How Much Sound Healing Therapy Practice Owners Make: $59k EBITDA

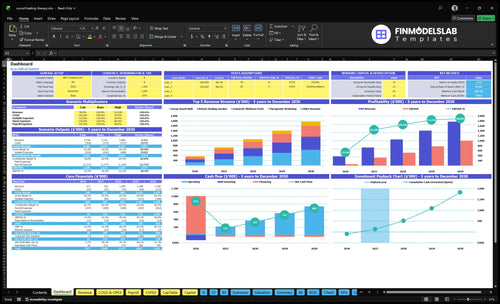

You’re modeling owner income before the studio is fully booked, so separate revenue, operating profit, reserves, and owner pay The base case shows $371k revenue and $59k EBITDA in the first year, reaching $1768M revenue and $1005M EBITDA by Year 5 This covers solo and small-studio economics, not tax advice or guaranteed wages

Owner income$214kNet margin16% to 57%Revenue for target pay$1.35MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full forecast and owner take-home?

For a Sound Healing Therapy Practice, the fastest income lift is better utilization: move from 15 visits/day to 30 visits/day before adding heavy staff or space. Then raise revenue quality with private sessions, corporate events, workshops, packages, and memberships. The Year 5 model reaches 45 visits/day, $1.768M revenue, and $1.005M EBITDA, but underused space, weak bookings, burnout, and contractor payouts can hurt margin.

Grow visits first

Lift daily visits from 15 to 30.

Delay heavy space commitments.

Delay heavy staffing commitments.

Fill more sessions before adding services.

Improve revenue mix

Sell more private sessions.

Book corporate wellness events.

Offer workshops, packages, and memberships.

Watch contractor payouts and burnout.

Can you make a living with a sound healing business?

Yes, a Sound Healing Therapy Practice can make a living if booked demand covers a high fixed-cost base; the Year 1 model needs 15 visits/day across 310 days to reach $371k revenue and $59k EBITDA. For setup decisions, How To Start A Sound Healing Therapy Practice? should focus first on visit volume, payroll, and cash left after fixed costs.

Living-Wage Math

4,650 Year 1 annual visits

$371k modeled annual revenue

$59k EBITDA before owner distributions

30–45 visits/day improves owner-pay odds

Cost Reality

$85k Studio Director payroll included

$65k Lead Sound Practitioner included

$1.056M–$1.768M revenue supports scale

EBITDA excludes taxes, debt, reserves

How much revenue can a sound healing practice make?

A Sound Healing Therapy Practice can make a lot more than a simple class ticket suggests, because revenue depends on service mix, not just attendance. Using the stated Year 1 mix, the weighted average is about $92.75 per booking, and retail can add $8 more per visit to about $100.75. By Year 5, the shift toward more private, corporate, and workshop sales lifts that to about $145.50 before retail, or $160.50 with the $15 retail add-on.

Year 1 revenue mix

65% group sessions at $45

20% private sessions at $150

5% corporate events at $500

10% workshops at $85

Year 5 revenue mix

45% group sessions at $45

25% private sessions at $150

15% corporate events at $500

15% workshops at $85

Want the six income drivers?

1

Utilization

15-45/day

More daily visits drive the biggest revenue jump, and moving from 15 to 45 visits a day is the main path to higher owner take-home.

2

Pricing

$45-$600

Higher ticket prices on private, corporate, and workshop sessions raise revenue per slot, so small price gains flow straight to profit.

3

Service Mix

45% group

As group sessions fall and higher-priced private and corporate work rises, average revenue per visit goes up.

4

Staffing Load

$214K

Year 1 payroll is $214K, so owner income improves only if session volume grows faster than labor cost.

5

Space Costs

$9.6K/mo

Studio lease and overhead are fixed, so fuller schedules spread those costs across more revenue and widen margin.

6

Repeat Sales

High

Repeat clients keep the calendar full and lower paid marketing needs, which helps protect take-home pay.

Sound Healing Therapy Practice Core Six Income Drivers

Pricing And Average Transaction Value

Pricing and ticket size

This driver is the average dollars collected per booking. Average transaction value (ATV) only lifts owner income when demand holds, because a higher price with weaker fill rate cuts total revenue and cash flow. One clean rule: price should rise only when repeat demand, room capacity, and facilitator value can absorb it.

