How Much Can a Scope 3 Reporting Service Owner Make? $180k+

You’re planning owner pay before the firm has steady delivery capacity, so the clean baseline is the modeled Managing Director pay of $180,000 per year These are planning assumptions for a private US Scope 3 reporting business, covering revenue, gross margin, overhead, cash needs, EBITDA, reserves, and owner pay before taxes

Owner income$180kNet margin24% to 41%Revenue for target pay≈$756kBusiness difficultyHard

Want the six drivers behind owner income?

1

Sales Positioning

$12K-$9.5K

Compliance-led demand brings in bigger deals and lowers CAC, but risk stays high until the cash trough at $689K in Month 5.

2

Contract Value

$1.99M-$7.66M

Higher rates push revenue from $1.989M in Year 1 to $7.658M in Year 5, so bigger scopes flow straight to owner pay.

3

Retention Mix

20%-85%

More retainer work smooths cash and keeps revenue steadier as advisory mix climbs from 20% to 85%.

4

Delivery Hours

80-120h

Billable hours set capacity, and 80 to 120 hours per project means any idle bench cuts take-home fast.

5

Labor Mix

5-18 FTE

Staffing grows from 5 FTE to 18 FTE, so wage mix and subcontractor use have a direct hit on margin.

6

Data Stack

8.5%-13%

Database and software spend stays near 13% of revenue in Year 1 and 8.5% in Year 5, helping EBITDA margin climb from 23.8% to 41.2% and cutting delivery risk.

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check the owner income model for the Scope 3 Emissions Reporting Service?

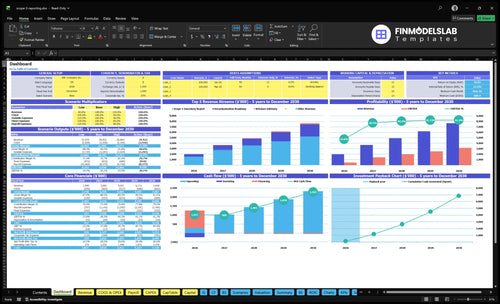

This dashboard shows revenue, EBITDA, owner pay, cash need, breakeven, payback, and IRR tabs across client assumptions, service mix, billable hours, hourly pricing, staffing, marketing, COGS, variable expenses, fixed overhead, capex, owner pay, reserves, and scenario charts. It’s planning support, so open the model.

Owner-income model highlights

Owner pay is built in

EBITDA tracks margin growth

Scenarios compare assumptions

How many Scope 3 reporting clients are needed to pay the owner?

For the Scope 3 Emissions Reporting Service, the owner can’t be paid from client count alone; it depends on contract value, service mix, and how much cash actually gets collected. On paper, 6 inventory reports at $30,000 each, 8 roadmap projects at $24,000 each, or 80 retainer months at $2,250 would reach a $180,000 target before costs. If the $120,000 marketing budget and $12,000 CAC hold, that points to about 10 acquired clients, but labor, software, travel, commissions, overhead, and reserves still have to be paid first.

Gross revenue

6 reports can hit $180,000.

8 roadmaps can hit $180,000.

80 retainer months can hit $180,000.

Higher price means fewer clients.

Cash reality

10 clients fit the CAC math.

$120,000 marketing implies that pace.

Booked revenue is not collected cash.

Costs still come out before pay.

How much can the owner of a Scope 3 reporting service take home?

The owner of a Scope 3 Emissions Reporting Service can realistically start with the modeled $180k Managing Director salary, then add distributions only after cash is collected, reserves are funded, taxes are covered, debt is paid, and reinvestment needs are met. For the operating setup behind this, see How To Launch Scope 3 Emissions Reporting Service?; just don’t treat EBITDA as guaranteed take-home.

Modeled Pay

$180k Managing Director compensation

Solo expert: simpler pay, lower capacity

Year 1 revenue: $1.989M

Year 1 payroll: $655k

Distribution Room

Year 1 EBITDA: $473k

Year 5 revenue: $7.658M

Year 5 payroll: $2.14M

Year 5 EBITDA: $3.154M

Can a Scope 3 reporting service scale without the owner doing all delivery?

Yes — the Scope 3 Emissions Reporting Service can scale without the owner doing every delivery task, but only if delegation is tight. In the model, headcount rises from 2 senior consultants and 1 analyst in Year 1 to 8 senior consultants and 5 analysts in Year 5, while revenue grows from $1.989M to $7.658M and EBITDA from $473k to $3.154M. The owner should shift to scoping, QA, key accounts, hiring, and methodology control, because weak QA can turn added payroll into rework and missed deadlines.

