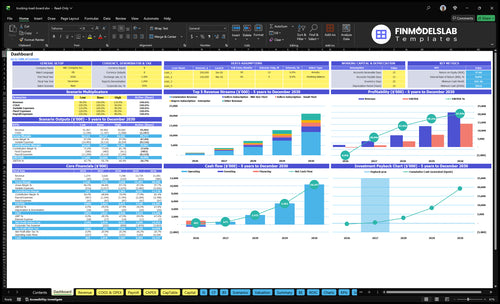

How Much Does A Trucking Load Board Owner Make? $812k Pre-Fixed Case

Using the researched assumptions, a trucking load board can show strong profit potential, but owner take-home is not the same as revenue The first-year case produces about $139 million in revenue, driven by subscriptions, an 80% transaction take rate, and optional promotion fees Gross margin is about 965% after transaction processing and cloud hosting costs, but marketing, sales commissions, support, payroll, reserves, and taxes reduce what the owner can actually take home The source data supports about $812k before fixed payroll, admin, reserves, and taxes final owner pay needs those missing assumptions entered separately

Owner incomeSet by ownerNet margin96.5%Revenue for target pay$996kBusiness difficultyHard

Want to see the six income drivers?

1

Carrier subs

500 carriers

Five hundred first-year carriers paying $29-$149 a month drive the core recurring revenue line.

2

Shipper supply

500 shippers

Five hundred first-year shippers keep the board full, which raises match volume and repeat use.

3

Pricing mix

80%

An 80% first-year take rate and $29-$149 carrier plus $49-$299 shipper pricing decide revenue per active account.

4

CAC efficiency

$350K

$350K of first-year acquisition spend only pays back if the $300 carrier CAC and $400 shipper CAC stay disciplined.

5

Churn control

Model input

Churn and reserves are model inputs here because no source values were provided, so retention risk is hard to price.

6

Cost structure

965%

Very low direct costs and the modeled 965% gross margin leave fixed payroll, support, and software as the main take-home drag.

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on demand, pricing, margins, payroll, taxes, debt, and reinvestment.

Want to stress-test owner income in the Trucking Load Board model?

What does the owner do in a trucking load board business?

The owner of a Trucking Load Board protects marketplace liquidity, so there’s enough real freight for carriers and enough reliable carriers for shippers. Early work is shipper sales, carrier onboarding, support, fraud checks, pricing tests, and keeping posted loads current. If one side grows faster than the other, paid carriers cancel when loads are thin, and shippers leave when coverage is weak. Founder-led ops can save cash early, but staffed scale has to be in the owner-pay math.

Keep freight moving

Sell shippers first

Onboard carriers fast

Keep loads current

Match routes closely

Protect cash and trust

Check fraud early

Test pricing often

Answer support quickly

Plan payroll for scale

Can you make money owning a trucking load board?

Yes, a Trucking Load Board can make money if paid carrier accounts, shipper demand, and load quality drive repeat use; see What Is The Current Growth Rate Of Your Trucking Load Board Platform? before scaling spend. In the first-year source case, 500 carriers and 500 shippers produce about $996k subscription revenue, $305k commission revenue, and roughly $139M total revenue if promotion fees run monthly.

Money Drivers

Sell paid carrier accounts

Build shipper density

Keep load quality high

Push repeat monthly usage

Owner Reality

Gross revenue is not take-home

Pay COGS and support first

Fund sales, ads, acquisition

Reserve for payroll, taxes

How many paid carriers does a load board need for owner pay?

For a Trucking Load Board, you can’t pin down one paid-carrier count from carrier subscriptions alone. Here’s the quick math: target owner pay ÷ operating margin = required revenue, then divide that by about $816 per carrier per year, based on a $68 weighted monthly price. That still leaves out shipper subscriptions, transaction fees, load volume, CAC, churn, and reserves, so the real threshold depends on fixed costs and your target reserve rate.

Carrier fee base

$29 owner-operator plan

$79 small-fleet plan

$149 mid-size plan

$68 weighted monthly average

What changes the count

Shipper subscriptions add revenue

Transaction fees add revenue

CAC and churn raise the bar

Reserves and fixed costs matter

Key Takeaways

500 carriers at $68 monthly drive predictable revenue.

500 shippers at $98 monthly add $588k annual revenue.

Churn can erase CAC gains if retention slips.

