How Much Seasonal Cleaning Owners Make With $75K Modeled Pay

This guide estimates seasonal cleaning business income using a five-year US model with a $75,000 owner/operator salary, Month 5 breakeven, and $179,000 Year 1 EBITDA It covers revenue assumptions, job mix, labor, supplies, travel, marketing, fixed overhead, reserves, and owner take-home It is not personal tax advice, a guaranteed salary, or an exact distribution plan

Owner income$75kNet margin30%Revenue for target pay$250kBusiness difficultyHard

Want to see the six income drivers?

1

Peak Bookings

Peak fill

Filled spring and fall slots drive the most revenue, so empty weeks hit take-home fast.

2

Ticket Mix

$550+$150

Higher package prices and add-ons lift each job, and small price gains flow straight to owner profit.

3

Crew Efficiency

12%-10%

Keeping direct labor near 12% cuts service cost and lets crews finish more work per day.

4

Repeat Clients

15%-50%

More subscription adoption steadies repeat work between seasons and lowers the need to re-sell every job.

5

CAC Control

$150-$120

Lower customer acquisition cost and digital spend means each booked customer costs less to win.

6

Cash Discipline

$3.2K/mo

Tight control of monthly overhead protects cash through launch capex and gets the business to Month 5 breakeven.

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on booked jobs, margins, payroll, reserves, and overhead.

Want to see the owner income model?

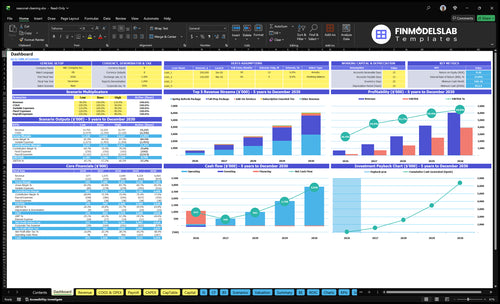

The dashboard shows $75,000 owner salary, Month 5 breakeven, $179,000 Year 1 EBITDA, $703,000 Year 2 EBITDA, and $104,500 initial capex. It also tracks revenue, margin, costs, reserves, and take-home pay in the Seasonal Cleaning Financial Model Template.

Owner-income model highlights

Owner salary and take-home

Revenue, margin, cash

Scenarios and assumption tabs

Can a seasonal cleaning business pay the owner year-round?

Yes, Seasonal Cleaning can pay the owner year-round in the base model: owner salary is $75,000 per year, or $6,250 per month, from Month 1 through Month 60. The catch is timing: breakeven lands in Month 5, so early pay depends on launch cash, booking speed, and tracking What Is The Most Critical Metric To Measure Seasonal Cleaning's Success?. Monthly cash flow will be uneven, with the minimum cash point modeled at $813,000 in Month 2.

Pay Reality

Model includes $75,000 annual owner salary

Monthly owner pay equals $6,250

Breakeven starts in Month 5

Early payroll needs launch cash

Cash Smoothing

Separate salary from bank balance

Save spring and fall surplus

Use pre-booked seasonal packages

Add subscription tiers for steadier cash

Should a seasonal cleaning owner do the work or hire crews?

If Seasonal Cleaning is still small, owner-operated work keeps more margin, but it also caps sales at the owner’s calendar. With $75,000 in owner/operator direct labor modeled at 12% of Year 1 revenue, that points to about $625,000 in revenue before adding crews. Hiring crews opens capacity, but only if booked hours stay full, travel gaps stay low, and reviews stay strong.

Owner-operated

More margin at first

Capped by one calendar

Less scheduling load

Lower rework risk

Crew-led

Year 1 labor: $50,000 lead

Two techs at $35,000 each

Needs tight scheduling

Needs quality control and reviews

What is the profit margin for a seasonal cleaning business?

If you’re pricing Seasonal Cleaning, How Much Does It Cost To Launch Seasonal Cleaning Business? helps frame the spend side, but margin comes from service mix. Year 1 gross margin is 82% after direct service costs, and contribution margin is about 72.5% after 7% digital marketing, 2% payment processing, and 0.5% referral bonuses. Operating profit then depends on $38,400 of annual fixed overhead, and the model shows $179,000 EBITDA in Year 1, not owner take-home.

Margin math

82% gross margin after direct costs.

12% technician wages and benefits.

4% supplies, plus 2% fuel and maintenance.

Contribution margin is about 72.5%.

Profit reality

Subtract $38,400 fixed overhead next.

EBITDA reaches $179,000 in Year 1.

EBITDA is not owner distributions.

Payroll, capex, and reserves still matter.

Key Takeaways

Book peak-season slots early to protect $399 contribution.