Scale path

Year 1: 3 delivery staff total

Year 5: 13 delivery staff total

Revenue reaches $7.658M

EBITDA reaches $3.154M

Owner’s job

Own scoping and pricing

Review quality before delivery

Manage key accounts directly

Hire and train the team

Key Takeaways

Scope and pricing drive the strongest revenue per engagement.

Retainers smooth cash flow, but low-value work can crowd out.

Utilization matters most when it avoids rework and deadline overruns.

Pricing must cover QA, software, and subcontractor costs.

Compare low, base, and high owner-income cases

Owner income scenarios

Owner income changes fast here because revenue, staffing, and cash reserves do not move at the same speed. Higher sales can still leave take-home modest if payroll and marketing keep scaling.

Compare cautious, modeled, and upside owner pay.

Scenario

Low CaseCash-first

Base CaseModel case

High CaseGrowth case

Launch model

The owner mostly takes the $180k operator salary and protects cash while sales stay light.

This matches the modeled Year 1 case, where owner pay comes from salary plus a limited draw.

This is the mature Year 5 upside case, where stronger revenue supports a larger owner draw.

Typical setup

Client volume stays low, one-off reports do most of the work, and cash stays inside the business for payroll, marketing, and reserves.

Year 1 revenue is $1.989M with $473k EBITDA, a 23.8% EBITDA margin, $655k payroll, $120k marketing, and a $689k minimum cash need.

Year 5 revenue reaches $7.658M with $3.154M EBITDA, a 41.2% EBITDA margin, $2.14M payroll, and $220k marketing while retainer advisory rises to 85%.

Cost drivers

Owner salary

light client load

fixed payroll

reserve buildup

marketing spend

Year 1 revenue

23.8% EBITDA margin

$655k payroll

$120k marketing

$689k cash need

Year 5 revenue

41.2% EBITDA margin

$2.14M payroll

$220k marketing

85% retainer advisory

Owner income rangeBefore owner reserves

$180k - $200kLow income

$220k - $300kModeled income

$400k - $700kUpside income

Best fit

Use this to stress-test slow sales or a cautious owner who wants liquidity first.

Use this as the most likely planning case for the first operating year.

Use this to test a stronger client mix, higher utilization, and a larger owner take-home before taxes.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Scope 3 Emissions Reporting Service Core Six Income Drivers

Average Client Contract Value

Scope 3 Client Contract Value

This driver is the price per engagement, and it’s the biggest lever on owner income. Here’s the quick math: an inventory report at 120 hours × $250 brings in $30,000; a roadmap at 80 hours × $300 brings in $24,000; retainer advisory at 10 hours × $225 per month is $2,250/month if billed monthly.

Take-home rises when scope stays tight and billable time stays billable. Better-scoped supplier data, category calculations, methodology documentation, and reporting support lift revenue quality. The risk is underpricing complex buyers and eating unpaid QA time, which pushes gross margin down even when revenue looks healthy.

Price the work, then protect the hours

Track contract value by project type, billable hours, and effective hourly rate. If a $24,000 roadmap needs extra review or messy data cleanup, the real rate drops fast. Price in QA, define deliverables up front, and use scope changes when supplier data, documentation, or audit support expands.

Track planned vs. actual hours.

Bill QA when scope expands.

Set minimum fees for complex buyers.

Separate advisory from one-time reports.

Delivery Capacity And Utilization

Delivery Capacity

This driver is about turning available analyst and founder time into billable hours without rework. In Year 1, the inventory report takes 120 hours, the roadmap takes 80 hours, and the retainer uses 10 hours; by Year 5, those shift to 100, 100, and 20 hours. If hours slip into unpaid QA or founder bottlenecks, owner pay drops fast.

Here’s the quick math: more usable capacity raises revenue, but only if deadlines hold and quality stays audit-ready. Overselling during reporting peaks can force overtime or contractors, which lifts delivery cost and cuts gross margin. The real target is steady, clean output per project, not the most hours booked.

Track Billable Time, Not Busy Time

Measure billable hours, rework hours, and deadline misses by project type. Use the model shift from 120 to 100 hours on inventory reports and 80 to 100 hours on roadmap work to set capacity by service line, not by guesswork. That keeps pricing, staffing, and owner draw tied to real throughput.

Cap work at clean delivery capacity

Flag QA time before selling

Price overtime into peak months

Protect utilization with a simple rule: if reporting deadlines stack up, pause new work or add paid help before quality slips. That protects cash flow and keeps the owner from working unpaid nights to fix avoidable errors. The goal is repeatable output that supports higher take-home income, not just a fuller calendar.

