How Much Window Cleaning Owners Can Make: $70K Pay, $840K EBITDA

Key Takeaways

Higher tickets help, but labor time drives margin.

Dense routes cut drive time and raise billable hours.

Recurring accounts stabilize cash flow and forecasting.

Fixed overhead and reserves limit true owner pay.

Owner income$70kNet margin27%-61%Revenue for target pay$476kBusiness difficultyHard

Want to estimate your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, labor, fixed overhead, marketing, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will change with demand, staffing, taxes, and reserve policy.

How much revenue does a window cleaning business need to make 100k?

If you want $100,000 of owner income from Window Cleaning, plan on about $155,000 in annual revenue just to cover $70,000 planned owner pay and $3,300 monthly overhead at a 29% variable-cost load. That is before marketing, reserves, and debt service, so the real revenue target is higher. Here’s the quick math: $109,600 in owner pay plus overhead, divided by 0.71, equals about $154,370.

Cost base

$70,000 planned owner pay

$3,300 monthly overhead

29% variable cost load

$39,600 annual overhead

Sales mix

Commercial tickets start at $250

One-time jobs start at $150

Repeat customers cut sales pressure

Recurring work helps stabilize revenue

What is a good profit margin for a window cleaning business?

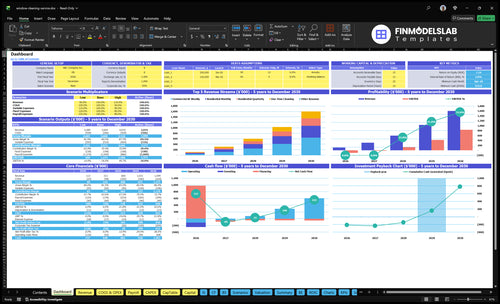

A good profit margin for Window Cleaning is a positive operating margin after labor and overhead, not a tax-deduction story. In this model, EBITDA moves from -$98,000 in Year 1 to $130,000 in Year 3 and $840,000 in Year 5, while variable costs drop from 29% to 20%; for launch costs, see How Much Does It Cost To Open And Launch Your Window Cleaning Business? With $39,600 a year in fixed overhead and a $636,000 minimum cash need, the real test is whether the business can fund the ramp long enough for labor, supplies, vehicle costs, and software to improve.

Margin drivers

29% variable costs in Year 1

20% variable costs by Year 5

Labor and supplies must tighten

Vehicle and software costs must improve

Cash and scale

-$98,000 EBITDA in Year 1

$130,000 EBITDA in Year 3

$840,000 EBITDA in Year 5

$636,000 minimum cash need

How much can a solo window cleaning business owner make?

Moving from $65 residential cleans to $250-$290 commercial runs pushes revenue per stop up fast, and that goes straight to owner income.

2

Route Density

$15K-$100K

Clustered routes cut drive time and let one crew finish more billable jobs from the same schedule, which raises take-home without adding staff.

3

Recurring Mix

90%

A heavier recurring mix keeps the calendar full after the first sale, so revenue is less choppy and breakeven gets easier to hold.

4

Crew Productivity

29%-20%

Better crew flow keeps labor, supplies, fuel, and software closer to the 29%-20% cost band, so more gross profit stays in the business.

5

Capacity Utilization

Month 22

Fill the schedule well enough to cross Month 22 breakeven and the model starts turning EBITDA positive, which is when owner income has room to grow.

6

Overhead Control

$3.3K/mo

Holding office, insurance, and admin near the $3.3K monthly base matters because fixed costs and $70K owner pay can wipe out margin when jobs slow.

Window Cleaning Core Six Income Drivers

Average Ticket

Average Ticket

Average ticket is the revenue per stop. For window cleaning, it goes up when pricing reflects panes, access, height, screens, tracks, and add-ons. Source prices in the model range from $45 for residential quarterly service to $290 for commercial bi-weekly by Year 5, so the same crew day can produce very different owner income.

The key limit is labor time, not invoice size. A tall or complex job can look strong on sales but still hurt profit if it takes too long, needs rework, or slows the route. Higher ticket only helps when the extra dollars beat the extra minutes.

Price by complexity

Track revenue per stop, labor minutes, and gross margin (money left after direct labor) by job type. Quote extra for height, hard access, screens, tracks, and add-ons, then compare the price to the time the crew actually spends onsite. If a job pays more but burns more labor, it can still cut owner take-home.

Job type and frequency

Minutes on site

Drive time

Add-on price

Rework rate

1

Job Volume And Route Density

Job Volume And Route Density

When more jobs sit close together, a crew spends less time driving and more time billing. In window cleaning, that lifts revenue per crew day and can pull vehicle operating costs from 6% of revenue toward 4%, so the same sales can produce more owner profit and more cash available to pay wages, taxes, and the owner draw.