Take rates fall, so volume must keep rising.

Compare lean, base, and scale scenarios for owner income planning

Owner income scenarios

Owner income swings hard because paid carriers, shipper mix, take rate, acquisition spend, and fixed payroll all move together. The low, base, and high cases show how fast cash can tighten or expand.

Compare downside, modeled, and upside owner income cases.

Scenario

LowDownside case

BaseModeled case

HighUpside case

Launch model

This is the lower owner-income path, with slow paid account growth and tight cash.

This is the modeled owner-income path, using the first-year setup and planned scale-up.

This is the stronger owner-income path, with more acquired users and better unit economics.

Typical setup

The model has fewer carriers and shippers, lower load volume, higher CAC pressure, and tighter owner pay while fixed payroll and sales spend stay heavy.

The model starts with 500 carriers and 500 shippers, about $139M revenue, 965% gross margin, and about $812k before fixed payroll, admin, reserves, and taxes.

The model scales to 4,250 acquired carriers and about 3,667 acquired shippers by year five, with 60% take rate, 23% COGS, and $195M in combined acquisition budgets.

Cost drivers

slow paid account growth

lower load volume

higher CAC

fixed payroll burden

reserve needs

carrier and shipper count

take rate

variable sales and ad costs

COGS

fixed payroll

more acquired carriers

more acquired shippers

lower CAC

stronger repeat orders

higher take rate

Owner income rangeBefore owner reserves

-$289k - $0Cash risk

$812k - $1.1MModeled range

$7.5M - $14.3MUpside range

Best fit

Use this to test downside cash burn, CAC payback risk, and how much reserve you need.

Use this as the working plan for budgeting, hiring, and cash control.

Use this to test upside capacity, staffing pace, and how fast owner income can scale.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Trucking Load Board Core Six Income Drivers

Paid Carrier Subscriptions

Paid Carrier Subscriptions

Paid carrier accounts are the cleanest recurring revenue line in a load board. With 500 carriers at a weighted monthly price of about $68, first-year revenue is about $34,000 a month or $408,000 a year. That cash is predictable, but only while carriers stay active and see enough real loads to justify the fee.

Here’s the catch: if churn rises, revenue drops and CAC rises at the same time. With first-year carrier CAC at $300, replacing 100 canceled accounts can cost about $30,000 before support even comes in. One weak retention month can shave owner draw fast.

Keep Carrier Revenue Sticky

Track active carriers, weighted monthly price, churn, CAC, and support capacity. The mix matters because small fleets and mid-size fleets usually pay more, but they also expect better tools and faster help. If support lags, cancellations rise and subscription cash turns into replacement spend.

Watch active carriers monthly.

Price for fleet size mix.

Cut churn before scaling ads.

Staff support before growth spikes.

Small revenue lifts matter only if retention holds. If the carrier base stays live, subscription cash can cover more overhead and leave more room for owner pay; if not, growth just funds acquisition.

Churn And Carrier Retention

Carrier Retention

Churn, or cancelled carrier accounts, is the leak here. With 500 carriers at about $68 per month, carrier subscription revenue is roughly $34,000 monthly or $408,000 yearly. If carriers leave faster than they can be replaced, owner take-home drops because the platform must keep spending on acquisition to hold the same revenue base.

The source model gives $300 carrier CAC, but not churn, so churn has to be an editable assumption. Retention gets better when posted loads are real, search results are useful, support is fast, pricing feels fair, and fraud controls work. If those break, gross margin can still look fine while cash flow and profit to the owner weaken.

Cut churn before you buy more growth

Track monthly churn, active carriers, repeat logins, booked-load conversion, and support response time. Here’s the quick math: if one lost carrier costs about $300 to replace, even modest churn can eat the income from new signups. Keep the focus on keeping current carriers active, not just adding more accounts.

Measure cancel rate by cohort.

Audit load quality daily.

Flag fraud and duplicate posts.

Review support speed weekly.

Use churn as a forecast input, not a surprise. If cancellations rise, reduce spend on broad acquisition and fix the carrier experience first. That protects monthly recurring revenue and keeps owner pay from getting squeezed by replacement marketing spend.

Monetization Mix

Monetization Mix

For a load board, volume only turns into income when it converts into subscriptions, transaction fees, promotion fees, posting fees, ads, broker tools, and partner income. Recurring fees support cash flow, while variable fees move with bookings, so the mix decides how much the owner can pay themselves.