Raise average ticket with add-ons and premium packages.

Keep crews busy; labor efficiency drives profit.

Rebook clients before season ends to cut customer acquisition cost.

Compare low, base, and high owner-income scenarios

Owner income scenarios

Income swings with seasonal bookings, add-ons, and crew use. Miss Month 5 breakeven or run CAC above the Year 1 target, and owner pay stays tight; hit mix and scale, and salary support improves.

Low, base, and high cases show how owner income changes as bookings, labor use, and mix improve.

Scenario

Low CaseLean launch

Base CaseStaffed base

High CaseScaled crews

Launch model

Lower earnings path if bookings stay below breakeven and crews are not fully used.

Modeled operating case with the owner salary supported by Year 1 demand and the core service mix.

Stronger earnings path if volume, mix, and labor use improve and EBITDA scales toward Year 2 levels.

Typical setup

Lean launch with slow booking flow, CAC above the Year 1 target, and too much idle labor.

Staffed launch with $550 seasonal packages, 18% direct costs, 95% variable costs, $38,400 fixed overhead, and $75,000 owner salary.

Scaled crews, stronger add-on and subscription mix, and better labor use support the owner salary and push EBITDA toward $703,000 in Year 2.

Cost drivers

Bookings below breakeven

CAC above $150

idle crews

fixed overhead

weak repeat mix

Seasonal package mix

$550 pricing

18% direct costs

95% variable costs

$38,400 overhead

Higher volume

better labor utilization

more add-ons

subscription mix

lower CAC

Owner income rangeBefore owner reserves

Below salary supportCash pressure

$75,000Salary supported

$75,000+Upside case

Best fit

Use this to stress-test owner pay when Month 5 breakeven slips or crew hours stay light.

Use this as the main planning case for an owner who wants a funded salary and a workable operating model.

Use this to test upside when the team fills routes, keeps CAC in check, and uses more recurring work.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Seasonal Cleaning Core Six Income Drivers

Peak-Season Booking Volume

Peak-Season Booking Volume

Spring and fall weeks drive most annual revenue in seasonal cleaning, so the owner’s income rises when those calendars fill early. With Year 1 packages priced at $550, each missed peak slot gives up about $399 of contribution before fixed overhead and payroll, which leaves less room for owner pay and EBITDA.

Here’s the quick math: $399 / $550 = 72.5% contribution per booked peak package. That means booking speed matters as much as lead volume. If the crew has open days, weak route density, or late sales, revenue looks fine on paper but cash flow and profit stay thin.

Book Peak Weeks First

Track filled spring weeks, filled fall weeks, lead time, and gaps between jobs. Those four inputs tell you whether the crew is priced and scheduled well enough to protect owner draw.

Set a simple rule: sell peak slots before demand slips, then build routes to cut dead time. Watch crew availability, route density, and schedule gaps; if any one weakens, you lose contribution and the year-end payout gets smaller.

Count booked peak slots weekly.

Measure days from lead to close.

Track unused crew hours.

Flag gaps by route and zip.

Labor Productivity And Crew Utilization

Labor Productivity and Crew Utilization

Labor efficiency is the main margin control point here. In Year 1, direct technician wages and benefits equal 12% of revenue, and total direct service costs are 18% once supplies and vehicle costs are included, so each $100 of sales leaves about $82 before overhead. With a base crew of one lead technician and two cleaning technicians, travel gaps, rework, and idle time directly cut the owner’s take-home profit.

What this hides is owner labor. If the owner is doing unpaid field work, the margin can look better than it really is. The real test is billable hours per paid hour: more completed work per crew hour means higher EBITDA and more cash left for owner pay.

Measure Billable Hours, Not Just Headcount

Track billable hours, paid hours, travel time, rework, and checklist misses by crew and by job. The key input is utilization: how much of a paid shift turns into paid service time. If a crew is paid for 10 hours but only bills 7, the missing 3 hours are margin leakage that can’t be ignored.

Log billable hours per crew per day

Separate owner hours from crew hours

Review rework and checklist failures

Cut route gaps between jobs

Use these numbers to price jobs, staff routes, and forecast cash. If billable time rises without adding headcount, EBITDA improves fast; if idle time stays high, the business needs more jobs per route or tighter scheduling before owner draws grow.

Marketing Cost Per Booked Job

Marketing Cost Per Booked Job

This driver is the cost to turn a lead into a booked seasonal cleaning job. With a $25,000 annual marketing budget and $150 CAC (customer acquisition cost), the model buys about 167 booked jobs a year before overhead. If CAC falls to $120 by Year 5, the same budget buys about 208 jobs, which lifts contribution and gives the owner more room to pay themselves.

