How Much Virtual Assistant Service Owners Make With $150K Founder Pay

You’re modeling owner pay before the agency can fully fund itself, so separate salary from profit This US virtual assistant service model includes remote administrative, technical, and creative support, with $150,000 annual founder salary, breakeven in Month 14, and EBITDA moving from -$236,000 in Year 1 to $547,000 in Year 2 It excludes personal taxes, debt payments, and guaranteed distributions

Owner income$12.5kNet margin-42% to 31%Revenue for target pay$46.8kBusiness difficultyHard

Which drivers move virtual assistant owner income most?

1

Pricing Power

$400-$870

Basic Admin starts at $400, Pro Creative at $650, and Elite Tech at $750, so every mix shift lifts owner income fast.

2

Client Growth

$50K-$400K

Marketing budget rises from $50K to $400K while CAC eases from $300 to $250, so more active clients only helps if churn stays low.

3

Billable Hours

20-30 hrs

Average billable hours per active customer rise from 20 to 30 a month, which is the cleanest way to grow revenue without adding as many clients.

4

VA Labor

18%-14%

Virtual Assistant compensation falls from 18% to 14% of revenue, so tighter delivery labor turns into higher margin and more owner pay.

5

Premium Mix

20%-40%

Selling more multi-service premium work, from 20% to 40%, and more add-ons, from 10% to 20%, raises revenue per client.

6

Overhead Control

$52.8K

Fixed overhead is about $52.8K a year, the model needs $599K minimum cash, and owner take-home is salary plus profit left after reserves.

What owner pay can your virtual assistant service support?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target owner pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, staffing, taxes, reserves, and execution.

Can you check owner income in the Virtual Assistant Service forecast?

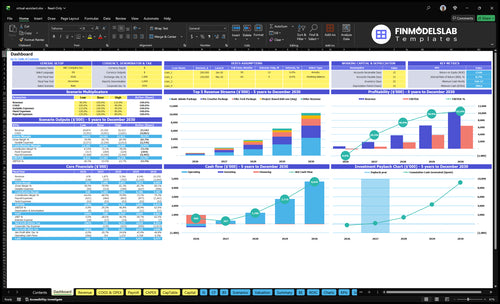

This dashboard in the Virtual Assistant Service Financial Model Template shows revenue, gross margin, EBITDA, cash need, breakeven, payback, and owner income. Charts run from -$236,000 EBITDA in Year 1 to $6.472 million in Year 5, with $599,000 minimum cash need, Month 14 breakeven, and $150,000 founder pay; assumptions tabs cover packages, client mix, billable hours, CAC, marketing, VA labor, payroll, fixed expenses, and startup costs.

Owner-income model highlights

Founder pay: $150k

Gross margin improves

Cash need: $599k

Low, base, high cases

What limits virtual assistant service owner income?

Virtual Assistant Service owner income is limited less by demand and more by founder time, client churn, quality control, delegation, pricing discipline, and client concentration. Here’s the hard math: founder pay is modeled at $150,000 a year, but Year 1 EBITDA is -$236,000, so early pay depends on cash planning, with a $599,000 minimum cash need, breakeven in Month 14, and payback in 24 months. This is not passive income, because client management and quality control stay active work.

What caps income

Founder time stays a bottleneck

Client churn cuts recurring revenue

Quality control needs constant oversight

Client concentration raises risk fast

What makes scale work

Train enough virtual assistants

Build account management capacity

Keep recruiting running every month

Use clear, priced service packages

What profit margin does a virtual assistant service make?

If you're sizing a Virtual Assistant Service, the short answer is that the model can show strong gross and contribution margins, but EBITDA is negative in Year 1 and turns positive at $547,000 in Year 2; see How Much Does It Cost To Open And Launch Your Virtual Assistant Service Business? for the startup-cost side of the math. Gross margin after VA delivery labor, training, quality assurance, and direct tools is 785% in Year 1, 799% in Year 2, and 841% in Year 5, while contribution margin after payment fees, onboarding, and sales commissions is 720% in Year 1 and 792% in Year 5. What this hides: revisions, hiring misses, and client churn can push the real margin lower.

Margin math

785% gross margin in Year 1

799% gross margin in Year 2

841% gross margin in Year 5

720% contribution margin in Year 1

Profit pressure

792% contribution margin in Year 5

EBITDA stays negative in Year 1

EBITDA turns positive at $547,000

Revisions and churn can cut real margin

Can a virtual assistant business owner make more by hiring subcontractors?

Yes, a Virtual Assistant Service owner can make more with subcontractors, but only if the billing spread pays for management time, recruiting, quality checks, and client success; track that spread with What Is The Most Critical Measure Of Success For Your Virtual Assistant Service?. Solo work can keep more margin per hour, but subcontractors raise total capacity and move the owner toward account management.

