How Much Does a Shaved Ice Stand Owner Make? $96K Year 1 EBITDA

You’re estimating owner income for a shaved ice stand, not a fixed paycheck In the provided five-year model, the stand reaches $96k EBITDA in Year 1, $289k in Year 2, and payback in 18 months, before personal taxes, debt service, reinvestment, and owner reserves

Owner income$96k-$289kNet margin15%-32%Revenue for target pay$917kBusiness difficultyHard

Want the six shaved ice income drivers?

1

Daily Cups

80-200/day

Moving from 80 to 200 cups a day is the biggest swing in owner take-home before taxes and reserves, because fixed payroll and rent stay mostly flat.

2

Labor Coverage

$290K

Year 1 payroll is about $290K, so overstaffing on slow shifts cuts profit fast and tight schedules protect cash.

3

Average Ticket

$13-$20

Midweek tickets at $13 and weekend tickets at $20 lift cash per guest, so mix matters almost as much as foot traffic.

4

Weather Days

Seasonal

Traffic is weather-driven, so rain or weak heat can shrink the number of good sales days and pull down take-home.

5

Cost per Serving

15%

Food and drink ingredients run near 15% of sales, so syrup and ice waste hits margin on every cup.

6

Rent & Fees

$7.5K/mo

Rent is $7,500 a month, and any event or site fee has to be covered before the owner sees profit.

Want to test your shaved ice stand income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, operating costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice, and it excludes debt guarantees and personal living costs.

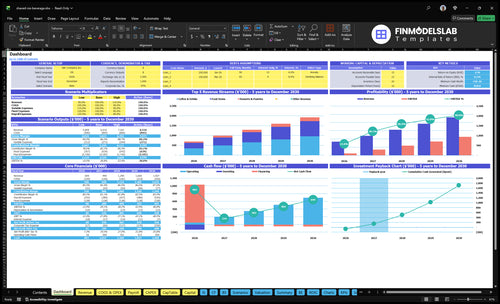

Can you check owner income in the Shaved Ice Stand model?

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions—open the Shaved Ice Stand Financial Model Template to test assumptions, not prove earnings.

Owner-income model highlights

$96k / $289k EBITDA

$829k Month 2 cash need

Month 4 breakeven, 18-month payback

Is a shaved ice stand a good side business?

It can work as a side business only if you cover the peak hours and keep labor tight; this model looks more like a staffed kiosk, with Year 1 payroll around $290k. Owner-run hours can lift sales, but they also hide unpaid work. Weather, school calendars, and event timing decide whether it feels like a side hustle or a full operating job.

When it works

Run hot-day peak shifts.

Keep labor owner-light.

Focus on events and weekends.

Use fast service to boost turns.

What can break it

$290k payroll is heavy.

Staffed hours cut margin.

Rain and cold crush demand.

School timing changes traffic.

What is the shaved ice profit margin?

The Shaved Ice Stand profit margin can look strong on paper, but owner pay is not included in year 1, so the real test is whether traffic covers staffing and overhead; if you also need launch spend, see What Is The Estimated Cost To Open And Launch Your Shaved Ice Stand Business?. Using the provided model, ingredient cost is 150% of sales and card fees plus marketing add 45%, leaving about 805% before labor, rent, utilities, insurance, permits, repairs, cleaning, and services. Fixed costs are $10,650 per month, and payroll starts at about $290k a year, so heavy staffing or weak foot traffic can wipe out the margin fast.

Key numbers

150% ingredient cost of sales

45% fees and marketing load

$10,650 fixed cost per month

$290k starting annual payroll

Margin risk

Owner pay is not included

Labor can crush margin fast

Weak traffic hurts quickly

Overhead matters more than product margin

How much can you make with a shaved ice stand?

A Shaved Ice Stand can make about $96k in Year 1 EBITDA on roughly $749.8k revenue, rising to about $941k EBITDA on $1.92M revenue by Year 5 if traffic and margins hold; for the main growth lever, see What Is The Most Important Factor Driving Growth For Shaved Ice Stand?. Owner income is not the same as EBITDA, because debt payments, taxes, working capital, and owner salary can still reduce cash taken home.