What matters most is not just lead volume, but whether those leads rebook. Digital spend at 7% of revenue, plus referral bonuses starting at 5% and declining to 2%, only help if they cut cost per booked job. The risk is buying one-time jobs that do not return, which pushes CAC up and leaves less cash after payroll and fixed costs.

Cut CAC, Not Just Lead Count

Track cost per booked job by channel: local search, referrals, and paid digital. The clean test is simple: if a channel does not lower CAC below $150 now, or toward $120 later, it is not improving owner income. Also watch rebook rate, because repeat seasonal clients spread acquisition cost over more revenue.

Here’s the quick math: every booking that comes back next season lowers the true CAC per customer. So the goal is not cheap clicks; it is booked jobs that turn into spring and fall repeats. If referral bonuses keep rising while conversion stays flat, marketing spend is leaking margin and shrinking owner draw.

Average Ticket And Service Mix

Average Ticket and Mix

Average ticket is the revenue per job, and here it comes from $550 spring and fall packages, $80 essential subscriptions, $120 premium subscriptions, and $150 add-ons. When the mix shifts toward bigger scopes and more add-ons, revenue rises faster than travel or admin time, so each booking can throw off more cash for owner pay.

The risk is underpricing deep-clean hours. If premium scope or add-ons take more labor than the price covers, contribution per booking drops even when sales look strong. The five-year mix matters too: add-ons rise from 20% to 40%, and premium subscriptions from 5% to 20%, so the owner needs pricing that tracks actual time.

Track Scope, Price, and Time

Measure average ticket by service line and compare it to labor minutes, travel, and admin time. One clean rule: if a job takes longer but the price stays flat, margin leaks out. Track attach rate for add-ons, premium plan share, and revenue per route day so you can see whether higher ticket sales are really lifting take-home income.

Track ticket by service type.

Price deep-clean hours separately.

Watch add-on attach rate.

Test premium bundle uptake.

Update forecasts when mix shifts.

Use the mix to choose which jobs to book first. More $150 add-ons and $120 premium subscriptions should mean fewer jobs needed to cover owner pay, as long as the extra revenue is not eaten by extra labor. That’s the real test: more contribution per booking, not just more bookings.

Operating Costs And Cash Reserves

Operating Costs And Cash Reserves

Even when job margins look strong, fixed overhead of $3,200 per month still comes off the top before owner pay. That overhead covers rent, insurance, software, utilities, accounting and legal, vehicle depreciation, and website costs, so the real question is not just “Did we book work?” but “Did we clear enough cash after fixed bills?”

Here’s the quick math: $104,500 in upfront capex ties up cash before the business feels healthy. Month 5 breakeven helps, but it does not protect against cancellations, slow weeks, or delayed collections. Owner distributions should come after those gaps are funded, or cash crunches will hit fast.

Track Cash, Not Just Profit

Build a reserve that can cover the monthly overhead and short booking dips before taking profit draws. If spring or fall jobs slip, the business still has to pay $3,200 in fixed costs, plus keep vehicles, software, and insurance current.

Track monthly overhead cash burn.

Separate owner pay from reserves.

Watch cancellations by season.

Keep capex cash off-limits.

Use cash forecasting to test bad months, not just average months. A model that clears breakeven can still fail if one slow stretch delays invoices or cuts bookings. The goal is safer year-round pay, not just a paper profit number.

Repeat Seasonal Clients

Repeat Seasonal Clients

Repeat clients turn seasonal demand into planned cash. In Year 1, the mix includes 60% spring package allocation, 55% fall package allocation, 10% essential subscriptions, 5% premium subscriptions, and 20% add-ons. The goal is pre-booked spring and fall work, not a generic maid route.

The owner wins when the next seasonal window is booked before the current job ends. That cuts paid lead spend, improves route density, and makes take-home pay easier to forecast. The main risk is weak rebooking, which forces the business back into expensive lead buying and creates choppy cash flow.

Track Rebook Rate by Season

Measure how many spring jobs are rebooked for fall, and how many fall jobs are locked for spring. Track repeat rate, add-on attach rate, and customer acquisition cost together, because a high repeat rate only helps if it replaces paid leads. If rebooking slips, owner income gets less predictable fast.

Track rebooked jobs before service ends.

Watch seasonal fill rate by route.

Compare repeat sales vs paid leads.

Price add-ons to raise ticket.

Here’s the quick test: if repeat bookings rise and marketing spend falls, more gross profit is left for payroll, overhead, and owner draw. If customers wait until the next season to call, demand gets spiky and the calendar gets harder to plan.