How Much Does A Small Restaurant Owner Make? $100K Salary Model

You’re sizing owner pay for a limited-seating restaurant, where sales can look strong but cash still gets tight This five-year model uses $100,000 owner/GM salary, Month 14 breakeven, revenue, margins, expenses, reserves, and owner-role assumptions It excludes tax advice, guaranteed salary claims, and exact local cost estimates

How much revenue does a small restaurant need to pay the owner?

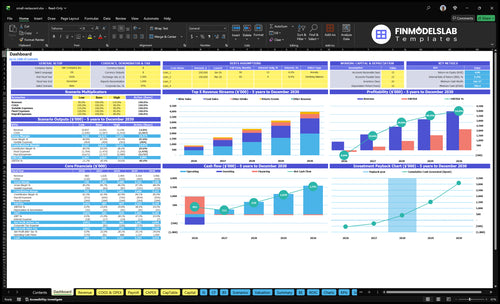

To pay the owner $100,000 a year, or about $8,333 a month, Small Restaurant needs enough sales to cover that salary and still leave room for operations. In the provided model, Year 1 revenue is about $101M, or $84,000 per month, but EBITDA is still -$151,000; breakeven arrives in Month 14 as volume improves. By Year 2, revenue rises to about $171M, or $143,000 per month, with $383,000 EBITDA after owner salary, so pay should be set apart from cash reserves and reinvestment.

Owner pay target

$100,000 yearly owner salary

$8,333 monthly owner pay

Keep pay separate from reserves

Use cash flow, not revenue alone

Revenue timing

Year 1 revenue: $101M

Month 1 average: $84,000

EBITDA in Year 1: -$151,000

Breakeven: Month 14

How much does a small restaurant owner make after expenses?

A Small Restaurant owner makes the planned $100,000 salary in this model, but safe owner draws depend on cash left after expenses; see What Is The Current Growth Trajectory Of Small Restaurant's Customer Base? because covers drive the whole profit picture. Year 1 EBITDA is -$151,000, so extra distributions aren’t supported; Year 2 EBITDA is $383,000 after owner salary, before taxes, debt service, capex, and reserves.

Owner Pay

Planned salary: $100,000

Year 1 EBITDA: -$151,000

Year 2 EBITDA: $383,000

Extra draws: not safe in Year 1

Expense Base

Rent: $12,000 per month

Includes food and beverage cost

Includes wages and payroll taxes

Includes utilities, insurance, repairs, software, reserves

What small restaurant profit margin supports owner take-home?

With seating capped, a Small Restaurant supports owner take-home only after margin turns meaningfully positive, not just “busy.” In Year 1, COGS is 150% of sales and variable expenses add 40%, so EBITDA margin is -149%; by Year 2, it improves to 224%. If you’re mapping startup spend, see How Much Does It Cost To Open A Small Restaurant? because every 1% of revenue is about $10,100 in Year 1 and $41,500 in Year 5.

Year 1 math

COGS runs at 150% of sales

Variable expenses add 40%

EBITDA margin is -149%

Owner take-home is still negative

What moves cash

Year 2 EBITDA margin reaches 224%

Each 1% of revenue matters fast

Food cost shifts take-home materially

Waste, labor, pricing, events change results

Key Takeaways

Table turns set the revenue ceiling.

Average check lifts revenue without adding seats.

Labor and rent pressure margins fastest.

Cash reserves carry the business through slow months.

Compare low, base, and high owner-income scenarios for planning

Owner income scenarios

Owner income changes fast with guest count, check size, and staffing. Early ramp years can stay loss-making, while fuller weeks push modeled earnings much higher.

Low, base, and high cases show how volume and check size shape owner income.

Scenario

Low CaseLow income

Base CaseBase income

High CaseHigh income

Launch model

This is the downside path, with a Year 1 ramp and no safe cash beyond the owner's salary.

This is the modeled operating path, where rising covers and check size support positive owner income.

This is the upside path, with strong traffic and higher checks driving much larger modeled owner earnings.

Typical setup

Year 1 runs at 250 weekly covers and a $7,780 blended check, with EBITDA at -$151,000 and no extra owner draw.

