Ride-Hailing Owner Income With 25% Take Rate And $1680 Fares

You’re not estimating driver wages here you’re estimating what a US ride-hailing operator can keep after driver payouts, platform costs, insurance, marketing, support, reserves, and reinvestment The model period runs from first year to mature year, with weighted average fares moving from $1680 to $1935 and variable commission moving from 2500% to 2200% Owner take-home is a planning output, not a guaranteed salary or tax answer

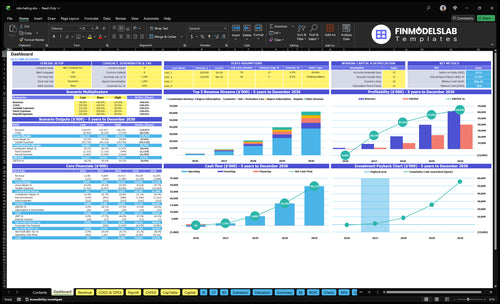

Owner income$150kNet margin82%Revenue for target pay$153kBusiness difficultyHard

Want to test your ride count?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, operating costs, reserves, and target owner pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to see the six biggest income drivers?

1

Ride Volume

5.4k-9.1k/mo

More completed rides spread the $18.5k fixed load and get you past the 5,438-rides break-even before payroll, or 9,112 with founder pay.

2

Average Fare

$16.8-$19.4

Higher fares lift commission dollars fast; the model moves from $16.80 in year 1 to $19.35 in mature year as premium and luxury mix rises.

3

Take Rate

22%-25%

Commission drops from 25.0% to 22.0%, and the fixed fee climbs from $0 to $0.50, so pricing changes swing owner take-home.

4

Driver Pay

4.0%-3.0%

Driver incentives and support ease from 4.0% to 3.0% of revenue, which keeps more gross profit after payouts.

5

Operating Costs

$18.5k

Ride insurance sits at 5.0% to 4.5% and fixed overhead totals $18.5k a month, so this driver sets reserve needs and cash burn.

6

Acquisition Efficiency

CAC -40%

Rider CAC falls from $50 to $30 and driver CAC from $250 to $150, so each new account costs less and payback improves.

Want to stress-test owner income in Ride-Hailing?

The dashboard in the Ride-Hailing Financial Model Template shows assumptions, revenue build, costs, cash flow, and owner take-home; open the model to test it.

Owner-income model highlights

Owner pay capacity

Revenue and margin

Scenario inputs

How many rides does a ride-hailing business need to make money?

Ride-Hailing needs about 5,438 rides per month to cover $18,500 in fixed overhead, and about 9,112 rides per month after adding $12,500 in founder pay. Here’s the quick math using a $16.80 weighted fare, 25.00% commission, $4.20 platform revenue per ride, and about $3.40 contribution after listed variable costs; track service quality alongside volume with What Is The Current Customer Satisfaction Level For Ride-Hailing?.

Break-even rides

5,438 monthly rides before payroll

About 181 rides per day

$18,500 ÷ $3.40 contribution

Needs dense local demand

Founder-pay target

9,112 monthly rides before taxes

About 304 rides per day

Driver supply must match peaks

Discount-led volume can still lose money

Can a ride-hailing business support full-time owner income?

Ride-Hailing can support a full-time owner, but only when ride density covers fixed overhead, staff, reserves, and founder pay. With a $150,000 annual CEO/founder salary target, that is $12,500 a month, and the known fixed load needs about 9,112 rides per month before taxes and reserves; adding a $140,000 CTO/lead developer salary adds about $11,667 a month and pushes the threshold to about 12,542 rides per month.

Owner pay math

$12,500 monthly founder pay target

9,112 rides/month to cover it

Threshold is before taxes and reserves

Owner-led ops can cut cash burn

What raises the bar

$140,000 CTO salary adds $11,667/month

Known threshold rises to 12,542 rides/month

Managed platforms need support and compliance

Marketing and technology overhead still matter

What ride-hailing operating costs compress owner take-home?

Ride-Hailing takes take-home fast when variable costs run hot; if you're sizing startup spend, check What Is The Startup Cost To Launch Your Ride-Hailing Business? first. In year one, COGS and variable costs total 190% of platform revenue, led by 20% payment processing, 50% ride insurance, 80% user acquisition marketing, and 40% driver incentives and support. Mature-year cost rate improves to 153%, but fixed overhead still runs $18,500 a month, so at 10,000 first-year rides contribution is about $34,020 and operating profit before payroll is about $15,520. Founder pay still needs more volume.