The key inputs are jobs per crew day, travel minutes between stops, cancellation rate, weather loss days, and technician capacity. Here’s the risk: a strong spring route can look better than it is if you annualize it without a slow-season adjustment. More volume only helps if the route stays dense and the schedule stays full.

Measure Density, Not Just Bookings

Track how many jobs each crew completes in one area, how far apart the stops are, and how much of the day is paid work versus drive time. If drive time drops and billable time rises, margin improves fast. If jobs are spread out, fuel, wear, and dispatch time eat the gain.

Jobs per crew day

Average drive time between stops

Cancellation and weather loss rate

Route density by zip or zone

Use a simple forecast: more nearby jobs should raise paid hours faster than vehicle cost. But to be fair, the ceiling is real. Sales pipeline, technician capacity, and weather can block growth, so build routes around repeat areas instead of chasing one-off jobs across town.

2

Recurring Account Mix

Recurring Account Mix

Recurring account mix is the share of monthly residential, quarterly residential, bi-weekly commercial, and one-time jobs. A stronger recurring mix steadies revenue, lowers replacement sales pressure, and makes owner pay less volatile. Here’s the quick math: bi-weekly commercial pricing starts at $250 and reaches $290 by Year 5, so repeat work can carry more of the monthly base without rebuilding demand every week.

What this driver hides is that one-time work can lift a busy month but does not protect cash flow. If recurring accounts drop, marketing spend usually has to rise to refill the calendar. Commercial stops may pay less per visit in some markets, but the frequency and route efficiency can improve forecasting, labor planning, and profit stability. Stable mix = steadier owner draw.

Track Mix, Not Just Volume

Measure the share of revenue and stops from each account type, not just total jobs. The key inputs are account count, service frequency, average ticket, retention rate, and route density. A clean forecast starts with recurring stops per route, then adds one-time jobs as upside.

Monthly residential accounts

Quarterly residential accounts

Bi-weekly commercial accounts

One-time cleaning jobs

Push for a mix that fills gaps in the route and keeps crews busy. If a lower-price recurring stop cuts drive time and improves scheduling, it can lift gross margin more than a higher-ticket one-time job that adds travel and churn risk. Track cancellations, rebooking speed, and the dollars tied to each recurring slot.

3

Crew Productivity

Crew Productivity

When the owner stops doing field work and starts managing technicians, take-home pay only improves if each crew hour creates more billable work than it costs. In this model, direct technician labor and payroll taxes are 15% of revenue at the start and can fall to 11% as crews get more productive, so a 4-point swing matters fast. Owner labor is not free, so slower crews can wipe out the gain from hiring.

Here’s the quick math: on $100,000 of revenue, that gap is $4,000. That is money that can go to owner pay, overhead, or cash reserve. The risk is real: training time, rework, and dispatch gaps can push payroll up before output catches up, so the crew has to beat the added cost of supervision.

Track billable output per tech hour

Measure revenue per labor hour, payroll tax burden, rework rate, and non-billable drive time. If you do not know how many crew hours turn into paid jobs, you cannot tell whether hiring is helping or hurting owner income. Keep a simple weekly view: jobs completed, labor hours used, and any redo work that eats margin.

Use a tight dispatch plan and train to one standard job method. Cut the hidden cost of supervision by documenting prep, cleaning, and closeout steps, then review the numbers every week. If adding a technician does not lower labor cost as a share of revenue toward 11%, the owner is likely buying busier days, not better profit.

4

Seasonality And Capacity Utilization

Seasonality and Capacity Utilization

This driver is about how much of the year turns into billable work. In window cleaning, income is strongest in spring, summer, and fall, but weather cancellations can cut billable days and push jobs into already full weeks. Utilization means the share of available crew days that get billed, and it drives revenue, cash flow, and owner pay.

Estimate it with booked jobs, cancellation rate, available crew days, and recurring commercial and maintenance mix. Don’t multiply peak-month revenue by 12; that hides slow months, and breakeven at Month 22 shows the early ramp has to be strong.

Booked billable days by month

Weather-cancel rate

Recurring account share

Backlog by crew week

Protect the slow months

Track billable days by week, not just sales dollars. Recurring commercial and maintenance plans smooth cash flow and keep crews moving when residential demand slows. If the calendar is full, raise prices or defer low-value work instead of stacking overtime, because crowded weeks can lift revenue but hurt margin.

