Owner income$16.1k/mo

Owner income$16.1k/moHow Much VHS to Digital Conversion Owners Can Make: $161k/Month

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$16.1k/mo  Net margin61%

Net margin61% Revenue for target pay$317.5k

Revenue for target pay$317.5k Business difficultyHard

Business difficultyHard

Key Takeaways

- Volume drives leverage after $6,050 fixed overhead.

- Break-even is about 262 service units monthly.

- Direct costs already exceed first-year revenue.

- Higher prices help only if margin stays intact.

Owner income$16.1k/moNet margin61%Revenue for target pay$317.5kBusiness difficultyHardWant to test your VHS conversion owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Need the VHS conversion forecast in a spreadsheet?

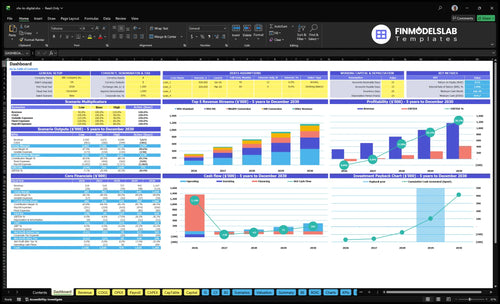

Yes—this VHS to Digital Conversion Service Financial Model Template shows the dashboard, income outputs, assumptions, revenue tabs, cost tabs, scenario testing, and owner-income outputs. It lets you test pricing, tape volume, service mix, labor, marketing, shipping, equipment reserves, and fixed overhead; known fixed overhead is $6,050/month before the missing software line.

Owner-income model highlights

- Revenue rises $317,500 to $1,167,080

- Gross margin near 893% to 898%

- Owner pay $193,410 to $936,518

What is the profit margin for VHS to digital conversion?

The VHS to Digital Conversion Service can look very strong on paper: the model shows $317,500 of revenue against $34,028 of direct COGS, so direct gross margin is about 89.3%. But once you add 55% of revenue for ads, outbound shipping, and payment processing, the leftover margin gets tight, so if you want the KPI view, see What Are The 5 KPIs For VHS To Digital Conversion Service Business?. The main leak is labor: technician hours are not supplied, so you should add them before treating margin as owner pay.

Direct margin

- $317,500 revenue in year one

- $34,028 direct COGS

- Direct COGS is about 10.7% of sales

- Direct gross margin is about 89.3%

Margin leaks

- 55% of revenue goes to variable costs

- Ads, shipping, and payment fees drive that

- USB drives and packaging add more leakage

- Add technician hours before owner pay

How many VHS tapes do I need to convert to make money?

If you’re running a VHS to Digital Conversion Service, the short answer is this: you need about 3,139 service units a year to break even, and about 7,464 service units a year to build $100,000 of pre-tax owner-pay capacity before reserves. The math is driven by $2,761 average revenue per service unit and about $2,313 of contribution after direct costs, ads, outbound shipping, and payment fees.

Break-even math

- $2,761 average revenue per unit

- $2,313 contribution per unit

- $72,600 fixed overhead per year

- 3,139 units yearly, or 262 monthly

Owner-pay target

- $100,000 pre-tax owner-pay capacity

- 7,464 service units yearly

- 622 orders monthly

- Five-tape orders need fewer customers

Can a VHS to digital conversion business be profitable from home?

A VHS to Digital Conversion Service can be profitable from home if you keep fixed costs, trust, and workflow tight. The supplied model includes $4,500/month in facility rent, so a home-based version should replace that cost instead of assuming it away. Local pickup lowers shipping friction and builds trust; mail-in can expand demand, but it adds packaging, tracking, return shipping, and loss-risk controls.

Home cost test

- Replace $4,500 rent line.

- Track capture station utilization.

- Control rework and spoilage.

- Price for owner time.

Demand and trust

- Use local pickup for trust.

- Use mail-in for wider demand.

- Add tracking and loss controls.

- Storefront raises credibility, not margin.

What moves owner take-home most?

1

11.5KOrder Volume

More tapes processed is the main revenue lever, since 11,500 first-year units set the base for owner pay.

2

$27.6Avg Ticket

A better mix of VHS HD, MiniDV, and repair lifts the average revenue per unit without the same fixed cost.

3

$23.1Labor Efficiency

Faster transfers and fewer reworks protect about $23.13 of contribution per service unit before overhead.

4

16.2%Fulfillment Cost

Tape handling, media, shipping, and payment costs decide how much of each job turns into EBITDA.

5

2.5%-1.5%Acquisition Cost

Keeping ad spend in range matters because paid demand eats margin before labor and overhead do.

6

$6.1K/moFixed Overhead

The monthly rent, utilities, and software load must be covered before any pre-tax owner draw starts.

