How Much Self-Storage Investment Owners Make Over 60 Months

You’re underwriting cash flow before the portfolio is stable, so owner income should be planned as distributions, not a fixed salary This 60-month self-storage investment income view uses researched assumptions including $290M in owned-facility purchases, $1425M in construction budgets, Month 36 breakeven, and Month 59 payback It covers revenue, NOI, debt, reserves, and take-home planning, but not taxes or guaranteed payouts

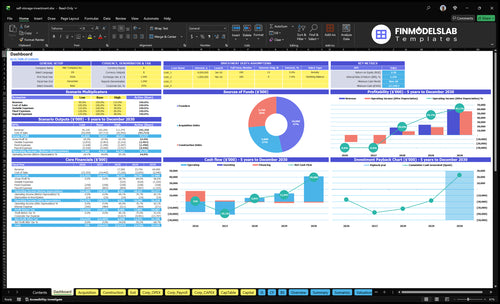

Owner incomeYr 5 $55.3MNet marginN/MRevenue for target payMonth 36Business difficultyHard

Want to test your self-storage owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income can change with taxes, depreciation, appreciation, refinancing proceeds, debt terms, and investor payouts. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to stress-test owner income in the Self-Storage Investment model?

How much does a self-storage facility owner make per year?

A self-storage facility owner doesn’t make a fixed yearly salary; take-home depends on cash flow after debt, reserves, lease payments, and distribution rules. In the Self-Storage Investment model, a $200,000 managing partner salary can sit in payroll, but distributions should wait until obligations are covered; see What Is The Current Growth Trajectory Of Your Self-Storage Investment Portfolio? because EBITDA, or earnings before interest, taxes, depreciation, and amortization, is not owner take-home.

Modeled annual income

Year 1 EBITDA: -$16.274M

Year 2 EBITDA: -$20.522M

Year 3 EBITDA: $8.578M

Year 5 EBITDA: $55.258M

What changes pay

Raise occupancy and achieved rent

Control construction timing risk

Fund debt and reserves first

Test refinancing and lease assumptions

Is it more profitable to buy or build self-storage?

For Self-Storage Investment, buying is usually the faster path to cash flow when occupancy and rent are already proven, while building can create more upside but adds lease-up, financing, and construction risk. In the research plan, owned acquisitions total $290M versus $1,425M in construction budgets, so the mix leans hard toward build risk. There’s no universal winner: buy for speed, build for upside.

Buying cash flow

Proven occupancy cuts ramp risk.

Rents start faster, so cash starts faster.

Owned acquisitions total $290M.

Best when you want earlier distributions.

Building upside

Higher upside, but more moving parts.

Construction budgets total $1,425M.

Build time runs 6 to 20 months.

Rented-site costs hit $45k per month at full rollout.

Risk timing

Lease-up risk can delay revenue.

Financing adds pressure before stabilization.

Cash trough shows -$27358M in Month 35.

Breakeven arrives in Month 36.

Owner economics

Active sponsors earn payroll or fees.

Passive investors rely on distributions.

Builds reward patience, not speed.

Buy deals fit income-first goals.

What is a good profit margin for self-storage?

A good profit margin for Self-Storage Investment is best judged at the property level with NOI margin before debt and owner payouts, not at corporate EBITDA; for cost context, see What Is The Estimated Cost To Open, Start, And Launch Your Self-Storage Investment Business?. Here’s the quick screen: measure operating costs like property taxes, insurance, utilities, repairs, software, security, payroll, marketing, third-party management fees, and lease payments, then test cash flow after debt service and reserves. The catch is simple: $215k in monthly fixed overhead plus wages rising from $560k in Year 1 to $850k in Year 5 can erase strong margins if debt load, lease-up delays, or construction overruns absorb cash.

Margin test

Use NOI margin first

Exclude debt and distributions

Track property-level operating costs

Check corporate EBITDA separately

Cash risk

Stress-test debt service

Reserve cash for repairs

Watch lease-up timing

Watch construction overruns

Want to see what drives self-storage owner income?

1

Lease-Up

Month 36

Breakeven lands in Month 36, so faster unit fill is the quickest way to pull owner income forward.

2

Capital Stack

-$27.4M

The model bottoms at about negative $27.4M in cash, and payback takes 59 months, so funding terms decide if the plan survives the build.

3

Portfolio Scale

$43.25M

Modeled purchase and construction spend totals about $43.25M, which sets the asset base that later drives EBITDA growth.

