How Much Does A Soybean Meal Production Owner Make On $2129M

A soybean meal production owner can make strong income only when the crush spread covers raw soybeans, plant costs, debt, and retained cash In the researched case, first-year sales are $2129M across 372,000 modeled units, with known product-level costs of about $215M plus 30% outbound logistics, or about $64M That leaves about $1851M before soybean purchases, fixed overhead, debt service, taxes if modeled, and reserves Treat that as planning contribution, not guaranteed soybean meal production owner take-home

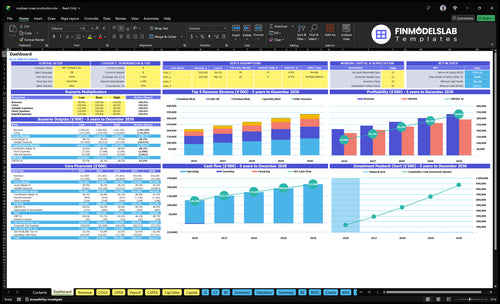

Owner income$180.4MNet margin84.8%Revenue for target pay$212.9MBusiness difficultyHard

Want to test your soybean meal owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, operating costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do I check owner income in the Soybean Meal Production model?

Open the Soybean Meal Production Financial Model Template to see revenue, gross contribution, operating costs, debt, reserves, and owner income. It also covers units, prices, costs, logistics, procurement, working capital, and reserve settings.

Owner-income model highlights

Owner income after obligations

Revenue and margin view

Scenario and cash charts

Can a small soybean meal plant support an owner?

Soybean Meal Production can support an owner, but only if utilization, contracts, maintenance uptime, and labor coverage stay strong. This case is not tiny: it models 372,000 first-year units and five revenue streams, so the business needs steady throughput, not passive ownership. A manager-run plant can cut owner time, but it also adds payroll pressure, so the owner still has to watch cash, controls, and inventory closely.

Owner support depends on volume

372,000 first-year units need uptime

5 revenue streams reduce single-customer risk

Contracts must keep the plant loaded

Low utilization hurts owner pay fast

What changes the workload

Manager-run ops lower daily owner labor

Payroll rises when you add managers

Scaled plants spread fixed costs better

More scale also needs more cash control

How do soybean prices affect soybean meal production profit?

Yes — soybean prices can squeeze Soybean Meal Production profit because they hit the crush margin, which is the spread between soybean input cost and the value of meal, oil, hulls, and other outputs. For startup context, see How Much Does It Cost To Open, Start, Launch Your Soybean Meal Production Business? because first-year revenue of $2,129M still has to cover raw soybean purchases before profit shows up. Standard meal at $450 and premium meal at $580 matter too, but even a small soybean cost increase can cut owner take-home fast.

Profit pressure

Higher soy cost shrinks crush margin.

Raw beans get paid first.

Meal price sets sales value.

Small cost jumps hit take-home.

Key price points

$450 standard meal price.

$580 premium meal price.

$2,129M first-year revenue.

Crush margin drives profit.

Is soybean meal production profitable?

Soybean Meal Production can be profitable, but only if the crush spread, meaning the gap between soybean input cost and meal/oil output value, covers processing, freight, fixed overhead, debt service, and cash reserves; see What Is The Most Critical Indicator To Measure Soybean Meal Production Success?. First-year revenue is $2,129M, with known direct product costs of $215M and outbound logistics of $64M, but that excludes raw soybean purchases, the largest cost driver.

Profit Drivers

Known costs total $279M

Known costs equal 13.1% of revenue

Raw soybeans are not included

Utilization drives margin recovery

Risk Checks

Lock quality sales contracts

Model soybean purchase exposure

Fund working capital needs

Protect plant reliability

Want the six soybean meal income drivers?

1

Throughput

372K

Year 1 volume is 372K units, so more line uptime spreads fixed plant costs and lifts cash after obligations.

2

Soy Cost

$215M

Known direct first-year costs are $215M, so every bean price cut widens owner take-home fast.

3

Selling Price

$2.13B-$3.35B

First-year revenue is $2.129B and mature-year revenue reaches $3.354B, so price discipline drives the biggest cash swing.

4

Byproduct Yield

112K

Hulls, oil, and specialty meal add 112K saleable units, so better recovery turns the same soy into more cash.