VHS to Digital Conversion Service Core Six Income Drivers

Monthly Order Volume

Monthly Order Volume

Volume is the main leverage point here. First-year output is 11,500 service units, or about 958 per month, and the disclosed break-even is about 262 service units per month before the missing software line. Once $6,050/month of fixed overhead is covered, extra units should move fast to owner pay.

The catch is capacity. Capture stations, labeling, quality checks, and delivery have to keep pace, or rushed volume raises rework, customer support, and lost-tape risk. One bad batch can wipe out the profit from several clean orders, so the owner has to watch throughput and quality together.

Track Volume by Station

Measure orders per month, units per day, and rework rate side by side. The useful test is simple: can the team hold 958 monthly units without slipping on scan quality, labeling, or return timing?

Set a hard control on intake above the 262-unit break-even line, then scale in step with station output. If turnaround slips, freeze new volume before support costs and remake work eat the margin.

- Track units per station daily.

- Log rework and lost-tape incidents.

- Watch customer tickets per 100 orders.

1

Average Order Value

Higher-Ticket Orders

AOV (average order value) is the average revenue per order: revenue ÷ orders. Here, it rises when customers choose $35 VHS HD instead of $25 standard VHS, or buy Hi8 at $28, MiniDV at $30, or tape repair at $15. That mix sets the weighted average ticket and helps owner pay, but premium USB drives, packaging, software, and processing also lift direct cost, so margin matters as much as ticket size.

Raise AOV Without Losing Margin

Track AOV by tape type, add-on rate, and gross margin per package. If HD lifts revenue but costs climb faster, the owner keeps less cash. Use minimum orders and bundled upgrades to raise revenue per shipment, and test pricing so each package covers handling, media, and rework risk. A 40% price step from $25 to $35 is useful only when the extra dollars stay in profit.

- Measure revenue per order weekly.

- Test bundles, not just higher tickets.

- Protect margin on every upgrade.

2

Transfer Labor Efficiency

Transfer Labor Efficiency

Labor is the swing factor here because the model does not give a separate technician payroll or owner hourly rate. At 958 tapes/month first-year volume, small changes in minutes per tape, capture station utilization, or rework rate quickly change paid hours and owner take-home. One extra paid hour is one less hour of margin.

Automation helps with batching and file handling, but it does not remove handling, inspection, customer communication, or redo work. So the real risk is not just speed; it is quality. If tape errors rise, you lose margin twice: once in labor, and again in referrals and repeat orders.

Track labor by step

Track labor by step: intake, capture, labeling, QC, upload or USB prep, and rework. Measure minutes per tape and station hours per day so you can see where the queue slows. If one step keeps stretching, that is the bottleneck that cuts owner pay.

Use simple controls: batch similar tape types, set QC checklists, and cap redo work. Aim to quote on the labor-heavy mix, not just the easy jobs. If rework keeps climbing, raise price, tighten process, or add help before volume scales into lower margin.

- Minutes per tape by step

- Rework rate per batch

- Station utilization per day

- Turnaround days from intake to delivery

3

Customer Acquisition Cost

Customer Acquisition Cost

When paid ads eat a big slice of revenue, more orders do not always mean more pay. Here, first-year digital marketing runs at 25% of revenue, or about $7,938, so the business only keeps enough margin if conversion and fulfillment stay tight.

The mature-year case drops marketing to 15%, which is the real target. Local search, reviews, referrals, estate organizers, senior communities, and family archive partnerships can shift demand away from paid ads, while mail-in campaigns may add reach but also raise shipping and support costs.

Measure CAC by channel

Track customer acquisition cost (CAC) as ad spend plus sales support divided by new customers, then compare it to gross margin per order. If one channel costs more than the first-order profit, it is buying growth that the owner cannot pay out of.

Watch cost per booked order.

Track conversion rate by channel.

Test referral and partner leads first.

Count shipping and support on mail-ins.

Use the 25% to 15% spend drop as a planning benchmark, not a promise. If paid CAC stays high, revenue growth can still crush cash flow because each new customer arrives with a marketing bill attached.

4

Direct Fulfillment Cost

Direct Fulfillment Cost

Direct fulfillment cost covers digital media, USB drives, packaging, cleaning supplies, freight supplies, electricity, adapters, capture consumables, repair parts, and tool wear. At $34,028 in year one, this is 107% of revenue, so every $1 of sales is matched by $1.07 of direct cost before overhead. That means gross margin is negative, and owner pay only improves if waste, damage, and rework come down.

Here’s the quick math: standard VHS runs at $158 + 40% of revenue, VHS HD at $215 + 45%, and tape repair at $295 + 43%. The mix drives profit more than volume alone. What this estimate hides is redo work, damaged tapes, and replacement media; those leaks quietly cut contribution, the cash left after direct costs.