Measure billable days weekly

Track cancellation losses

Fill gaps with recurring work

Protect margin in peak weeks

5

Overhead And Reserves

Control Overhead and Reserves

Owner pay rises when fixed overhead stays at $3,300 per month and the business does not let insurance, software, and replacement gear drift up. Here’s the quick math: that is $39,600 a year before variable field costs. If overhead grows faster than recurring revenue, profit can look fine on paper but cash available for the owner shrinks fast.

The bigger strain is cash planning. This model carries $130,000 of capex across vans, equipment, setup, website, safety gear, and supplies, plus annual marketing that rises from $15,000 to $100,000. With a $636,000 minimum cash need, not all profit is owner pay. One clean rule: protect reserves before taking draws.

Track Cash Before Taking Draws

Measure overhead as a percent of collected revenue, not booked sales. Track monthly fixed costs, marketing spend, repair and replacement timing, and cash on hand against the $636,000 minimum need. If marketing jumps toward $100,000 a year, the owner should test whether new recurring accounts cover that spend before increasing salary or profit draws.

Fixed overhead: $3,300 per month

Capex reserve: $130,000 total

Marketing range: $15,000 to $100,000

Cash floor: $636,000 minimum

Use a simple payout rule: only distribute profit after paying for replacements, insurance, software, and growth spend. If cash drops below the reserve target, owner income should pause even if the income statement shows profit. That keeps the business funded through slow weeks, gear failures, and higher ad spend.

6

Window Cleaning Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with route density, recurring accounts, and fixed crew costs. Year 1 can stay near salary-only, while Year 3 and Year 5 profit levels raise take-home.

Shows how pay changes as recurring routes, staffing, and cash needs improve.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Early ramp keeps owner income near salary-only levels while EBITDA stays negative and cash needs stay high.

A modeled mid-case with a maturing crew and more recurring jobs lifts owner income above salary.

A stronger recurring-account mix and higher volume push owner income well past salary.

Typical setup

Year 1 setup with $70,000 owner salary, -$98,000 EBITDA, and 29% variable costs.

Year 3 setup with $130,000 EBITDA, 24.5% variable costs, and a stronger recurring mix.

Year 5 setup with $840,000 EBITDA, 20% variable costs, and higher-volume recurring accounts.

Cost drivers

29% variable costs

$75 CAC

$15k marketing budget

$70k owner salary

fixed overhead $3.3k/month

24.5% variable costs

$65 CAC

$50k marketing budget

added dispatch/admin payroll

stronger recurring mix

20% variable costs

$55 CAC

$100k marketing budget

larger support payroll

higher recurring volume

Owner income rangeBefore owner reserves

$70,000 salary, -$98,000 EBITDALow income

$70,000 salary, $130,000 EBITDACore income

$70,000 salary, $840,000 EBITDAUpside income

Best fit

Use this to stress-test launch-year cash strain and a large reserve buffer.

Use this if you expect a stable small crew and can fund the run to Month 22 breakeven.

Use this if you can win larger recurring accounts and hold the payback path to Month 46.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model carries a $70,000 owner/operator salary, but actual take-home depends on profit and cash needs EBITDA is -$98,000 in Year 1, $130,000 in Year 3, and $840,000 in Year 5 Treat any profit distribution as optional until reserves, debt service, taxes, and reinvestment are covered

This model reaches breakeven in Month 22 and payback in 46 months The early drag comes from $130,000 of startup capex, $15,000 of Year 1 marketing, payroll, and fixed overhead of $3,300 per month A leaner setup could differ, but slower sales or weak routing can push payback out

You don’t need only commercial work, but recurring accounts help a lot The model uses residential monthly, residential quarterly, commercial bi-weekly, and one-time cleaning streams Commercial bi-weekly pricing starts at $250, while residential monthly starts at $65, so the best mix depends on route density, labor time, and repeat frequency

Average ticket, route density, recurring work, labor productivity, seasonality, and overhead control drive income In the model, variable costs fall from 29% of revenue in Year 1 to 20% in Year 5 That spread matters because every saved point can support owner pay, reserves, or growth spending

Build dense recurring routes before adding overhead Start with pricing discipline, repeat residential plans, commercial maintenance routes, and tight scheduling Watch the big cost lines: technician labor at 15% of revenue in Year 1, vehicle costs at 6%, software at 3%, and fixed overhead at $3,300 per month

About the author

Caleb Ross

Small Business Advisor

Caleb Ross is a small business advisor at Financial Models Lab who helps first-time entrepreneurs plan startup costs before launch. He studies common expenses, revenue drivers, and launch requirements, then turns broad business ideas into clear planning assumptions. His work focuses on pricing and profitability basics, with a practical, research-based approach to building realistic forecasts.

Choosing a selection results in a full page refresh.