5

Variable Costs

4.5%

Outbound logistics starts at 3.0% and sales fees at 1.5%, so tight cost control protects take-home margin.

6

Cash Buffer

$3.63M

Debt service, working capital, and reserves lock up cash, and the model needs $3.634M minimum cash in the opening month.

Soybean Meal Production Core Six Income Drivers

Throughput And Plant Utilization

Throughput and Plant Utilization

Utilization is how much of the plant’s usable capacity turns into sold output. Here, modeled volume rises from 372,000 first-year units to 536,000 mature-year units, and revenue rises from $2129M to $3354M. That helps because fixed plant costs get spread over more units, but only if gross margin stays positive.

The owner’s take-home improves only after soybean cost, overhead, debt, and reserves are covered. The main risk is treating capacity as sales before contracts exist. Watch annual units sold, uptime, customer orders, and inventory turns so the plant does not look busy but still fail to generate cash.

Track Sold Units Before You Chase Capacity

Measure sold units, not just run rate. If uptime rises but orders do not, cash gets trapped in inventory and owner pay stays weak. Here’s the quick math: more output helps only when each extra unit still clears variable cost and supports fixed overhead.

Use a simple weekly scorecard:

Annual units sold vs plan

Uptime and downtime hours

Customer orders by contract

Inventory turns and days on hand

1

Soybean Procurement Cost

Soybean Procurement Cost

Soybean procurement cost is the biggest swing factor in soybean meal income. If the plant buys on the wrong basis, moisture, quality, or freight terms, the apparent contribution can disappear before processing starts, which cuts gross margin and the cash left for owner pay.

Think in gross margin, meaning sales left after direct input costs. Compare each soybean purchase against the value of meal, oil, hulls, and any specialty output; if landed soybean cost rises faster than that bundle, the owner’s take-home drops even when plant volume stays flat.

Track the landed soybean cost

Measure landed cost per ton, not just the bid. Build it from purchase price, freight terms, moisture discounts, shrink, and quality cuts, then compare it with realized output value from meal, oil, hulls, and specialty product. That tells you if the plant is buying margin or just buying throughput.

Track basis and freight separately.

Log moisture and protein discounts.

Test yield against output mix.

Review supplier terms before buying.

If landed cost moves up but output value does not, owner cash gets squeezed fast. The useful control is simple: keep a purchase ledger that ties each load to expected recovery, so you can see margin loss before it becomes a bad month.

2

Soybean Meal Selling Price

Soybean Meal Selling Price

Selling price drives revenue, but it does not set owner pay on its own. First-year pricing is $450 for standard meal, $580 for premium meal, and $680 for specialty meal; mature-year pricing rises to $490, $640, and $760. The real question is the net realized price after specs, freight, and contract terms.

Here’s the quick math: better pricing lifts revenue per ton, but weak delivery terms can turn volume into low cash. The key inputs are product mix, protein specs, customer mix, and contract quality. If soybean input costs and operating costs rise faster than selling price, the extra revenue won’t flow through to gross margin, cash flow, or owner distributions.

Track Net Realized Price

Measure cash collected per ton by grade, not just list price. Compare actual sales against $450, $580, and $680, then against the mature targets of $490, $640, and $760. Split out freight, discounts, rejects, and short-ships so you can see what the market is really paying.

To improve owner income, test whether tighter protein specs and stronger contracts raise realized price more than they add cost. If premium or specialty meal needs extra testing, handling, or delivery expense, include that in the margin check before you sign. Price growth only helps when it leaves more cash after input costs and operating costs.

3

Yield And Byproduct Credits

Yield And Byproduct Credits

Byproduct credits lift cash from the same soybean input. In year one, disclosed byproduct revenue includes $12M from soybean hulls and $665M from crude oil, and specialty meal adds $204M. That can raise margin per ton processed, but only if extraction rates, product quality, and handling losses stay tight.

What this hides is plant-to-plant variation. Oil recovery, hull handling, shrink, and off-spec output all move gross profit, so a plant with the same soybean feed can still pay the owner very different cash. The key inputs are processed volume, oil yield, hull capture, and quality loss.