Track Cost Per Tape

Track direct cost by service type, rework rate, and replacement media count. Start with units, price, and mix, then add consumables, freight supplies, and tool wear so you can see which jobs make money and which do not. If the HD or repair mix rises, watch cost per unit closely, because those lines carry the heaviest load.

- Measure cost by tape type.

- Log redo and damage rates.

- Price repair work separately.

- Cut waste in packaging and media.

Set a monthly limit on scrap, damaged tapes, and replacement runs. These are cash costs paid before the owner sees profit, so even small leaks hit take-home fast. If direct cost stays above sales, more volume only scales the loss.

5

Fixed Overhead And Equipment Use

Fixed Overhead and Utilization

Fixed overhead is already $6,050/month from rent, utilities, security monitoring, and high-speed internet. Software subscriptions are listed but not priced, so keep that line editable; every added dollar raises the monthly hurdle before owner pay.

At about 958 tapes per month, that fixed load is roughly $6.32 per tape before software or equipment reserve. If stations sit idle, overhead per tape climbs fast; if utilization stays high, more of each job can flow to operating profit and then owner draw.

Track Utilization Before You Raise Pay

Build the model as $6,050 plus software plus an equipment reserve, and keep that reserve below operating profit before owner pay. Track tapes per station hour, downtime, rework, and turnaround time; those inputs tell you if the business can safely support a bigger draw.

Use one simple rule: more volume helps only if quality holds. If deck wear, cleaning, or replacements start rising, fund those costs first. Good utilization only lifts take-home income when the extra output does not create more redo work or customer support.

- Track tapes per station hour.

- Set software as an editable line.

- Reserve cash for deck replacement.

- Watch downtime and rework weekly.

6

Compare lean, base, and high VHS conversion income cases

Owner income scenarios

Owner income rises as volume scales and variable load falls, but fixed overhead still limits how much cash reaches the owner.

| Scenario | Low CaseReserve need | Base CaseBest fit | High CaseCapacity risk |

|---|---|---|---|

| Launch model | This is the lean case with lower output and tighter owner pay capacity. | This is the modeled core case with mid-range owner pay and steadier throughput. | This is the stronger earnings path, but it needs much higher throughput and tighter control. |

| Typical setup | The business runs at first-year scale with 11,500 service units, $317,500 revenue, a 55% variable expense load, and $72,600 of fixed overhead before owner pay. | The business reaches 25,300 service units, $726,630 revenue, a 44% variable load, and $545,971 of pre-tax owner-pay capacity. | The business reaches 39,100 service units, $1,167,080 revenue, a 33% variable load, and $936,518 of pre-tax owner-pay capacity. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $193,410Lean load | $545,971Core load | $936,518Heavy load |

| Best fit | Use this to stress-test a small launch, home-based setup, or any plan with slow early volume. | This is the main planning case for a staffed shop that is growing into stable demand. | Use this to test upside, but only if staffing, equipment, and turnaround times can handle the volume. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. If you run home-based, swap the $4,500 monthly rent for your actual overhead before using them.

Related Products

- VHS to Digital Conversion Service Porter's Five Forces Analysis

- VHS to Digital Conversion Service BCG Matrix

- VHS to Digital Conversion Service Business Model Canvas

- What Are The 5 KPIs For VHS To Digital Conversion Service Business?

- VHS to Digital Conversion Business Plan Template in Pre-Written Word

- How Increase Profitability Of VHS To Digital Conversion Service?

- What Are Operating Costs For VHS To Digital Conversion Service?

- How Much It Costs To Start A VHS To Digital Service: $46K+ CAPEX

- VHS to Digital Conversion Service Financial Model Template in Excel

- How To Open A VHS To Digital Conversion Service In 4 To 8 Weeks

- How To Write A Business Plan For VHS To Digital Conversion Service?

- VHS to Digital Conversion Service Marketing Mix

- VHS to Digital Conversion Service Marketing Plan

- VHS to Digital Conversion Service Business Proposal

- VHS to Digital Conversion Service PESTEL Analysis

- VHS to Digital Conversion Service Pitch Deck Example Editable PPTX

- VHS to Digital Conversion Service Business SWOT Analysis

- VHS to Digital Conversion Service Value Proposition Canvas

Frequently Asked Questions

Under the researched first-year assumptions, it can produce $317,500 in revenue from 11,500 service units After direct costs, variable ads, shipping, payment fees, and known fixed overhead, pre-tax owner-pay capacity is about $193,410 That is not guaranteed take-home because labor, taxes, debt, software amount, and reserves still matter