Year 2 reaches 382 weekly covers and an $8,619 blended check, with EBITDA at $383,000 after owner salary.

Year 5 reaches 725 weekly covers and an $11,017 blended check, with EBITDA at $2,142,000 after owner salary.

Cost drivers

250 weekly covers

$7,780 blended check

-$151,000 EBITDA

owner salary only

no safe extra draw

382 weekly covers

$8,619 blended check

Year 2 scale-up

$383,000 EBITDA

owner salary absorbed

725 weekly covers

$11,017 blended check

Year 5 volume peak

$2,142,000 EBITDA

strongest cover density

Owner income rangeBefore owner reserves

$100,000 salary onlySalary only

$383,000 after salaryModeled profit

$2,142,000 after salaryPeak upside

Best fit

Use this to stress-test cash strain when traffic is light and the owner stays on salary only.

Use this as the planning case for normal growth, stable staffing, and a functioning week-to-week run rate.

Use this to test the best case when the room is full more often and pricing power holds.

!

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets.

Small Restaurant Core Six Income Drivers

Seating Capacity And Table Turns

Table Turns

Table turns decide how many guests a fixed room can serve, so they set the revenue ceiling. Modeled weekly covers rise from 250 in Year 1 to 725 in Year 5, with Saturday climbing from 75 to 200 covers and Monday from 10 to 45.

Income improves when filled seats, reservation discipline, fewer no-shows, tighter service pacing, and smart operating days keep the room busy. If midweek demand stays weak, fixed costs like $12,000 monthly rent and $24,500 fixed overhead get spread over too few checks, which cuts cash flow and owner draw.

Track Turns, Not Just Seats

Track covers by day, turn rate, average dining time, and no-show rate. Here’s the quick math: a Saturday target of 200 covers only works if the room resets fast enough and reservations land on time. One clean rule: fill seats before adding hours.

Watch Saturday and Monday separately.

Use deposits to cut no-shows.

Stagger reservations to smooth pacing.

Close weak days if demand misses plan.

Test tighter seating windows on busy nights and shorter hours on slow ones. If Monday demand stays near 10 covers, labor and rent are underused; if it reaches 45 covers, the same staff can support more profit and a better owner draw.

Cash Reserves And Owner Draw Policy

Cash Reserve Discipline

Cash reserves decide how much the owner can safely take home. In this model, minimum cash reaches $396,000 in Month 13, breakeven lands in Month 14, and payback comes in Month 31, so profit alone is not enough; the business still needs cash for slow periods, repairs, debt service, and reinvestment.

The owner’s draw should sit below available cash, not accounting profit. Keep $100,000 salary, owner draw, taxes, debt payments, and retained cash separate. With $410,000 of startup capex already tied up, a bigger draw can drain the restaurant even when the P&L looks fine.

Track Cash Before You Pay Yourself

Measure cash weekly and forecast 13 weeks ahead. Here’s the quick filter: pay salary first, then check whether cash stays above the reserve floor after taxes, debt service, and known repairs. If cash falls below the Month 13 minimum, the draw is too high.

Track available cash, not profit.

Separate salary from owner draw.

Hold a repair and debt buffer.

Review reserves every month.

Average Check And Menu Mix

Average Check And Menu Mix

Average check is the spend per guest ticket. In this model, blended check moves from $7,780 in Year 1 to $11,017 by Year 5, while midweek check rises from $65 to $95 and weekend check from $85 to $120. That lifts revenue without adding seats, so each higher ticket can flow through faster than new traffic.

Menu mix is the share of appetizers, entrees, desserts, wine, other drinks, specials, and private events in the ticket. The owner’s income improves when high-margin items make up more of sales, but a blanket price hike can hurt value, slow repeats, and leave labor and spoilage too high for the revenue gained.

Raise Check With Better Mix

Track check by daypart, item mix, and attach rate on wine, desserts, and specials. Here’s the quick math: if covers stay flat and check rises, revenue rises; if food and labor costs rise with the higher ticket, owner pay may not. Price around guest value, then test small lifts on the items that already sell well.

Watch midweek and weekend checks.

Measure add-on item attachment.

Test pricing by menu section.

Protect margins on private events.

