How Much a Roadside Assistance Owner Can Make With $180k CEO Pay

You’re planning owner pay before the model is safely cash-positive, so separate salary from profit In this five-year roadside assistance model, owner income includes a planned $180,000 CEO salary, while EBITDA moves from -$695,000 in Year 1 to $15322 million in Year 5 This excludes tax advice, guaranteed local pricing, and personal benefits

Owner income$180kNet margin-13.0%Revenue for target pay$1.7MBusiness difficultyHard

Which drivers control owner income most?

1

Call Volume

0.10h

More active customers spread the $18K monthly overhead faster, so this is the main path to breakeven and take-home.

2

Labor Model

$180K

The CEO pay line and staffing scale drive the biggest burn, so every extra FTE cuts owner profit.

3

Avg Ticket

$12.99

Per-call pricing is user-entered, so better plan mix and add-ons lift margin without needing as many calls.

4

Truck Utilization

20.5%

Higher truck use lowers service cost as a share of sales and turns each dispatch into more profit.

5

Cost Control

$18K/mo

Keeping office, software, and admin tight protects cash when the model still shows a -$375K minimum cash trough.

6

Channel Mix

$35 CAC

Better acquisition channels cut the cost to win each driver, which helps cash in the early months.

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice. The model reaches breakeven in Month 10 and minimum cash of -$375,000.

Can you check owner income in the model?

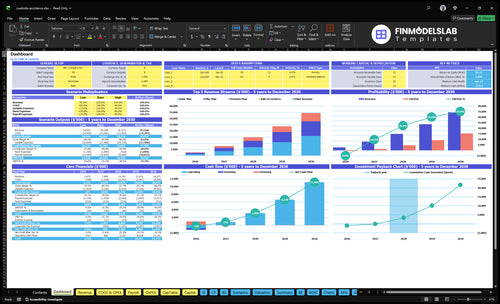

This dashboard shows owner pay, EBITDA, cash, customer growth, revenue, COGS, payroll, fixed costs, capex, and reserves, plus assumptions for pricing, CAC, fees, and support—open the Roadside Assistance Financial Model Template.

Owner-income model highlights

Year 1 -$695,000 EBITDA

Month 10 breakeven

27-month payback, -$375,000 cash

How does scaling a roadside assistance business affect owner income?

Scaling Roadside Assistance can raise owner income once utilization catches up, but it can also cut percentage margin if trucks, technicians, dispatch, or partner coverage sit idle. In this model, marketing grows from $12 million in Year 1 to $70 million in Year 5, CAC falls from $35 to $26, payroll rises from $995,000 to $2.625 million, and EBITDA improves to $15,322 million by Year 5, so the owner wins only if the service network stays busy.

Income driver

More jobs spread fixed costs.

Idle trucks hurt margin fast.

CAC drops from $35 to $26.

Utilization is the main lever.

Cash risk

Marketing rises to $70 million.

Payroll reaches $2.625 million.

Minimum cash hits -$375,000 in Month 16.

Keep reserves ahead of growth.

How many roadside assistance calls per day to make money?

There isn’t one fixed number for Roadside Assistance; the call target depends on contribution per call, not just volume. Using the provided costs, the monthly fixed burden is $215,917 ($18,000 overhead + $82,917 payroll + $100,000 marketing + $15,000 owner pay), so break-even calls per day = $215,917 divided by contribution per call and operating days. The model’s breakeven is Month 10.

What drives the call count

No universal calls/day

Use contribution per call

Include operating days

Keep the model editable

Quick break-even math

$215,917 monthly burden

$18,000 overhead

$82,917 payroll

$100,000 marketing

Is a roadside assistance business profitable?

Yes, Roadside Assistance can be profitable, but not right away: Year 1 EBITDA is -$695,000, then it turns positive in Year 2, and you can pair that with the startup-cost context in How Much Does It Cost To Open And Launch Your Roadside Assistance Business?. The catch is service mix, because towing, battery work, lockouts, tire changes, and fuel delivery do not all carry the same cost. So high revenue is not the same as high margin.