Profit math

Year 1 revenue: about $749.8k

Year 1 EBITDA: about $96k

Year 5 revenue: about $1.92M

Year 5 EBITDA: about $941k

What drives it

80 orders on Mondays in Year 1

200 orders on Saturdays in Year 1

High traffic must cover rent and labor

Events help only after added fees

Key Takeaways

Traffic drives revenue, but only if costs stay controlled.

Pricing lifts profit fastest when value feels clear.

Lost weekend open days hurt more than weekdays.

Fixed costs and labor decide your break-even speed.

Compare low, base, and high shaved ice stand income scenarios

Owner income scenarios

Owner income moves with traffic, weekend pricing, and fixed labor. This table shows a cautious start, a modeled mid-case, and a stronger scale case.

Low, base, and high cases for owner take-home planning.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Lower income path if traffic stays soft while rent and labor still run.

Modeled mid-case once weekday traffic and weekend sales settle into a steady run rate.

Stronger earnings path if volume keeps rising and weekend pricing holds.

Typical setup

Year 1 runs 910 weekly orders, $13 midweek AOV, $20 weekend AOV, about $804k revenue, 85% gross margin, and $96k EBITDA.

Year 3 reaches 1,365 weekly orders, $15 midweek AOV, $22.5 weekend AOV, about $1.37M revenue, 86% gross margin, and $494k EBITDA.

Year 5 reaches 1,900 weekly orders, $16.5 midweek AOV, $24 weekend AOV, about $2.04M revenue, 87% gross margin, and $941k EBITDA.

Cost drivers

910 weekly orders

$13 midweek AOV

$20 weekend AOV

85% gross margin

fixed rent and labor

1,365 weekly orders

$15 midweek AOV

$22.5 weekend AOV

86% gross margin

fuller staffing

1,900 weekly orders

$16.5 midweek AOV

$24 weekend AOV

87% gross margin

stronger weekend mix

Owner income rangeBefore owner reserves

$96kLow Case

$494kBase Case

$941kHigh Case

Best fit

Use this to stress-test cash flow if launch traffic is slower than planned.

Use this as the main planning case for a stable operating year.

Use this to test upside if the stand wins repeat visits and peak-day demand.

!

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; owner take-home will be lower after reserves, taxes, debt service, and reinvestment.

Shaved Ice Stand Core Six Income Drivers

Traffic And Cups Sold Per Day

Traffic And Cups Sold Per Day

This driver is the largest revenue lever because every extra cup sold adds ticket revenue before ingredient and other variable costs. In Year 1, the model runs from 80 Monday orders to 200 Saturday orders, with about 910 weekly orders; that spread shows how much weekends and hot-weather events matter to cash flow and owner pay.

What this estimate hides is the demand swing risk. Parks, pools, beaches, schools, festivals, and summer events can lift volume, but rain, heat swings, short hours, and slow service cap sales. Higher traffic only raises EBITDA if labor and site costs do not rise faster than the extra cups sold.

Track Cup Count by Daypart

Measure orders per day, cups per hour, and sales by site. Here’s the quick math: more cups should push revenue up first, then ingredients, cups, syrup, and labor take their cut. If traffic rises but line speed drops, the stand may sell less than it could on the same hot day.

Use a simple weekly sheet for Monday through Saturday volume, plus weather, event type, and service time. If Saturday volume is near 200 orders but a rainy day falls far below 80 orders, staffing and open-hours plans need to match demand so the extra traffic turns into profit, not overtime.

Track orders by day and location.

Watch speed when lines build.

Match labor to peak hours.

Test events that lift cup count.

Protect margin from slow service.

Labor Coverage And Owner Hours

Labor Coverage

Year 1 payroll is about $290k, or roughly $24.2k a month. That makes labor the biggest controllable cost after sales volume. If staffing is too heavy for the day’s traffic, profit per open hour drops fast. If the owner covers shifts, cash draw can improve, but that time is still labor and should be priced into target pay.

Weekends can justify more staff because higher traffic can absorb the extra cost. Employee-run shifts can extend hours, but they also add training, supervision, and slower-service risk. The key test is simple: does each staffed hour sell enough cups to cover labor and still leave margin for the owner?

Schedule To Sales

Track cups per labor hour, payroll as a share of sales, owner hours, and profit per open hour. Here’s the quick math: $290k / 12 = about $24.2k per month, so small staffing errors add up fast. If a shift does not cover its own labor, it is taking income from the owner.