When it works

Bill above subcontractor cost

Cover quality review time

Keep client scope tight

Protect recurring subscription revenue

Model watchouts

VA compensation: 180% of Year 1 revenue

Falls to 140% by Year 5

Gross margin listed: 785% to 841%

Verify pricing before scaling labor

Key Takeaways

Clear packages raise revenue without adding full owner hours.

Retention matters; losing big clients can crush profit.

Billable hours must stay high, or labor hides cost.

Year-one EBITDA is negative $236,000, so reserves matter.

Scenario objective: Compare lean, base, and mature virtual assistant service owner-income outcomes using the model assumptions

Owner income scenarios

Owner income shifts as client count, package mix, and staffing scale change margin. The low, base, and high cases show what launch ramp, post-breakeven operation, and mature scale can look like.

A quick read on how owner pay changes as the service grows.

Scenario

Low CaseHigh cash risk

Base CaseReserve-dependent

High CaseHigh execution risk

Launch model

Year 1 is a lean ramp, so owner income stays close to founder salary while EBITDA is still negative.

Year 2 reaches post-breakeven, so owner income can start including profit distributions after salary.

Year 5 is the scale case, with stronger client density and higher owner income potential.

Typical setup

About $46,800 monthly revenue, about 69 active clients, and a 78.5% gross margin leave the business cash tight even with a $150,000 founder salary.

About $147,300 monthly revenue, about 188 active clients, and a 79.9% gross margin support positive EBITDA of $547,000 after the founder salary.

About $830,700 monthly revenue, about 725 active clients, and an 84.1% gross margin push EBITDA to about $6.472 million.

Cost drivers

Client ramp

founder salary

onboarding load

support costs

cash burn

Client growth

mix shift

lower CAC

fixed overhead

founder pay

Client density

add-on uptake

pricing lift

lower unit CAC

scale staffing

Owner income rangeBefore owner reserves

$150,000 salaryCash risk

Salary + distributionsPost-breakeven

Salary + scaled distributionsScale upside

Best fit

Use this to stress-test launch-month cash needs and a slow sales ramp.

Use this as the core operating case for planning reserves and owner draw policy.

Use this to test upside if sales, hiring, and delivery all work together.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Virtual Assistant Service Core Six Income Drivers

Pricing And Package Value

Pricing and Package Value

If your packages are too cheap, you sell busywork instead of margin. Here, the stated Year 1 prices start at $400 for Basic Admin, $650 for Pro Creative, and $750 for Elite Tech, with expected monthly customer value listed at $67750 after mix, uplift, and add-ons. Bigger retainers raise revenue per client, so you need fewer accounts to support owner pay.

The risk is scope creep. Underpriced packages create revision work, over-servicing, and margin leakage, which pushes up labor cost and hurts cash flow. By Year 5, expected customer value is listed at $1,14550, so pricing gains matter if scope stays tight and clients pay for the right service tier.

Price by scope, not by hours

Measure revenue per client, revision time, and add-on attach rate. Those three inputs tell you if the package is healthy or just keeping the team busy. If a lower tier keeps needing extra work, move tasks into a higher package or charge for add-ons.

Track scope changes each month.

Limit revisions in writing.

Price add-ons separately.

Review gross margin by package.

One clean rule: if the package does not cover the work, it is too cheap. Better packaging lifts monthly revenue per client and reduces client-count pressure, which helps protect owner take-home without forcing the founder to add the same amount of extra work.

Service Specialization

Service Specialization

Service specialization changes income by changing what each retainer can charge and how much hidden work it creates. As the mix shifts from 700% Basic Admin in Year 1 to 500% by Year 5, while Pro Creative rises from 300% to 500% and Elite Tech from 150% to 350%, average revenue per active customer can rise if the buyer sees clear value. That only works when price matches skill, scope, speed, and client expectations.

The risk is broad task lists. They blur scope, create unpaid revisions, and push the founder into low-value cleanup work, which cuts gross margin and owner pay. One clean rule: sell a defined outcome, not an open-ended to-do list.

Price the Scope

Track each service line by retainer, revision time, and hours per account. If a niche needs more speed, more QA, or deeper skill, the price has to move too. Specialization only helps when extra revenue is bigger than the added delivery cost.

Measure revenue per active customer.

Count unpaid revision hours.

Review scope creep weekly.

Raise price when skill jumps.

Use the mix to protect margin: keep Basic Admin simple, charge more for Pro Creative, and price Elite Tech for higher expectations. If one service drives the most rework, narrow the offer or reprice it before it drags cash flow and the owner’s draw.