Year 1 pricing is $45 per group attendee, $150 per private session, $500 per corporate event, and $85 per workshop. By Year 5, those rise to $55, $175, $600, and $110. That’s a 22% lift on group seats and a 20% lift on corporate events, so price gains only help if attendance and repeat bookings stay steady.

Raise price without losing fill

Track realized price per booking, repeat rate, and fill rate by offer type. If a $45 seat moves to $55, revenue improves only if you do not lose more than about 18% of attendees. Watch corporate close rate too, because that tier carries the biggest ticket and the biggest drop in income if deals slip.

Test increases by format: group baths, private sessions, workshops, and corporate events. If repeat demand softens after a price change, hold price and improve the experience first. Use retention as the guardrail, since weak repeat bookings turn a higher list price into lower total revenue and less owner draw.

1

Utilization And Booking Volume

Utilization And Booking Volume

Utilization is booked visits divided by available slots. In this model, volume moves from 15 visits/day in Year 1 to 45 visits/day in Year 5 across 310 operating days, or 4,650 to 13,950 visits a year. That is the main driver of owner income: more filled sessions spread fixed costs over more sales, so cash flow improves only when seats stay full.

Year 1 revenue starts at $371k, and the model hits break-even in Month 5. If fixed overhead is $96k/month, weak weekday bookings can drain cash fast, because empty Monday-to-Thursday slots still carry rent and payroll. That is why utilization matters more than raw capacity.

Track Visits By Day, Not Just Month

Track booked visits by day and time slot. Here’s the quick math: 15/day equals 4,650 annual visits; 22/day is 6,820; 30/day is 9,300; 38/day is 11,780; 45/day is 13,950. Use that pace to judge whether the schedule can cover fixed costs and still leave room for owner draw.

Measure weekday fill rate daily.

Watch no-shows and repeat bookings.

Test offers for Tue-Thu demand.

Cut open hours if slots stay empty.

Protect take-home pay by tying staffing and room hours to demand, not hopes. If Tuesday-to-Thursday fill stays soft, pull back capacity before fixed costs outrun bookings.

2

Service Mix

Service Mix Drives Revenue Per Booking

Service mix is the split between group sound baths, private sessions, corporate events, and workshops. A 65% group mix in Year 1 keeps the calendar full, but the 25% private, 15% corporate, and 15% workshop mix by Year 5 raises revenue per booking. Group work gives capacity; private and corporate work raise owner income faster.

Here’s the tradeoff: group sessions use less sales effort and can repeat well, while private and corporate bookings need more prep and venue control. Corporate revenue can be lumpy, so one weak month can hit cash flow even if the annual mix looks strong. If mix shifts toward higher-ticket work, the owner’s take-home can improve only if booking flow stays steady.

Measure Mix By Slot Type

Track bookings, revenue, and prep time by service line. Use the same view each month: group, private, corporate, and workshops. That shows whether higher-priced work is really lifting profit, or just adding sales time and schedule gaps.

Watch revenue per booking by type.

Track fill rate on group sessions.

Log prep hours for private and corporate.

Flag corporate sales cycles and delays.

A simple rule helps: if the mix adds revenue but also adds empty gaps, margin can fall. If corporate leads take longer to close, build a cash buffer before you rely on them for owner pay.

3

Memberships And Repeat Clients

Repeat Clients and Memberships

Packages, memberships, and recurring classes can smooth cash flow, but only if clients keep coming back. With 310 operating days, even a small drop in repeat bookings cuts annual visits, and that hits owner pay fast. If the studio drives 15 visits per day in Year 1, retail add-ons at $8 per visit add about $120 per day, or $37,200 a year.

What this driver includes is simple: repeat bookings, membership renewals, and add-on sales tied to group sound baths, workshops, and private session packages. The key inputs are visit frequency, retention rate, and add-on spend per visit. By Year 5, retail add-ons rise to $15 per visit, or about $225 per day, which is $69,750 a year before any extra labor or refund risk.

Track Redemptions, Not Just Sales

Measure renewal rate, unused credits, and repeat-booking share every month. Memberships that look good on paper can hurt cash if clients do not redeem them, since that creates refunds, churn, and weak trust. Build offers around attendance, not just prepayment, so the studio protects revenue across the full 310-day schedule.