Staff up on weekend peaks.

Keep weekday coverage lean.

Count owner time as paid labor.

Measure wait time and speed.

If service slows when the team is thin, you lose cups and repeat orders. If labor is too heavy, the stand stays open longer but pays the owner less. Better scheduling means more of each open hour turns into take-home income.

Cost Per Serving And Gross Margin

Cost Per Serving

This driver is the cost to make one cup: syrup, ice, cups, spoons, napkins, toppings, spoilage, and waste. The Year 1 input says ingredients equal 150% of revenue, so gross margin on that math is -50% before labor, fees, and rent. At that level, owner pay gets squeezed fast.

The plan also shows an 85% gross-margin benchmark before fees and overhead, but that conflicts with the 150% cost line. One sloppy pour can erase the profit from several cups.

Protect Margin Per Cup

Build a cost card for each size and update it when suppliers change prices. Split food and beverage recipes into separate cards, then track contribution per cup by watching syrup ounces, ice fill, toppings, cupware, and waste. If the recipe drifts, fix it before the shift ends so the owner’s draw does not get hit.

Weigh pours, don’t eyeball.

Charge for extra toppings.

Log spoilage by event.

Review cost cards weekly.

Pricing And Average Ticket

Average Ticket

Higher average order value (AOV) lifts revenue without adding a full extra cup. In Year 1, AOV is $13 midweek and $20 on weekends, so premium sizes, toppings, cream add-ons, and bundles matter. At 910 weekly orders, even a $1 ticket lift adds about $910 a week before extra variable cost; the ceiling is set by what nearby customers will pay.

Raise Ticket, Not Friction

Track AOV by day, add-on rate, and bundle mix, then test one price move at a time. Event pricing can support a higher weekend ticket, but local competition and line speed set the limit. The Year 5 sensitivity figures shown as $1650 and $2400 should be checked before use in a forecast.

Season Length And Open Days

Season Length And Open Days

When the stand is open fewer days, revenue drops faster than the calendar suggests because the best sales sit on hot weekends and event days. The model’s weekly order pattern, built across five years, still reaches Month 4 breakeven only if peak days are captured. Missing Saturday and Sunday hurts more because those days carry the heaviest traffic and ticket size.

This driver includes planned open days, season length, and missed-day risk from rain, cold fronts, smoke, storms, and short staffing. School breaks, festivals, pool schedules, and local climate shift demand, so forecast by day type, not just by month. Fewer high-traffic days lowers cash in and can push owner pay out of reach.

Protect Peak Open Days

Track open days by weekday and weekend, then compare cups and average ticket by day type. The key test is simple: if a closure removes a high-traffic day, does the lost gross profit still cover the labor or cleanup saved? If not, stay open.

Log planned and missed open days.

Split data by weekday and weekend.

Track weather, events, and school breaks.

Back up staff for peak days.

Protect the busiest days first. A lost weekend can cut more profit than several slow weekdays, so set weather rules, staffing backups, and a cash buffer before peak season starts.

Rent, Event Fees, And Fixed Costs

Rent and Fixed Site Fees

$10,650 in monthly fixed costs is the floor the shaved ice stand must clear before owner pay. Rent is the biggest line at $7,500, then utilities at $1,200, insurance at $300, software at $250, repairs at $350, cleaning at $500, permits at $150, and professional services at $400.

Rent alone is about 70% of fixed costs, so the site fee drives the sales target. High-traffic spots only work when extra cups cover the fee; otherwise, the location raises EBITDA pressure and cuts cash available for the owner. Slow weather makes that tradeoff worse.

Track Fee per Cup

Measure each site by added cups, not just foot traffic. A premium park, event, or concession spot should show enough extra volume to pay its rent and any storage or commissary cost before it touches owner income. One clean rule: if the site fee does not buy more cups, it is too expensive.

Track rent, fees, and cups

Test payback by location

Cut slow-weather premium sites

Protect cash before owner draw

Use the $10,650 base as the hurdle in every forecast. If a location adds cost but does not lift average daily cups, it lowers profit even when sales look busy. The right site fee improves cash payback because the stand keeps more margin after fixed costs.