Software, Data, And QA Costs

Software, Data, and QA Costs

Emissions databases, carbon accounting tools, data management, and quality review protect credibility, but they can eat margin if treated like generic overhead. In Year 1, the model assumes 8% of revenue for emissions database subscriptions and 5% for specialized software, or 13% before QA labor. On a $30,000 inventory report, that is $3,900 in tools alone.

Here’s the quick math: if a small engagement does not carry a minimum fee, the owner pays for data access and review time out of profit. That lowers gross margin, slows cash recovery, and cuts what is left for salary or owner draw. The burden should shrink as work gets more repeatable, but early pricing has to cover the full stack.

Price QA Into Every Engagement

Track tool cost per project, QA hours per deliverable, and revenue per client. Split software, database, and review time by contract type so you can see when a job is too small for the stack. If a project cannot absorb the modeled 13% software and data load plus QA labor, add a minimum fee or raise the hourly rate.

Use pricing to protect take-home income: bake quality review into scope, bill review-heavy work at full rate, and test margin by project size. The risk is simple: expensive tools on a low-value contract can turn a strong report into a thin or negative-margin job.

Labor Mix And Subcontractor Economics

Labor Mix Drives Margin

For this Scope 3 consulting model, labor is the main cost that decides gross margin and owner take-home. The model shows $655k of Year 1 payroll, including a $180k Managing Director, 2 senior consultants at $135k each, a $95k data analyst, and a $110k sales manager. If the team is too fixed for the work won, cash gets tight fast.

The disclosed Year 5 payroll of $214M signals the same risk at scale: more employees can add control and delivery capacity, but solo delivery caps revenue. Subcontractors add flexibility, yet they only help owner income if their cost is built into the bill rate and the contract covers QA time, rework, and deadline spikes.

Price Capacity Before You Add People

Track billable hours by role, loaded cost by role, and utilization (billable time as a share of paid time). That tells you whether each consultant, analyst, or subcontractor is paying for itself. One clean rule: if a role cannot cover its fully loaded cost plus QA, it is not helping owner pay.

Use a simple test on each engagement: revenue per hour minus direct labor cost minus subcontractor cost. For hourly projects, price the work so the labor mix still leaves room for owner draw. If subcontractors are used for peak reporting periods, lock their cost into the scope before the deadline hits, or margin will leak on every rush job.

Track loaded cost by role

Measure utilization weekly

Price QA into contracts

Limit unpaid rework

Match staffing to booked demand

Recurring Revenue And Client Retention

Recurring Retainer Mix

Recurring Scope 3 reporting revenue smooths cash flow and lowers sales pressure. The mix shifts from 20% retainer advisory in Year 1 to 85% in Year 5, while the retainer rate rises from $225 to $280 per hour. That gives the owner more predictable income, but only if retainers stay tied to real advisory work and don’t replace stronger project fees.

Here’s the quick math: a higher retained base means more billed hours come back each period, so collections are steadier and owner draws are easier to plan. The hidden risk is selling low-value retainers that soak up senior time and crowd out one-time inventory reports and roadmap projects, which can reduce total profit even when revenue feels stable.

Manage Retention and Mix

Track retained clients, retainer hours, renewal rate, and retainer revenue share each month. Separate advisory retainers from one-time reports so you can see whether recurring work is truly adding cash flow or just shifting hours away from higher-margin projects. If renewal stays strong, owner income gets less volatile.

Retainer hours sold

Hourly rate

Renewal rate

Project vs retainer mix

Owner draw coverage

Set a floor on pricing and scope so low-fee retainers do not crowd out better work. A clean rule helps: if a retainer needs heavy QA or senior advisory time, it should be priced to protect margin, not just fill calendar time. That keeps recurring revenue useful for cash flow without weakening take-home income.

Sales Positioning And Compliance Demand

Sales Positioning And Compliance Demand

This driver sets how much demand the firm can pull from companies that need Scope 3 emissions help. It depends on customer pain, supply-chain data pressure, disclosure readiness, and audit-ready documentation. If positioning is weak, the team sells less, discounts more, and leaves senior consultants idle; if it’s sharp, close rates and pricing power rise, which lifts owner pay.

Here’s the quick math: marketing budget rises from $120k in Year 1 to $220k in Year 5, so every lead has to convert into paid work. Model client acquisition cost at $12k to $95k and compare it with project margin; if CAC runs too high, cash flow gets tight before payroll does.

Measure Pipeline Quality, Not Just Lead Count

Track qualified accounts, close rate, and average deal value. Also watch how many deals need audit-ready reports, since those buyers usually pay for proof and support better pricing. A strong pitch ties compliance risk to a fixed scope and clear deliverables, so senior staff spend time on the right work instead of chasing low-fit leads.