4

Rent Mix

High

Achieved rents and unit mix drive revenue per occupied foot, so better pricing lifts income without adding much cost.

5

Team Cost

$560K-$850K

Payroll rises from about $560K in Year 1 to $850K in Year 5, and that sits on top of $215K a month in fixed overhead.

6

Fee Drag

2.2%-4.5%

Deal execution and investor reporting costs take 2.2% to 4.5% of revenue, so lean processes protect take-home as the platform scales.

Self-Storage Investment Core Six Income Drivers

Occupancy and Lease-Up

Lease-Up and Occupancy

Lease-up turns empty units into rent, so it drives effective gross income, net operating income (NOI), debt coverage, and the cash the owner can actually take out. Track both physical occupancy (units rented) and economic occupancy (rent collected after discounts and concessions); if discounts rise, the property can look full and still miss cash.

Here’s the quick math: slower lease-up delays distributions and widens the cash gap while the asset stabilizes. With construction runs of 6 to 20 months, revenue timing should lag completion risk; the Month 35 minimum cash of -$27358M shows how timing can dominate early returns.

Track Lease-Up, Not Just Headcount

Measure occupancy, lease-up pace, monthly move-ins, renewals, and concession rate together. A unit that rents fast but needs heavy discounts can hurt economic occupancy and owner pay, even if physical occupancy looks strong.

Track physical and economic occupancy

Watch discount and concession burn

Stress test slower lease-up months

Delay draws until cash stabilizes

Build the forecast from unit count, rent per unit, and the rent collection rate. If lease-up slows, push distributions later and protect reserves; that keeps debt coverage from slipping when the property is still filling.

1

Achieved Rent and Unit Mix

Achieved Rent and Unit Mix

If your facility is full but cash still feels thin, achieved rent is usually the reason. It is the rent you actually collect per unit and per rentable square foot after concessions and discounts. Unit mix also matters: climate-controlled and drive-up units, plus size mix, set the pricing ceiling before property expenses, debt, and reserves.

Track average rent, rent per square foot, concessions, discounts, and rent increases by unit type. Discounting can lift physical occupancy while lowering economic occupancy, so the property looks busy but earns less. Do not treat national averages as a guarantee; local supply and tenant demand decide pricing power.

Measure Rent Mix by Unit Type

Build the forecast from signed rents, not asking rents. Test each unit type separately, then watch whether higher rates lift revenue per rentable square foot more than they raise move-outs. The quick check is simple: more rent per square foot helps cash flow only if occupancy and renewals stay solid.

Measure the gap between physical and economic occupancy every month. If concessions rise, cash collected falls even when units are rented. That gap hits gross income first, then NOI, and then the owner’s ability to take distributions.

2

Facility Scale and Market Demand

Facility Scale vs. Demand

Facility size sets the revenue ceiling. More rentable square feet and unit count can create more gross rent, but only if the local market fills those units at supportable rates. If demand is weak, the extra space just adds carrying cost and delays cash that would otherwise reach the owner.

Here’s the quick math: this plan adds assets from Month 3 through Month 24 and construction from Month 6 through Month 30, so capacity comes online before it stabilizes. A $290M purchase plan plus $1,425M in construction only works if occupancy and rates follow; bigger assets need more capital up front, so slow lease-up cuts owner distributions fast.

Track Demand Before You Scale

Measure location, traffic visibility, population growth, household density, and competing supply before you buy or build. Those inputs tell you whether added square feet can turn into cash, or just sit empty and drag on profit.

Use a simple test: if the market can’t absorb new units while keeping pricing firm, slow the next acquisition or phase of construction. That protects NOI before debt, reserves, and owner pay get squeezed by vacant space.

3

Operating Expense Control

Control Operating Expenses

Operating expenses reduce NOI before debt, reserves, or owner distributions. In this model, monthly fixed overhead is $215k, wages rise from $560k in Year 1 to $850k in Year 5, and variable deal and reporting costs fall from 45% to 22%. That means early profit is most exposed to fixed cost creep, especially before rent and occupancy ramp.

Track property taxes, insurance, utilities, repairs, software, security, payroll, marketing, and management fees as separate lines. Each $1 saved in operating expense adds $1 to NOI, but that does not fix weak rent collection or slow lease-up. The risk is blunt: if revenue lags, fixed costs can delay distributions and squeeze owner take-home income.