Track Recovery, Shrink, and Credit Value

Measure byproduct revenue by plant and by line, not just total meal sales. If credits come from oil recovery and hull handling, then small yield changes can change owner pay more than a small price move in meal.

Track oil pounds per soybean ton.

Track hull capture and shrink.

Track off-spec and downgraded lots.

Compare credit value by plant.

Use those numbers to forecast gross profit per ton before you promise distributions. If quality slips or losses rise, the byproduct credit falls fast and cash for debt, reserves, and owner draws drops with it.

4

Operating Cost Control

Operating Cost Control

Operating cost control decides how much of each soybean meal sale turns into cash for the owner. First-year direct product costs are about $215M, and outbound logistics at 30% adds about $64M, so variable spend is roughly $279M before fixed overhead. If those costs drift, owner pay shrinks even when volume grows.

The mix matters. Standard meal carries $35 per-unit processing costs plus 30% revenue-linked costs, while specialty meal carries $60 per-unit costs plus 51% revenue-linked costs. At first-year prices of $450 and $680, a weak freight plan or poor yield can turn sales into thin cash fast.

Track Unit Cost

Track cost per unit by product, not just plant totals. Use units sold, product mix, freight miles, processing labor, yield loss, and downtime to split variable costs from fixed overhead. That split shows where scale helps and where it doesn’t. One line: control the unit cost, and you protect the draw.

Set monthly targets for processing cost, outbound freight, and shrink. Compare actuals to the model: standard meal should not drift above its $35 base without a clear reason, and specialty meal needs enough price premium to cover its 51% revenue-linked load. What this hides is debt and reserve needs, so the real goal is free cash after operating costs.

5

Debt Service And Cash Reserves

Debt Service And Cash Reserves

EBITDA is not owner income. A plant can look profitable and still keep cash for soybean inventory, repairs, lender requirements, compliance, and expansion debt service. Because debt service and working capital are not provided, distributable cash cannot be finalized. The $1,851M known contribution is only a ceiling signal, not take-home pay.

Here’s the quick rule: when inventory rises, maintenance hits, or financing needs grow, owner distributions should drop. More cash trapped in the business means less cash to draw. That’s the real pressure point for a soybean meal plant, especially before reserve targets and loan payments are locked in.

Track Cash Before You Pay Yourself

Model monthly cash after soybean buys, repairs, taxes, and debt payments. Track a minimum cash floor, inventory days, and any reserve covenants so you can see what is actually safe to distribute. If those items are not in the forecast, profit can look strong while owner pay stays tight.

Set a monthly reserve floor.

Model debt payments first.

Separate maintenance from growth.

Pay owners only from surplus cash.

6

Compare low, base, and high soybean meal owner income cases

Owner income scenarios

Owner take-home moves with plant use, soybean cost, meal pricing, freight, and debt service. The low, base, and high cases show how much cash can reach the owner after operating costs and missed obligations.

Low, base, and high cases for owner take-home.

Scenario

Low CaseDownside case

Base CasePlanning case

High CaseUpside case

Launch model

Runs below plan with weaker throughput and pricing, so owner take-home stays thin after freight, soybean, and debt costs.

Tracks the modeled first year, where 372,000 total units and $212.9M revenue leave room for owner take-home after operating costs and obligations.

Assumes stronger utilization, better price realization, and tight cost control, so more cash can reach the owner after obligations.

Typical setup

The plant runs below nameplate, meal prices soften, soybean inputs stay high, and logistics plus debt service absorb most of the margin.

Standard and premium meal carry most volume, by-products add value, and owner income depends on soybean cost, freight, fixed overhead, debt, taxes, and reserves.

The plant stays fuller, freight stays controlled, premium products sell well, and reserve discipline keeps more EBITDA available to the owner.

Cost drivers

Lower utilization

higher soybean cost

softer meal pricing

freight pressure

debt service

Volume mix

soybean cost

outbound logistics

fixed overhead

debt and taxes

Higher utilization

stronger pricing

controlled freight

lower waste

reserve discipline

Owner income rangeBefore owner reserves

Near-zero drawThin draw

Moderate drawModeled draw

Strong drawUpside draw

Best fit

Use this to stress test weak sales, cost spikes, and tight cash days.

Use this as the core planning case for budgeting and lender review.

Use this to test what happens when volume, pricing, and cost control all hold up.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.