fund launch and early operations.

Regulatory Formation And Chartering Startup Expense

Charter Filing

Bank charter and de novo regulatory costs are mostly professional work, not a shortcut to approval. Budget for legal counsel, regulatory advisors, application prep, feasibility studies, organizer support, policy drafting, examiner-response support, board materials, and, when needed, Federal Deposit Insurance Corporation (FDIC) insurance application work. Treat these as filing and advisory costs, then add $8K/month in professional services and $12K/month in regulatory and compliance fees.

Cost Inputs

Estimate this line with scope times months of support plus outside quotes. The key inputs are application complexity, whether FDIC work is needed, how many draft cycles are required, and how long the team stays on through examiner questions. This cost sits in startup overhead, not in capital, liquidity, deposits, loan funding, or post-launch losses.

Count draft and response cycles

Quote monthly advisory support

Separate filing from capital

Control Spend

Keep the work tight by using fixed-scope quotes, one lead counsel, and a clear document owner for policies and board materials. Do not cut reviewer time or examiner response support, because that usually raises rework. A lean team can still stay compliant if it prices the full path up front, including recurring $8K and $12K monthly run rates.

Ask for fixed-fee milestones

Bundle policy drafting

Protect examiner response time

Budget Guardrails

The clean rule is simple: budget chartering work as a pre-launch regulatory expense, then fund regulatory capital and operating liquidity separately. That keeps the model honest and avoids mixing approval costs with balance sheet funding needs. If the filing takes longer than planned, the extra burn usually shows up in advisory hours, compliance fees, and repeated document revisions.

Branch Buildout And Security Startup Expense

Buildout scope

A branch opening needs the physical shell: leasehold improvements, teller line, customer area, office space, signage, accessibility work, vault or safe, alarms, cameras, and access control. Estimate it from square feet, finish level, security scope, and contractor quotes. Do not fold rent into CAPEX unless leasehold accounting requires it.

Cut rework

Use one bid package and a standard branch layout to avoid change orders. Lock drawings before permits, and confirm accessibility and security specs early. Get separate quotes for furniture, signage, and low-voltage work so the opening budget stays tied to readiness, not future expansion.

Freeze layout before bidding

Price security separately

Check accessibility twice

Security stack

Physical security is a separate line item, not a vague overhead bucket. It includes vault or safe infrastructure, alarm systems, cameras, and access controls, plus install work to tie them together. The key inputs are device count, monitoring scope, and installation quotes. If one is missing, the opening budget will be too low.

Rent anchor

Use the model anchor of $35K per month for branch rent and maintenance from Month 1 through Month 60. That is $2.1M over five years before any leasehold accounting treatment. Keep this block separate from startup buildout so you can see opening cash need versus ongoing occupancy cost.

Core Banking Technology And Cybersecurity Startup Expense

Core stack

A retail bank’s core stack is usually two buckets: one-time build work and ongoing run costs. Use $20K per month for IT software licenses and $15K per month for data center and cloud hosting as the baseline. That covers the platform, card and payment links, security tools, and reporting needed to open with a real product set.

Setup math

For the startup build, separate implementation from monthly run costs. Quote the core banking vendor, mobile and web setup, card and payment links, security tools, compliance reports, testing, employee devices, and hosting. Your model needs users, devices, integrations, and months of coverage. One-time software work is capitalized if your accounting policy allows it; recurring fees hit operating expense.

Control spend

Keep the first release tight. Launch the core platform, security, and reporting first, then add loans and card rails only when service volume justifies them. That keeps licenses and hosting aligned with live accounts instead of the full Year 1 wish list. Watch for the common mistake: paying for features before they drive deposits or loan origination.

Phase product rollouts.

Match hosting to traffic.

Test every payment link.

Year 1 scope

Year 1 product breadth matters because each product adds setup, testing, reporting, and support load. A bank offering mortgages, personal loans, auto loans, credit cards, student loans, savings, checking, certificates of deposit, and money market accounts needs a bigger core and more controls than a deposits-only launch. Size the tech stack to the product list, not the launch date.

Staffing Readiness And Pre-Opening Payroll Startup Expense

Pre-Open Payroll

Before opening day, a retail bank can already carry $940K in listed annual salaries, and the visible schedule is still not finished on the compliance side. That means payroll is a real startup cash need, not a nice-to-have, and it belongs in pre-opening expense or working capital.

Core Roles

Use headcount times salary to build this line: CEO $250K, Head of Lending $180K, Branch Manager $90K, Financial Advisor $80K, 2 Customer Service Representatives $110K, Software Developer $120K, and Compliance Officer $110K. The visible plan already clears $830K before the compliance FTE schedule is complete.

What To Include

This cost covers recruiting, background checks, training, and payroll before revenue starts. Build it from salary months needed to hire and onboard, then add the launch runway. Do not mix it with branch buildout or software capital spend; this is cash burn tied to staffing readiness.