Use menu engineering, the practice of ranking dishes by profit and popularity, to keep margin in view. Push profitable items, trim weak sellers, and update forecasts when guest mix shifts. If a price change lowers traffic or slows table turns, roll it back fast; revenue quality matters more than a higher menu number.

Occupancy And Fixed Overhead

Occupancy and Fixed Overhead

In a limited-seating restaurant, rent and fixed overhead set the floor for owner pay. With $12,000 monthly rent, or $144,000 a year, rent alone is about 142% of Year 1 revenue and about 35% of Year 5 revenue. Total fixed monthly overhead is $24,500, so sales must rise fast enough to cover the room before the owner can draw profit.

Here’s the quick math: rent is almost half of fixed overhead, and it turns into a cash drag if table turns stay low. If Monday and other weak days do not fill seats, the business still owes rent, utilities, insurance, permits, software, cleaning, accounting, music, and payroll taxes. High rent is only safe when covers and average check can carry it.

Track fixed burn weekly

Measure rent as % of sales, total fixed overhead, and sales per open day. The key inputs are monthly rent, utilities, insurance, permits, software, cleaning, accounting, music, payroll taxes, covers, and average check. If sales do not outpace $24,500 a month, owner pay gets squeezed before growth has a chance to show up.

Watch sales per seat each week.

Cut weak days if demand is thin.

Match hours to traffic patterns.

Protect table turns on busy nights.

What this estimate hides: a small room can look busy and still miss profit if fixed costs stay too high. The fix is not just more traffic; it is enough traffic at the right check size to absorb the rent and keep cash left for the owner.

Food, Beverage, And Gross Margin Control

Food And Beverage Margin Control

Food cost, beverage margin, and menu mix decide gross profit before payroll, rent, debt, and owner pay. In this model, COGS falls from 150% of sales in Year 1 to 120% in Year 5, so small waste, spoilage, or over-portioning can still wipe out cash. Gross margin is not net profit or owner take-home; it is the money left after food and drink costs.

The key inputs are purchase price, recipe cost, portion size, spoilage, comps, wine mix, and private event pricing. Wine sales rise to 500% of Year 1 sales and stay at 450% by Year 5, while private events move from 50% to 100%, so beverage and event pricing can change income fast if margins hold.

Track Plate Cost, Pour Cost, And Waste

Use recipe costing on every core item, then compare it to actual invoices and sales mix each week. A one-line rule: sell what you can cost, and cost what you sell. If the menu changes, update margins before the next service, not after month-end. That keeps owner pay from getting eaten by hidden cost drift.

Track food cost percentage weekly

Measure wine pour cost by bottle

Flag spoilage and comped items

Test menu items by margin

Price events on full cost

If portion control slips or spoilage rises, gross profit drops first, then cash available for payroll and draws. Tight purchasing and menu engineering protect the spread between sales and COGS, which is the part that funds the owner.

Labor Cost And Scheduling

Labor Cost and Scheduling

Labor includes the owner/GM, head sommelier, head chef, servers, bartenders, kitchen staff, and host/support. In Year 1, wages are $495,000, plus $8,250/month in payroll taxes and benefits, or $99,000/year. That makes labor one of the biggest cash drains, so every extra shift has to be tied to covers, check size, and service quality.

For a limited-seat restaurant, labor cost percentage is a direct hit to owner income. If the owner covers shifts, cash strain can fall in the short run; if those hours shift to paid staff, distributions drop unless revenue rises enough to cover it. The quick math: more paid hours only work when table turns and average check support them.

Match Staff to Covers

Track labor as a percent of sales by daypart, not just month end. Compare scheduled hours to covers, check size, and reservations so slow days do not carry weekend staffing. Here’s the quick rule: if Monday volume is light, trim prep and floor labor early; if Friday and Saturday fill faster, add enough support to protect service speed and tips.

Track labor dollars per cover.

Schedule to reservation counts.

Log owner hours separately.

Test one labor-light weekday plan.

Protect service on high-cover nights.

What this estimate hides: bad scheduling can raise payroll without lifting revenue, and that cuts owner draw fast. Use a weekly labor plan that shows paid staff hours, owner-covered shifts, payroll taxes, and benefits together. If paid staffing rises, revenue must rise too, or the extra labor just replaces profit.