Tighten the Expense Run-Rate

Separate operating expenses from debt service and capital reserves, then review actuals against budget every month. Use the disclosed cost buckets to test where the leak is: payroll, vendor fees, marketing, or facility operations. If a line grows faster than revenue, it is not scale; it is margin loss.

For planning, use the Year 1 to Year 5 drop in variable costs, from 45% to 22%, as the target shape of efficiency. If the platform cannot pull fixed overhead down as revenue rises, owner income stays trapped below NOI even when assets perform well. Keep reserve funding separate so operating savings are not confused with cash available for draws.

4

Financing Structure

Debt Mix and Exit Timing

Financing structure decides how much NOI becomes owner cash after operations, not the property’s core profit model. On $290M of purchases, the cash can bottom at -$27,358M in Month 35 if leverage is too high or the exit slips. Higher leverage can lift equity returns when NOI grows, but it also raises debt service and can delay distributions.

Purchase price and loan size

LTV, rate, and amortization

DSCR = NOI / debt service

Refinance terms and timing

Exit month and sale proceeds

Stress Test Cash First

Track monthly debt service against stabilized NOI and a minimum cash floor. If the loan pushes DSCR below lender limits, owner draws get squeezed fast. Financing cannot fix weak occupancy or low rent, so use lower leverage or longer amortization only if the asset can still cover payments.

Re-run the downside case with slower lease-up and a later sale. If the cash trough approaches -$27,358M in Month 35, cut leverage, add reserves, or delay refinance assumptions before closing.

5

Ancillary Income and Reserves

Ancillary Income and Reserves

Ancillary income lifts cash flow, but rent still pays the bill. Tenant insurance, admin fees, late fees, truck rentals, locks, and deposits can improve owner distributions if occupancy is strong and discounts stay tight. If fees rise because service is useful, margin improves; if fees replace rent, the model gets fragile.

Measure it from occupied units, fee take-up, late-pay volume, and average fee per transaction. Track each source separately so you can see whether cash is coming from real demand or from pressure on tenants.

Tenant insurance

Admin fees

Late fees

Truck rentals

Locks and deposits

Reserve Cash First

Capex reserves and repair reserves cut near-term payouts, but they protect the asset and the owner’s future income. That matters when construction budgets total $1425M and setup capex is $190k; paying out too much before stabilization can widen the funding gap and force a later cash call.

Use a reinvestment policy that keeps cash inside the deal until repairs, replacements, and upgrades are covered. Reserve first, distribute second. If the balance gets thin, slow owner draws before the next problem shows up in operating cash.

Track reserve balance monthly.

Test payouts after weak months.

Link draws to stabilization.

6

Compare low, base, and high self-storage owner income cases

Owner income scenarios

Owner income swings hard here because the model is capital-heavy, timing-sensitive, and distribution-dependent. Lease-up speed, rent strength, expense control, and reserve needs drive the gap between loss years and paid-back years.

Low, base, and high cases show how fast cash can turn from negative to distributable.

Scenario

Low CaseDownside case

Base CaseModeled path

High CaseUpside case

Launch model

Owner income stays weak while the portfolio leases up slowly and distributions remain delayed.

Owner income follows the modeled path as EBITDA moves from -$16,274k in Year 1 to $55,258k in Year 5.

Owner income improves faster when lease-up is quicker and the portfolio reaches stronger cash flow sooner.

Typical setup

Occupancy builds slower, achieved rent is softer, expenses run higher, debt service and reserves stay heavy, and the owner mainly funds the gap.

The portfolio follows the researched model, reaches breakeven in Month 36, and pays back in Month 59 as scale improves and fixed costs get spread out.

Occupancy ramps faster, achieved rent holds up better, expenses stay tight, reserves are controlled, and distributions start earlier.

Cost drivers

Slower occupancy

weaker rent

higher expense ratio

heavier debt service

larger reserves

Modeled EBITDA path

breakeven in Month 36

payback in Month 59

fixed overhead spread

staged acquisitions

Faster lease-up

stronger achieved rent

tighter expenses

controlled reserves

earlier distributions

Owner income rangeBefore owner reserves

No distributionsLoss and delay

-$16,274k to $55,258kModel path

Faster positive cash flowUpside cash

Best fit

Use this to stress-test a slow lease-up and a long wait for cash to reach the owner.

Use this as the main planning case for budgeting, hiring, and capital timing.

Use this to test what happens if the portfolio scales cleanly and cash turns positive faster than planned.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.