Overhead, Systems, And Reserves

Overhead, Systems, And Reserves

Fixed overhead is the monthly support cost that keeps delivery running: founder salary, ops, sales, technical, recruiting, and accounting. Here it’s $4,400 per month, or $52,800 per year, plus a $150,000 founder salary. If those costs grow faster than gross profit, owner take-home gets crowded out.

The hard part is cash. Year 1 EBITDA (earnings before interest, taxes, depreciation, and amortization) is -$236,000, so reserves are not optional. The model’s $599,000 minimum cash need gives room for setup, payroll, and a slow sales ramp; without that buffer, growth can force pay cuts or delayed hires.

Track overhead before it eats owner pay

Watch fixed cost as a share of monthly gross profit, and separate core support from nice-to-have tools. Keep payroll roles tied to load: operations, sales, technical, recruiting, and accounting. If service quality slips, overhead was cut too far; if owner pay is the first line to get squeezed, the plan is underfunded.

Build a cash forecast that covers $40,000 platform development, $20,000 website and branding, and the ongoing burn, then test it against a slow sales month. One clean rule: if reserves cannot cover the ramp, don’t hire for capacity yet.

Billable Utilization And Capacity

Billable Utilization

Billable utilization is the share of VA time that clients can actually pay for. In this model, average billable hours per active customer rise from 20 per month in Year 1 to 30 per month in Year 5, a 50% increase. That lifts revenue density without needing the same jump in client count, but only if quality stays steady and rework stays low.

If the founder fills gaps with unpaid work, the numbers look better than the business really is. That hides true labor cost and can overstate profit, which makes owner pay hard to trust. More billable hours help cash flow, but only when delivery, onboarding, and account management are staffed well enough to avoid burnout and service slips.

Track Billable Hours Hard

Measure billable hours by client, VA, and service type. Split owner time between paid delivery, sales, onboarding, recruiting, and account management so nonbillable work does not disappear into the margin. The key test is whether the team can hold the move from 20 to 30 billable hours per customer per month without quality falling.

Track billable and nonbillable time.

Track rework, refunds, and churn.

Set capacity before selling more.

Protect owner time from free work.

Use those inputs to see whether revenue is coming from real capacity or just owner overtime. If higher utilization raises revisions, the extra revenue is fake. Predictable take-home income comes from hours that are billed, collected, and delivered without creating hidden labor cost.

Client Volume And Retention

Client Volume And Retention

Stable monthly clients make owner income easier to plan because less time goes into replacement sales. In this model, marketing budget rises from $50,000 in Year 1 to $100,000 in Year 2, CAC improves from $300 to $280, and average active clients rise from about 69 to 188. That supports steadier cash flow, but only if retained accounts stay active long enough to cover onboarding and service costs.

The key risk is concentration: losing a few large clients can erase profit fast. Churn means the share of clients who cancel in a period, and it is not provided here, so the model should keep an editable churn field. Here’s the quick math: better retention lowers replacement sales pressure and helps protect owner pay, while weak retention pushes spend back into marketing just to stand still.

Track churn and active accounts

Measure active clients, monthly churn, average client value, and CAC together. If active accounts are rising but churn is high, the business is buying growth instead of earning it. Watch which package tiers cancel first, because a few lost high-value clients can hit profit faster than many small ones.

Use a simple forecast with one editable churn input, then test retention actions that protect monthly recurring revenue: tighter onboarding, faster response times, and account reviews for larger clients. The goal is simple: keep more clients long enough to spread sales and setup cost across more months of revenue.

Track churn by package tier

Review active clients monthly

Flag top accounts early

Test onboarding and follow-up

Delivery Labor Mix

Delivery Labor Mix

This driver is the gap between client billing and delivery cost. In Year 1, VA compensation equals 180% of revenue, then falls to 140% by Year 5. Add 20% for training and QA and 15% for direct VA tools, before recruiting, backups, handoffs, and client review work. On the disclosed math, Year 1 delivery load is 215% of revenue before overhead.

That means the owner only keeps the spread, and in Year 1 that spread can be negative unless pricing, utilization, or scope improve. Weak QA turns into refunds, churn, and founder rework, so delivery quality is not a soft issue; it is a margin issue.

Track the labor spread

Build the plan from four inputs: client billing, VA pay, QA and training load, and tools. Then add recruiting time, backup coverage, handoffs, and client review work so the model matches real cash outflow, not just paid hours.

Watch delivery cost as a % of revenue, plus refund rate and rework hours. If quality stays consistent, a managed team can raise total owner economics; if not, growth just adds labor cost and lowers take-home pay.