How Much Webinar Production Owners Can Make With A $120k Pay Model

You’re trying to turn live webinar projects into owner income, not just busy production days This five-year model separates revenue, profit, reserves, and owner take-home before taxes, using $120,000 annual founder pay, $7,150 monthly fixed overhead, and 79% to 85% contribution margin after listed revenue-based costs

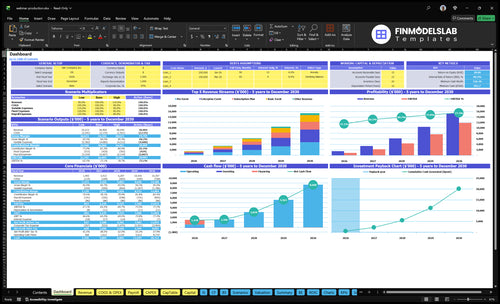

Owner income$120kNet margin79%–85%Revenue for target pay$31.7kBusiness difficultyHard

Want the six owner income drivers?

1

Booked Volume

5-32h

More booked webinars fill 5 to 32 billable hours per event, so fixed staff gets used better and owner take-home rises fastest.

2

Package Price

$500-$7.5K

The Year 1 package spread runs from $500 to $7,500, so pushing more jobs into higher-priced events lifts revenue fast.

3

Delivery Margin

79%-85%

Contribution margin moves from 79% to 85%, so more of each sale reaches owner pay after direct delivery costs.

4

Subscription Mix

15%-30%

Subscription plans grow from 15% to 30% of mix by Year 5, which steadies recurring income and cuts one-off swings.

5

Pipeline Quality

$500->$400

CAC drops from $500 to $400, so the same marketing budget buys more booked work and growth costs less.

6

Overhead Control

$7.15K/mo

Fixed overhead sits near $7,150 a month, so tight reserve discipline keeps cash from getting squeezed when bookings lag.

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

Want to check owner income in Webinar Production?

Open the Webinar Production Financial Model Template to review the dashboard, income outputs, assumptions, and scenario testing. It maps revenue forecast, margin bridge, staffing, marketing, overhead, capex, reserves, and owner pay. Open the model.

Owner-income model highlights

$120k founder salary

$7,150 fixed overhead

79% to 85% margin

$50k to $250k marketing

What profit margin can a webinar production business make?

If you’re sizing Webinar Production, the first cut is strong: Year 1 direct revenue costs are 21% total, so the gross margin is 79%; see What Is The Estimated Cost To Open, Start, And Launch Your Webinar Production Business? for the setup-cost side. Operating margin is lower, because it’s what’s left after payroll, fixed overhead, and marketing, and payroll rises from $165,000 in Year 1 to $650,000 in Year 5. By Year 5, the contribution margin improves to 85%, but low overhead still doesn’t mean high take-home.

Gross margin math

5% platform licenses

3% streaming and encoding

8% sales commissions

5% promotional assets

Operating margin watch

Year 1 contribution margin: 79%

Year 5 contribution margin: 85%

Payroll grows to $650,000

Year 1 payroll starts at $165,000

How many webinars per month replace a $120,000 salary?

To replace a $120,000 salary in Webinar Production, you need about $31,700 in monthly revenue at a 79% contribution margin before capex and reserves. That’s roughly 32 Basic Events at $1,000, 12 Pro Events at $2,625, or 4 Enterprise Events at $7,500. At a blended $2,488 per Year 1 customer unit, you need about 13 units; count projects, not just clients, because one client may buy a series, subscription, or add-ons.

Revenue math

$31,700 monthly target

79% contribution margin

32 Basic Events

12 Pro Events

Client mix

4 Enterprise Events

13 blended units

Separate projects from clients

One client can buy add-ons

How much can a webinar production owner pay themselves?

A Webinar Production owner can pay themselves $120,000/year, or $10,000/month before taxes, only when cash flow supports it—not as a guaranteed salary. Year 1 needs about $31,700/month in revenue before capex and reserves to cover that pay, What Is The Most Important Metric To Measure The Success Of Webinar Production Business?, 0.5 Technical Director FTE, $7,150 fixed overhead, and $50,000 annual marketing.

Owner Pay Math

Target pay: $10,000/month

Annual founder pay: $120,000

Required revenue: $31,700/month

Annual run-rate: $380,400

Cash Flow Risks

Fixed overhead: $7,150/month

Marketing budget: $50,000/year

Technical staffing: 0.5 FTE

Owner production tightens sales time fast

Key Takeaways

Booked webinar volume works only with enough coverage.

Higher fees need clearer scope to keep closing.

Recurring subscriptions smooth cash flow and staffing.