Profit path

Year 1 EBITDA: -$695,000

Year 2 EBITDA: $1,269 million

Year 3 EBITDA: $4,465 million

Year 4 EBITDA: $9,203 million

Margin drivers

Year 1 COGS: 205%

Variable expenses: 95%

Contribution: about 700%

Year 5 EBITDA: $15,322 million

Key Takeaways

More billable calls help only when trucks stay busy.

Pricing and service mix raise income only if costs lag.

Marketing must lower CAC faster than revenue grows.

Cash reserves matter because breakeven still leaves losses.

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with CAC, plan mix, and marketing spend. Early years keep the CEO on salary only, while later years can support distributions after reserves and reinvestment.

Low, base, and high cases show when salary stands alone and when distributions can start.

Scenario

Low CaseLow case

Base CaseBase case

High CaseHigh case

Launch model

Lower earnings path with salary only and no safe distribution.

Modeled mid case with salary plus limited distribution after reserves.

Stronger earnings path with salary plus distributions after reinvestment.

Typical setup

Year 1 ramp, $1.2 million marketing, $35 CAC, and -$695k EBITDA keep the owner on salary only.

Year 2 operating shape, $2.5 million marketing, $32 CAC, and $1.269 million EBITDA can support pay after cash is set aside.

Year 5 scale, $7.0 million marketing, $26 CAC, and $15.322 million EBITDA can fund owner pay after growth spend.

Cost drivers

CEO salary

$1.2M marketing

$35 CAC

-$695k EBITDA

$375k min cash

$2.5M marketing

$32 CAC

$1.269M EBITDA

reserve-first payout

steady plan mix

$7.0M marketing

$26 CAC

$15.322M EBITDA

reinvestment load

scaled support team

Owner income rangeBefore owner reserves

$180,000 onlySalary only

$180,000 plus reservesReserve first

$180,000 plus distributionsDistribution upside

Best fit

Founders stress-testing Year 1 ramp and cash risk.

Operators who want a realistic post-launch income check.

Owners modeling mature-year scale and payout capacity.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Roadside Assistance Core Six Income Drivers

Call Volume and Truck Utilization

Call Volume and Truck Utilization

More qualified roadside calls only lift owner income when dispatch, routing, response time, and technician capacity hold up. The model uses active-customer usage, a proxy for paid service time, at 10 billable hours per month in Year 1 and 8 by Year 5; if trucks sit idle, payroll, vehicles, and coverage costs still hit cash flow.

Here’s the quick math: low utilization spreads fixed overhead, including $18,000 per month, across too few jobs. High utilization helps only if uptime stays strong, because missed calls and slow response can raise churn and erase the extra contribution dollars that should flow to owner pay.

Track Billable Hours per Truck

Measure qualified calls per day, billable hours per active truck, and missed-call rate. If calls rise but response time slips, revenue quality drops fast. Test route density by zip code, then add capacity only where trucks can still answer fast and stay busy.

Track hours per truck weekly.

Watch response time by zone.

Flag missed calls daily.

Compare payroll to contribution dollars.

That’s the real test: contribution dollars need to grow faster than fixed overhead and support cost. If they don’t, more volume just creates more strain, not more take-home income.

Operating Costs and Cash Reserves

Operating Costs and Cash Reserves

When the business carries $18,000 a month in fixed costs and 95% variable expenses, owner pay comes last. Even if breakeven lands in Month 10, the model still shows minimum cash at -$375,000 by Month 16, so paper profit does not mean safe take-home pay.

Here’s the quick math: thin reserves turn a good month into a cash squeeze. COGS at 205% also signals that service delivery can eat more cash than expected, so the owner cannot treat early profit as distributable income until operating buffers are funded.

Protect Cash Before Owner Pay

Track monthly burn, gross margin, and cash runway before setting any owner draw. The key inputs are revenue, variable expense rate, COGS, fixed overhead, and the reserve floor needed to survive delays between breakeven and actual cash recovery.

Hold owner pay until reserves are funded.

Review burn against a 12-month runway.

Test higher pricing before adding draw.

Cut fixed costs below $18,000 if possible.

If cash starts to trail the plan, freeze distributions fast. The business can look profitable on paper and still force the founder to fund payroll, software, and insurance out of pocket, which is where stress and missed payments usually begin.