Big cost leaks

190% year-one variable cost load

50% ride insurance is the biggest line

80% marketing hits take-home hard

40% driver support and incentives stay heavy

Volume still matters

$18,500 monthly fixed overhead

10,000 rides gives $34,020 contribution

$15,520 profit before payroll

More rides are needed for founder pay

Key Takeaways

About 5,438 rides cover monthly overhead.

Higher fares help only when rides complete.

Take rate and driver pay set contribution.

Repeat riders matter more than paid growth.

Scenario objective: compare low, base, and high ride-hailing owner-income cases without treating them as expected results

Owner income scenarios

Ride volume, fare mix, and commission rates swing owner pay fast here. Fixed overhead is steady, so the break-even ride count changes a lot by case.

Low, base, and high planning cases show how ride volume changes founder pay.

Scenario

Low CaseDownside case

Base CaseBase case

High CaseUpside case

Launch model

This is the lower earnings path, and cash reserves stay under pressure.

This is the modeled case, with ride volume near the owner pay threshold.

This is the stronger earnings path, where mature-year economics ease the pay hurdle.

Typical setup

First-year volume stays below 5,438 rides a month, so the $18,500 fixed overhead and payroll base are not fully covered.

First-year volume reaches about 9,112 rides a month, using a $16.80 fare, 25.0% commission, 19.0% variable and COGS, $18,500 fixed overhead, and $12,500 monthly founder pay.

By mature year, a $19.35 fare, 22.0% commission, $0.50 fixed commission, and 15.3% variable and COGS lower the threshold to about 7,694 rides a month.

Cost drivers

Low ride count

$18,500 fixed overhead

25.0% commission

19.0% variable and COGS

thin reserve cushion

$16.80 fare

25.0% commission

19.0% variable and COGS

$18,500 fixed overhead

$12,500 founder pay

$19.35 fare

22.0% commission

$0.50 fixed commission

15.3% variable and COGS

lower ride threshold

Owner income rangeBefore owner reserves

Under 5,438 rides/moBelow target

Around 9,112 rides/moNear target

Around 7,694 rides/moHigher upside

Best fit

Use this to stress-test a slow launch, weak demand, and tighter cash planning.

Use this as the main planning case for cash, staffing, and owner pay decisions.

Use this to test a stronger mix, better unit economics, and what it takes to fund growth.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Ride-Hailing Core Six Income Drivers

Completed Ride Volume

Completed Ride Volume

Completed ride volume is the count of rides that finish and clear payment. In ride-hailing, it is the top owner-income driver because each ride adds platform revenue and helps absorb fixed overhead. With about $340 contribution per ride after listed variable and COGS, $18,500 of monthly fixed overhead needs roughly 5,438 rides before founder pay.

At $150,000 founder pay, the business needs about 9,112 rides per month before taxes and reserves. The risk is empty growth: discounts can lift volume without profit, weak driver supply can cap completions, and low repeat use can make demand fade fast.

Track Completion, Not Just Demand

Measure completed rides by hour, zone, and rider type, then compare them with driver online supply and completion rate. The key input is not just bookings; it is rides that actually finish and pay. When demand density and driver availability stay balanced, owner pay can rise without extra promos or higher incentives.

Track rides completed per day

Watch driver online supply

Separate promo rides from repeat rides

Test completions without discounts

If volume grows only from discounting, margin usually falls. If onboarding takes too long or drivers go offline in busy zones, completed rides stall and fixed overhead stays heavy.

Average Fare Per Ride

Average Fare Per Ride

Average fare per ride sets gross fare volume, but the owner only keeps the platform revenue after the take rate. In the model, first-year weighted fare is $1,680 from the Casual, Regular, and Commuter mix, and mature-year weighted fare rises to $1,935 as Regular and Commuter riders grow.

Higher fares help only if completion rates and repeat rides stay strong. Short trips can lift ride count but cap fare dollars; longer or premium trips raise fare volume, but pricing too high can cut demand and force more promotions, which reduces the owner’s take-home income.

Track Fare Mix and Net Yield

Measure fare by rider type, route, and time of day, then compare it with completed rides and promo spend. If the mix shifts toward Regular and Commuter riders, the weighted fare should move toward $1,935; if conversion drops, the higher sticker price is not helping profit. One clean check: net revenue per completed ride.

Test small price moves, then watch completion rate, repeat rides, and cash collected per ride. Keep the take rate intact, because gross fare only helps the owner when it turns into platform revenue after payouts and promos. If fares rise but repeat use falls, margin and owner pay usually get hit.