Payroll, overhead, and reserves cut owner take-home.

Compare lean, base, and high owner-income cases

Owner income scenarios

Owner income swings with booking mix, CAC, and fixed payroll. Low cases leave the founder near salary only; high cases depend on a heavier enterprise and subscription mix.

Three ways the founder's take-home can look.

Scenario

Low CaseDownside case

Base CaseBase case

High CaseUpside case

Launch model

Owner income stays tight because the business is still below break-even and extra distributions are unlikely.

Owner income is centered on salary and modest draws once the model reaches break-even.

Owner income improves as the mature mix skews more to Enterprise and Subscription work with stronger contribution margins.

Typical setup

Lean booking volume, mostly Basic and Pro Events, with fixed overhead and founder salary absorbing most cash.

Year 1 break-even is about $31,700 monthly before capex and reserves, with a 79% contribution margin, $120,000 founder pay, and $7,150 monthly fixed overhead.

The model uses mature-year assumptions, a 85% contribution margin, $250,000 marketing, $400 CAC, and a heavier Enterprise plus Subscription mix.

Cost drivers

Under-break-even revenue

$120,000 founder pay

$7,150 monthly overhead

weaker add-on mix

higher CAC

79% contribution margin

Month 3 breakeven

$120,000 founder pay

$7,150 monthly overhead

$50,000 marketing

85% contribution margin

$250,000 marketing

$400 CAC

higher Enterprise mix

higher Subscription mix

Owner income rangeBefore owner reserves

Founder salary onlyLow income

Founder pay plus modest drawsBase income

Salary plus strong drawsHigh income

Best fit

Use this to stress-test the business if sales ramp slowly or margins stay thin.

Use this as the most practical planning case for day-to-day owner compensation.

Use this to test upside if sales scale cleanly and the mix shifts toward larger, recurring accounts.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Webinar Production Core Six Income Drivers

Booked Webinar Volume

Booked Webinar Volume

Booked webinar volume is the number of webinars sold and delivered each month, weighted by billable hours, not just event count. In Year 1, the work mix is 8 hours for Basic, 15 for Pro, 30 for Enterprise, 20 for Subscription, and 5 for Add-On work, so more bookings only help income if producer coverage and rehearsal time keep up.

When volume rises without enough support, prep gets rushed, show-day risk rises, and retention can weaken. That hits owner pay twice: first through missed or delayed revenue, then through higher rework and labor strain against $7,150 in monthly fixed overhead and $165,000 in Year 1 payroll.

Track hours, not just events

Measure booked load as billable hours per month versus available producer hours. The key inputs are package mix, rehearsal slots, backup coverage, and post-event follow-up time, because those drive whether extra bookings turn into profit or just calendar stress.

Track booked hours by package type.

Reserve rehearsal and backup time.

Compare load to payroll and overhead.

Here’s the quick test: if bookings grow but coverage does not, margin can fall even as revenue rises. Keep enough slack for live support and fixes, or the owner ends up paying for growth with overtime, churn risk, and weaker take-home income.

Sales Pipeline Quality

Sales Pipeline Quality

Sales pipeline quality is the share of leads that fit webinar production work and can buy at the right price. Better-fit clients support higher pricing, retainers, and repeat programs, so this driver affects revenue and cash flow, not just lead count. With marketing spend rising from $50,000 in Year 1 to $250,000 in Year 5 and CAC improving from $500 to $400, the pipeline has to get tighter, not just bigger.

Here’s the quick math: $50,000 at $500 CAC implies about 100 acquired customers; $250,000 at $400 CAC implies about 625. If lead quality slips, the owner spends more time on weak calls and sales gaps widen, which delays cash and cuts take-home pay. The real risk is paying for activity that does not turn into repeat work.

Tighten Lead Fit Before You Scale Spend

Track lead source, close rate, and repeat rate by client type: single-event, subscription, and add-on work. A clean pipeline means more calls end in the right package, not just any package. Review rejected deals and long-cycle deals each month; if they cluster around low-budget or unclear-scope prospects, positioning is too broad and the owner’s calendar is getting burned on poor-fit sales work.

Set a simple gate: only pursue prospects that match your webinar scope, budget, and timing. Then test whether higher-fit leads lift retainers and repeat programs while keeping CAC near $400 instead of drifting above $500. If close rate improves, sales gaps shrink, and more of the owner’s time goes to delivery and profitable accounts instead of chasing weak leads.

Overhead And Cash Reserves

Overhead and cash reserves

Overhead is the monthly cost base that gets paid before the owner takes profit. For a webinar production business, that includes platform costs, streaming fees, office rent, insurance, software, internet, accounting, travel, marketing, equipment, and reserves. With $7,150 in fixed overhead each month, that is $85,800 a year before the owner pays themselves.