Keep the offer tied to group sound baths, workshops, and private session packages so clients have a clear reason to return. If add-on spend stays near $8 to $15 per visit, that is a clean signal the model is working; if redemptions slip, the owner may have cash in hand now but less income later.

4

Space And Venue Costs

Space Costs Set the Floor

Space can protect margin or crush it. A $65k/month dedicated studio lease sits inside $96k/month of fixed overhead before payroll, so the room has to stay busy just to avoid turning rent into owner pay. If class fill is uneven, every empty seat still carries the same fixed cost.

Shared space or room rental lowers cash risk, but it also limits schedule control and peak booking capacity. The $75k acoustic buildout only makes sense if steady attendance can absorb the extra fixed load; otherwise, the owner is financing quiet hours and unused square footage.

Track Fill Before You Sign

Measure the inputs that decide whether space pays: weekly bookings, average attendees per class, private session demand, and monthly fixed overhead. Here’s the quick math: if bookings are inconsistent, fixed rent stays the same and owner income drops fast.

Track fill by day and session type.

Test shared space first.

Delay buildout until demand is steady.

Match lease length to bookings.

If weekday volume is thin, keep the footprint light. If attendance is reliable, a dedicated room can support scale, but only when the rent, buildout, and schedule control all line up with real cash flow.

5

Owner Time And Staffing

Owner Time and Staffing

Solo delivery keeps payroll low, but it caps how many sessions you can run. This staffing plan adds an $85k Studio Director, $65k Lead Sound Practitioner, $52k Associate Practitioner, and $38k Front Desk Coordinator. As the Associate Practitioner grows from 0.5 FTE to 2.5 FTE and Front Desk from 1.0 FTE to 2.0 FTE, fixed payroll rises fast, so owner pay depends on bookings staying ahead of labor.

Here’s the quick math: more staff can lift visit volume, but if payroll grows faster than revenue, owner distributions shrink even when sales rise. The key inputs are visits, schedule fill, revenue per session, and total payroll. If weekday demand is uneven, the studio may look busy on paper yet still miss the cash needed to pay the owner well.

Track staffing against bookings

Measure revenue per labor dollar, weekly booked sessions, and hours used by each role. Keep each hire tied to a clear load target, like class count, private sessions, or front-desk coverage, before adding FTE. That protects margin and keeps payroll from eating the extra cash the new staff is supposed to create.

Use a simple gate: hire only when booked volume is stable enough to cover the new payroll rate. Watch whether the $52k Associate Practitioner and $38k Front Desk Coordinator pay for themselves through more visits, not just better service. If bookings lag, hold staffing flat and keep the owner on the schedule.

6

Compare owner income under lean, base, and mature operating scenarios

Owner income scenarios

Owner income shifts fast in this model because it depends on visit volume, service mix, staffing, and fixed lease load. Higher utilization lifts EBITDA, but cash stays tight until payroll and reinvestment are covered.

Low, base, and high cases show how much owner income can move as the studio fills up.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Low-case ramp: 15 visits a day and Year 1 pricing support only $59k EBITDA, so owner income stays tight after payroll and lease costs.

Base-case growth: 30 visits a day and Year 3 pricing lift EBITDA to $522k, so owner take-home improves if staffing stays controlled.

High-case scale: 45 visits a day and Year 5 pricing drive $1.005M EBITDA, but owner income still depends on cash, debt, and reinvestment needs.

Typical setup

This is a lean opening year with $371k revenue, 65% group sessions, $214k payroll, $9.6k monthly fixed overhead, and Month 5 breakeven.

This is a steadier operating year with $1.056M revenue, a more balanced service mix, and enough throughput to support higher margin.

This is a mature studio with $1.768M revenue, stronger corporate and workshop mix, and more staff needed to hold service quality.

Cost drivers

Visit volume

group-heavy mix

payroll load

fixed lease overhead

booking and marketing fees

Visit volume

service mix shift

practitioner staffing

retail attach rate

fixed overhead spread

Visit volume

corporate events

workshop mix

staffing FTE

reinvestment needs

Owner income rangeBefore owner reserves

About $59k EBITDALow Case

About $522k EBITDABase Case

About $1.0M EBITDAHigh Case

Best fit

Use this to stress-test a slow ramp, weaker utilization, or higher staffing strain.

Use this as the modeled middle case for budgeting, hiring, and cash planning.

Use this to test upside from strong utilization and higher-value bookings.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.