Platform Commission Rate

Platform Commission

The platform commission rate is the share of gross passenger fares that becomes net platform revenue. With a 25.00% first-year variable commission, a $1,680 ride brings about $420 before listed costs. In the mature year, 22.00% plus $0.50 per order brings about $370.10. That spread moves owner pay one ride at a time.

There’s no universal take rate here. A higher rate can lift margin, but it can also squeeze driver economics and slow supply; a lower rate can help drivers, but it can delay owner distributions. The real check is contribution per ride after incentives and support, because that is what funds fixed overhead and profit.

Track Net Take

Measure net revenue per completed ride, not just gross fares. Split the model by city and rider mix, then test whether 25.00% still clears enough supply better than 22.00%. If wait times rise or cancellations climb, the rate is probably too high for that lane.

Build the forecast around fare mix, ride count, and the fixed $0.50 fee per order. That shows whether owner draw is funded by real contribution or by discount-led volume. If you miss the fee, cash flow will look stronger than it is.

Review commission by city weekly

Watch driver supply and cancellations

Reprice before margin slips

Driver Payouts And Incentives

Driver Payouts And Incentives

Driver payouts and incentives decide whether rides get completed and what margin is left for the owner. The stated 2500% first-year platform commission means 7500% of fare value is not retained as variable commission before other fees, while driver incentives and support add 40% of platform revenue in year one and 30% in the mature year.

Here’s the tradeoff: pay too little and completion rates and rider retention drop; pay too much and profit per ride shrinks. Supply gaps can force faster payouts, bigger bonuses, or lower commissions, so owner income depends on keeping enough qualified drivers without giving away too much of each ride.

Track payout rate by ride

Measure driver payout as a share of platform revenue, plus bonus spend, payout speed, and completion rate. The key test is simple: if a small bonus lift raises completed rides more than it cuts margin, it helps owner income. If not, it is just expensive demand shaping.

Track completed rides per active driver.

Watch rider repeat after payout changes.

Flag shortages by zip code.

Test bonuses before lowering commissions.

Build forecasts with three inputs: completed rides, payout mix, and support cost. That shows how much cash stays after variable driver pay and whether the owner can still cover fixed overhead and take a draw. If on-time payouts slip, supply risk rises fast.

Customer Acquisition And Retention Efficiency

Ride Acquisition and Repeat Use

Customer acquisition cost (CAC) sets how fast owner pay can start. In year one, rider marketing is $1,000,000 at $50 CAC, so that buys 20,000 riders; driver marketing is $500,000 at $250 CAC, so that buys 2,000 drivers. That is $1.5 million of spend before repeat usage carries the model.

Here’s the quick math: mature CAC falls to $30 for riders and $150 for drivers, while repeat rides rise from 200 to 250 for Casual, 500 to 600 for Regular, and 1,000 to 1,200 for Commuter. The risk is paying for promos to push rides while delaying owner distributions. Owner income improves when repeat trips replace paid acquisition.

Track CAC by cohort and repeat rate

Measure rider and driver CAC by month, then split repeat rides by segment. If CAC stays high but repeat rides do not move from 200/500/1,000 toward 250/600/1,200, the spend is just buying churn. The owner should watch payback speed, not just signups, because cash gets trapped until usage becomes habitual.

Test promos against retention, not just bookings. A lower CAC only helps if it comes with more repeat rides, better driver supply, and fewer empty trips. Keep a simple rule: if acquisition spend rises faster than repeat usage, owner draw should wait; if repeat use rises and CAC falls, cash flow can support pay sooner.

Insurance, Compliance, Support, And Platform Overhead

Insurance, Compliance, and Platform Overhead

This cost stack hits owner pay fast. In year one, ride-hailing COGS includes 20% payment processing and 50% ride insurance premiums, so 70% of platform revenue is gone before fixed overhead. In the mature year, those rates ease to 18% and 45%, but the business still carries $18,500 per month in rent, software, hosting, legal, regulatory compliance, supplies, professional services, and app maintenance.

Here’s the quick math: fixed overhead alone is $222,000 a year. That means owner take-home stays thin until ride volume spreads those costs. The real risk is underbudgeting insurance, support, background checks, or compliance; if those run hot, operating profit drops before any owner draw gets paid.

Track the cost per completed ride

Build the forecast from ride volume, average fare, take rate, claims, support tickets, background-check volume, and compliance work. That tells you how much of each ride is left after payment processing and insurance, and whether fixed overhead is shrinking or growing as a share of revenue.

Watch COGS % and monthly fixed spend every month. If claims, support, or compliance rise faster than rides, delay owner distributions and tighten approval rules, vendor terms, and dispute handling. The goal is simple: keep semi-fixed costs flat while ride volume climbs.