Cash reserves matter because live production has backup risk: gear fails, a client delays payment, or a month comes in light. Launch equipment of $25,000 for camera kits plus $8,000 for microphones ties up $33,000 in cash, so distributions should wait until the business can cover slow months and replacement needs.

Control overhead before owner draws

Track fixed costs separately from event costs so you can see the real break on owner income. Keep a simple monthly list for platform, software, rent, insurance, accounting, internet, travel, and marketing, then compare it to booked webinar revenue before paying draws. If overhead rises faster than bookings, take-home pay falls fast.

Set a reserve policy before distribution day. Hold back enough cash for slow periods and emergency backup capacity, then review it after each month-end close. One clean rule: no owner distribution until overhead, upcoming vendor bills, and reserve funding are covered. That protects delivery quality and keeps one bad month from hitting pay.

Recurring Webinar Production Revenue

Recurring Webinar Revenue

When subscription plans and repeat series grow, cash flow gets steadier. In this model, subscription share rises from 15% in Year 1 to 30% in Year 5, and pricing moves from $3,000 to $3,740 based on source hours and rates. That mix lowers sales gaps and gives the owner more predictable income.

The key input is recurring billable hours, not just event count. One-off webinars are lumpy, so the same team can swing between busy weeks and idle weeks. Recurring series make scheduling easier, support staffing, and reduce the risk that prep or live support gets rushed. If source hours fall below plan, the plan price needs a reset or margin slips.

Track source hours and plan mix

Measure subscription revenue as a share of total booked work. Track active series, monthly source hours, and realized price per hour. The useful test is simple: if subscription work keeps moving toward 30%, staffing is easier to plan and the owner can pay themselves from steadier cash instead of waiting on one-off closes.

Use source hours to price the plan. If delivery time rises but the plan stays at $3,000, margin gets squeezed and owner draw drops. Bundle planning, tech checks, live support, and follow-up into a fixed scope so the team can staff ahead of time. That is how recurring revenue stays profitable instead of just busy.

Average Package Fee

Average Package Fee

Average package fee is the price mix behind each booked webinar. With Year 1 fees at $1,000 Basic, $2,625 Pro, $7,500 Enterprise, $3,000 Subscription, and $500 Add-On, revenue shifts fast when more sales move into higher-scope work. The catch is simple: price only helps if delivery still fits the promise.

Here’s the quick math: higher fees lift owner income only when planning, tech checks, live support, recording, editing, reporting, and follow-up assets are really included. If the scope stays thin while the rate rises, close rate can fall, and the owner still has to cover $7,150 in monthly fixed overhead before pay improves.

Price the Scope, Not the Logo

Track average revenue per booked package by tier, then compare it with delivery hours. Year 1 workload runs from 5 hours for Add-On work to 30 hours for Enterprise, so a low fee on a heavy job can crush margin. Keep each quote tied to a clear scope sheet.

Booked packages by tier

Billable hours per package

Included scope and assets

Close rate after price tests

Raise price only when the offer also adds visible value. If you charge more, the client should see more planning, stronger live support, or better post-event assets. Otherwise, you risk fewer wins and the same workload, which cuts cash flow and leaves less profit for owner pay.

Delivery Labor Margin

Delivery Labor Margin

Delivery labor margin is the cash left after paying the people who produce, manage, and edit the webinar work. If the owner does everything alone, short-term margin can look better, but sales time and delivery capacity stay tight. Payroll starts at $165,000 in Year 1 and reaches $650,000 in Year 5, so owner pay depends on whether booked volume can support that labor load.

Track booked production volume in hours, not just event count. Basic jobs use 8 hours, Pro uses 15, Enterprise uses 30, Subscription uses 20, and Add-On uses 5. More staff can raise revenue, but each technical director, project manager, sales rep, marketer, and editor only helps if the calendar has enough paid work to cover their wage.

Match Hiring to Booked Hours

Start with a simple test: compare next-quarter booked hours to payroll. If booked work is thin, keep delivery lean and protect owner draw. If recurring series and add-ons are filling the calendar, add labor only when the new role has a clear hour load to cover. The goal is not bigger payroll; the goal is more profit per booked hour.

Track hours by package type.

Map payroll to booked work.

Watch owner draw after staffing.

Here’s the quick check: if a hire does not unlock enough extra billable hours, better delivery may not translate to better take-home. Tight staffing protects margin, but under staffing can also hurt close rate, retention, and repeat revenue. The sweet spot is enough labor to keep production smooth without letting payroll outrun booked demand.