Owner-Operator vs Employees

Owner Labor Mix

Owner-led dispatch, sales, and service work can protect early cash because it delays hiring, but only until call volume rises. In this model, payroll starts at $995,000 in Year 1, including a $180,000 CEO salary, then climbs to $2.625 million by Year 5 as support scales. More labor raises capacity, but it also locks in fixed cost.

Once customer support grows from 30 FTE to 180 FTE, the business can answer more calls and keep service moving, but the owner loses flexibility and takes on scheduling, training, compliance, and management load. The key test is whether added labor lifts retained revenue faster than payroll and overhead. If not, owner pay gets squeezed fast.

Track Labor Before You Hire

Measure calls per FTE, owner hours on dispatch and sales, payroll per subscriber, and support time per job. If the owner is still covering core work, keep a hard cap on hiring until response times and churn stay stable. One clean rule: every new hire should free enough owner time or add enough capacity to pay for itself.

Track payroll as revenue grows.

Split owner work from staff work.

Test hire timing by call load.

What this estimate hides: training time, compliance work, and supervisor layers. If those rise faster than billable volume, labor becomes a fixed burden instead of a growth engine, and the owner’s draw gets pushed back.

Channel Mix and Customer Acquisition

Channel Mix and CAC

Direct calls can support higher pricing, but motor club or insurance-style dispatch brings steadier volume with less control over rate cards and response rules. Here’s the quick math: $12 million of Year 1 marketing at $35 CAC implies about 342,857 customers; by Year 5, $70 million at $26 CAC implies about 2.69 million. Owner income rises when acquired customers stay active and paid spend grows slower than cash from service.

What this hides: if marketing is 80% of revenue in Year 1 and 60% in Year 5, the model is still spend-heavy early. If retention slips or dispatch partners force lower pricing, extra volume won’t reach take-home pay. One clean rule: growth only helps when repeat use pays back acquisition.

Measure CAC by Channel

Track CAC by source, not just total spend. Split direct calls, motor club, and insurer-style dispatch so you can see which channel brings cheaper repeat customers and which one creates volume with tighter service rules. Use the same unit test for each channel: leads, conversions, first-job rate, repeat rate, and net revenue after service cost.

Watch CAC vs. repeat use

Test pricing by channel

Protect response-time rules

If one channel lifts volume but cuts margin, cap spend there until retained customers pay back the move from $35 CAC to $26 CAC faster. That is the lever that turns paid acquisition from cash burn into owner income.

Truck Costs and Vehicle Uptime

Truck Costs and Uptime

Truck costs here mean roadside repairs, tires, tools, equipment replacement, and the cash lost when a unit sits idle. The key metric is billable hours per truck, because downtime cuts revenue and also adds cost. The model does not disclose truck payment or maintenance amounts, so those lines should stay editable.

Here’s the quick math: if one vehicle is down, you lose dispatch capacity right away, but insurance, payroll, and software still run. That means profit drops twice, once from lower service volume and again from higher repair spend. The tighter the fleet uptime, the better the owner’s draw.

Track Uptime by Unit

Track downtime hours, repair spend, tire life, and tool replacement by vehicle, not in one pool. Set a monthly reserve per truck from actual service history, then compare it with lost billable hours. If a truck misses dispatches, the fix is faster maintenance, not more sales spend.

Use uptime % and cost per billable hour to decide when to repair, replace, or retire a unit. If downtime pushes missed calls higher, raise coverage or add backup capacity before churn shows up. The goal is simple: keep vehicles earning while fixed overhead keeps moving.

Average Ticket and Service Mix

Average Ticket and Service Mix

This driver is the average cash you collect per roadside job, shaped by towing, jump starts, flat tires, lockouts, fuel delivery, and battery work. Year 1 pricing is membership-based at $999, $1,499, and $2,499 per month, with a weighted plan price of $1,299 before add-ons.

If the mix shifts toward higher-ticket jobs and add-ons, owner pay rises only when fulfillment, fuel, equipment, and partner payments stay below the price lift. With $18,000 of monthly fixed overhead, margin quality matters more than ticket size alone.

Track Mix by Job Type

Measure average revenue and direct cost by job type, not just total calls. Here’s the quick filter: track plan fee, add-ons, dispatch time, partner payout, fuel, and equipment cost for each service. A richer mix helps only when the extra dollars drop faster than the service cost.