How To Budget It

Keep the team lean until launch timing is locked, but do not delay compliance or lending leadership. Stage start dates where you can, use contractors for short gaps, and avoid hiring months too early. The key is simple: pay for readiness, not idle seats.

Compliance, Insurance, And Risk Management Startup Expense

Regulated launch floor

Compliance and risk management are not optional for a retail bank launch. Use a baseline of $12K/month in regulatory and compliance fees plus $10K/month in insurance, or $264K/year before staff, to cover BSA/AML, fraud controls, customer identification, internal controls, policy development, audits, cybersecurity governance, and launch checks.

Cost build

Split one-time setup from recurring run-rate. One-time work includes legal counsel, application prep, examiner-response support, board materials, vendor due diligence, and disclosure drafts. Recurring work includes compliance staff, monthly fees, insurance premiums, audits, and capital buffers. Build it as months × monthly rate, not one lump sum.

Count setup hours once.

Price monthly fees separately.

Keep buffer cash outside CAPEX.

Cost control

To keep this cost tight, write policies early, use a small vendor list, and bind insurance before launch. The expensive mistake is redoing controls after the first exam or incident. BSA/AML means Bank Secrecy Act and anti-money laundering; if the workflow is vague, review time and rework go up fast.

Approve policies before buildout.

Test controls with real cases.

Fix gaps before opening day.

Launch gate

Do not open until customer disclosure text is approved, insurance is bound, audit files are ready, and fraud monitoring is live. If any of those lag, you are not ready to take deposits. That last mile matters because compliance failures hit both cost and trust at the same time.

Compare 3 Startup Cost Scenarios

Scenario table

Startup cost rises as you add branches, lending products, staff, and compliance. Lean stays digital-heavy, Base matches one branch, and Full adds broader reach plus more control layers.

Lean, Base, and Full retail bank startup cost comparison

Scenario

Lean LaunchLow CAPEX

Base LaunchMid CAPEX

Full LaunchHigh CAPEX

Launch model

A limited-branch launch with digital support and a tighter physical footprint.

A single-branch consumer bank sized to the model's Year 1 loan, asset, and deposit levels.

A broader launch with more branches, deeper product depth, and heavier control needs.

Typical setup

Use one small branch, core banking, and a lean ops team.

Run one branch, digital channels, and the staffing needed for lending and service.

Run multiple customer channels, more staff, and stronger security and data systems.

Cost drivers

Core banking build

cybersecurity

smaller branch fit-out

lighter staffing

lower compliance load

Core banking system

branch build-out

Year 1 payroll

compliance fees

working cash

Multiple branch buildouts

higher payroll

security and tech

compliance overhead

larger working capital

Planning rangeCAPEX only

$8,000,000 - $15,000,000Lower cash need

$20,000,000 - $28,000,000Model-aligned

$30,000,000 - $45,000,000Largest cash need

Best fit

Fits founders who want a digital-heavy start and can keep customer volume focused.

Fits a launch that matches the modeled operating scale and needs enough cash for the build and ramp.

Fits teams aiming for wider reach and a heavier operating model from day one.

!

Planning note: These ranges are researched planning assumptions from the model, not vendor quotes or exact funding offers.

A retail bank needs startup costs plus separate funding for capital, liquidity, deposits, and loans The model shows $105K in monthly fixed costs, at least $830K in visible scheduled Year 1 payroll, and a first-year balance sheet with $100M in loans Those are planning inputs, not a complete approval budget or vendor quote

Cost planning should cover launch and the early operating years This model runs from Month 1 through Month 60, with fixed costs active across the full 60-month period Year 1 includes $100M in loans, $60M in other interest-earning assets, and $90M in liabilities, so a one-month opening budget is not enough

A US retail bank that accepts insured deposits generally needs Federal Deposit Insurance Corporation involvement, along with a chartering path The cost plan should include regulatory advisors, legal work, compliance policies, and examiner-response support In the model, regulatory and compliance fees are $12K per month, separate from capital, deposits, and loan funding

Treat startup costs as money spent to get ready, and capital as money kept in the bank to support risk and growth For example, $35K monthly branch rent, $20K software licenses, and $10K insurance are operating costs The $100M Year 1 loan book and $90M liabilities are balance sheet funding items, not ordinary setup expenses

Not every cost plan needs the same branch footprint, but this model includes a branch cost anchor Branch rent and maintenance are $35K per month from Month 1 through Month 60 A digital-supported plan may reduce buildout and teller-area costs, but it still needs core banking technology, cybersecurity, compliance systems, and customer support capacity

About the author

Simon Reed

Small Business Educator

Simon Reed is a small business educator at Financial Models Lab who helps service business founders understand the numbers behind everyday business ideas. He focuses on pricing and margin basics, common business costs, and the first months after launch, giving readers a clearer view of what it takes to build a healthy business. Simon brings a simple, confident approach that balances optimism with cost-aware planning.

Choosing a selection results in a full page refresh.