Here’s the quick math: the source case assumes $0 fixed commission, a variable commission starting at 80% in year one, and $15 seller promotion fees. By year five, the take rate falls to 60%, so the same load count earns less unless volume rises. Payment-flow revenue may need compliance, payment controls, and partner agreements.

Measure the mix, not just loads

Track each stream separately: active shippers, active carriers, load postings, bookings, average fee per load, and promotion use. If one stream carries most profit, protect it with pricing and retention work. A board with more loads but weaker monetization still leaves less owner income.

Watch take rate by year

Separate payment revenue

Stress-test booking volume

Test whether $15 promotion fees speed bookings enough to justify the charge. If they do not, they can hurt churn and lift support costs. The win is a mix that raises cash receipts without pushing fraud, compliance, or service work faster than revenue.

Shipper And Load Supply

Shipper Load Supply

Posted loads are the supply signal carriers pay for. In the first-year case, 500 shippers at a weighted $98 per month create about $588k of annual shipper subscription revenue. But the real ceiling is matching: implied shipper-side GMV is about $490M, while carrier-side constrained GMV is about $382M, so commission revenue stops where capacity runs out.

That means more loads help income only if they are monetized. Without subscriptions, posting fees, take rate, or promotion fees, extra volume mostly improves liquidity and retention, not owner pay. If posted loads grow faster than carrier supply, conversion falls and cash flow gets weaker even when top-line activity looks strong.

Measure Match, Not Just Posts

Track active shippers, posted loads, booked loads, and the gap between shipper demand and carrier capacity. Here’s the quick math: revenue depends on loads posted × booking rate × monetization per load, not on posted volume alone. If the carrier side stays below $382M of capacity, the board needs either more carriers or higher fees per load.

Active shippers

Loads posted per shipper

Booked-load rate

Revenue per load

Price the supply, not just the signup. Watch subscription ARPU, posting fee yield, and promotion fee attach rate. If a shipper posts lots of freight but pays only the base plan, the board may look busy while owner cash stays flat. Busy is not paid; matched and monetized is.

Operating Cost Structure

Operating Cost Structure

On a trucking load board, COGS and growth spend decide how much gross revenue reaches the owner. In the source case, COGS start at 35% of revenue and ease to 23% by year five, while variable sales and digital ad costs drop from 130% to 70%. If those costs outrun revenue, owner pay stays at zero even with strong bookings.

As the platform adds staff, cash use rises for support payroll, software development, data integrations, fraud prevention, compliance, and admin. The rule is simple: build reserves first, then pay the owner. If onboarding or support load spikes, fixed costs can eat margin fast.

Control the cost ratios first

Track revenue, COGS %, sales and ad spend as a percent of revenue, and each support role’s cost per active account. Compare actuals to the model’s 35% to 23% COGS path and 130% to 70% variable sales and digital ad path.

Hold owner draws until reserves fund.

Test founder-led support before hiring.

Measure cost per booked load monthly.

If costs do not fall as scale grows, higher volume just creates more cash pressure, not more take-home income.

Customer Acquisition Efficiency

Customer Acquisition Efficiency

This driver is the cost to win each active carrier and shipper account, and it decides whether growth turns into profit or just cash burn. In year one, $300 carrier CAC and $400 shipper CAC with $150k carrier marketing and $200k shipper marketing buy 500 accounts on each side. If those accounts churn fast, the owner keeps paying to refill the funnel instead of taking home cash.

By year five, CAC improves to $200 for carriers and $300 for shippers, but combined acquisition budgets rise to $195M. That can look like strong growth and still leave thin owner income if paid acquisition is eating the margin. Judge profit after growth spend is separated from stable operating costs, or owner pay will be overstated.

Track CAC by side, not blended spend

Track CAC separately for carriers and shippers, and use only activated accounts in the math. If $150k gets 500 carriers, carrier CAC is $300; if $200k gets 500 shippers, shipper CAC is $400. One clean rule: never count leads as revenue base.

Test spend by channel, then tie it to retention and booked loads. If the carrier side keeps active users longer, CAC can fall toward $200; if not, paid growth just replaces churn. Keep growth budgets on a separate line from fixed overhead so you can see the cash left for reserves and owner draw.