How long does it take to start a window cleaning business?

Window Cleaning usually takes 2–6 weeks to start at a small scale if registration, insurance, tools, pricing, and lead channels move together. The slow spots are usually insurance approval, safe equipment sourcing, website and booking setup, first-customer acquisition, and hiring if you open with a crew. The fastest path is an owner-operator model focused on residential and storefront jobs before heavier commercial routes.

Fast launch path

2–6 weeks for a small launch

Owner-operator starts fastest

Residential jobs come first

Storefront jobs build early cash

Common delay points

Insurance approval can slow opening

Safe tools take time to source

Website and booking need setup

Crew hiring pushes launch later

What mistakes can delay a window cleaning business launch?

The biggest launch mistakes in Window Cleaning are pricing before route math, skipping insurance and ladder safety, and opening before the workflow can quote, book, clean safely, collect payment, and request a review. For this model, vehicle operating costs are about 6% of Year 1 revenue and direct labor plus payroll taxes are about 15%, so bad pricing can crush margins fast. Fix those blockers before adding crews or commercial accounts.

Pricing and safety

Price after route math

Do not skip insurance

Train ladder safety first

Use clear, written quotes

Launch readiness

Test the full workflow

Keep scheduling tight

Request reviews every job

Scale only after basics work

How do you get window cleaning customers?

If you’re starting Window Cleaning, your first customers come from narrow local action: neighborhoods, door hangers, referral offers, a complete local business profile, basic service pages, real estate agents, storefront canvassing, and property managers. For the quick math, a $75 Year 1 CAC cap and a $15,000 marketing budget mean every paid lead should prove booking flow before you scale; How Much Does It Cost To Open And Launch Your Window Cleaning Business? helps frame that spend.

Start local

Hit one neighborhood at a time.

Use door hangers and referral offers.

Build a full local business profile.

Send simple service pages to prospects.

Watch the numbers

Keep paid lead cost near $75.

Test $150 residential jobs first.

Push $250 bi-weekly commercial accounts.

Get photos, reviews, and repeat reminders.

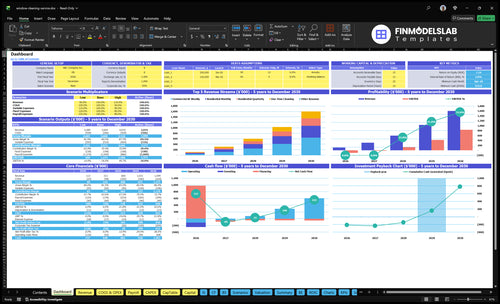

Window Cleaning Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Confirm day-one readiness before accepting paid window cleaning jobs

Launch readiness checklist

Use this go-live approval checklist before opening to confirm the business is ready to start service.

1Compliance

Entity setup filedCritical

The business needs a legal entity before contracts, banking, and permits move ahead.

Local permits reviewedCritical

City and county rules can block launch if the service license path is unclear.

Insurance boundCritical

General liability coverage should be active before any customer work starts.

Workers comp path setHigh

Set this before hiring so labor risk is covered from the first crew member.

2Safety

Ladder rules documentedCritical

Clear ladder rules reduce fall risk on residential and low-rise jobs.

Chemical handling sheet readyHigh

Crew needs safe handling steps for glass cleaners and any site-specific chemicals.

Vehicle safety checklist doneHigh

A vehicle check catches issues before crews drive to the first job.

3Equipment

Vans and gear purchasedCritical

The two vans and core gear must be ready before service routes can start.

Initial supply kit stockedHigh

Supplies for Month 1 jobs should be on hand so crews do not miss appointments.

Backup tools loadedMedium

Backup tools lower downtime when a squeegee, pole, or pump fails in the field.

4Pricing

Pricing sheet approvedCritical

Pricing must match the plan: $65 monthly, $45 quarterly, $250 bi-weekly, $150 one-time.

Quote form testedHigh

A standard quote form keeps estimates fast and consistent across jobs.

Booking and payment liveCritical

Customers need a working path to book, confirm, and pay without delays.

Review request flow readyMedium

Reviews help the first lead channel convert faster and support local trust.

5Dispatch

Route plan finalizedCritical

No route plan means higher fuel costs and missed appointment windows.

Coverage schedule confirmedHigh

The opening schedule should cover calls, arrivals, and same-day follow-up.

Crew trained on standardsCritical

Training must cover window finish quality, customer handoff, and safety steps.

6Finance

Cash runway reviewedCritical

Year 1 EBITDA is negative, so launch cash must cover setup and early losses.

Breakeven path reviewedHigh

The model reaches breakeven in Month 22, so sales pace must build fast.

Go-live signoff completeCritical

Final signoff should confirm compliance, tools, staffing, pricing, and cash are ready.

Which launch drivers matter most before opening?

1Service Mix

2-6 wk scope

Pick residential, commercial, or mixed routes first; scope shapes tools, pricing, and sales speed.

2Legal Safety

$400/mo

Certificates, liability coverage, and stop-work rules must be ready before the first paid job.

3Equipment Setup

$95K capex

Two vans and core gear must match the sales promise, or callbacks and delays rise.

4Pricing Quotes

65/45/250/150

Set recurring and one-time pricing early so quotes hold margin and route density.

5Lead Flow

$15K / $75 CAC

Year 1 marketing at $15K and $75 CAC implies about 200 customers if it performs.

6Staffing QC

Month 1 team

Owner, dispatch, and admin must train on checklists, photos, and reviews to protect repeat work.

Service Mix And Territory

Service Mix & Territory

Your launch scope decides whether you can open on time. A mixed Year 1 plan of 40% residential monthly at $65, 35% residential quarterly at $45, 15% commercial bi-weekly at $250, and 10% one-time jobs at $150 changes pricing, route design, and the first sales channel. If you try to serve every segment at once, quotes slow down and day-one capacity gets thin.

Residential work needs trust and reviews, storefront routes need tight scheduling, and commercial accounts need insurance certificates plus recurring reliability. That means the territory plan has to match the service mix before launch. A broad, unfocused area adds drive time, delays first visits, and creates missed windows that can hurt early revenue and customer confidence.

Lock the first route map

Before opening, decide which segment leads the launch and write the quote rules, service area, and sales channel for that mix. Match the tool list, vehicle setup, and safety process to the work you will sell first, not the work you hope to sell later. One clear scope beats three half-ready ones.

Verify these inputs before taking bookings:

Residential trust plan and review flow

Storefront route ZIPs and visit cadence

Commercial certificate timing

Pricing for $65, $45, $250, $150

Job type, access, and travel limits

1

Legal, Insurance, And Safety Readiness

Insurance And Safety Readiness

If you open without local registration, license, tax setup, and insurance certificates, commercial clients can reject you before the first job. General liability is modeled at $400/month, so it belongs in launch cash, not later. One missing certificate can delay a paid account even when the crew and tools are ready.

Safety readiness also sets day-one capacity. The operating plan needs written rules for ladders, low-rise work, water-fed poles, scrapers, chemicals, vehicles, and job-site photos. If workers compensation is not planned before employees start, hiring can stall and the owner may have to stay solo longer than planned.

Prepare Proof Before Selling

Verify every local filing before marketing. Get the certificates, written procedures, and stop-work rules in place before the first paid job so the team can pause unsafe work, document issues, and keep commercial prospects moving through approval.

Confirm registration, license, tax rules.

Issue insurance certificates early.

Write ladder and chemical rules.

Train photos, access, and stop-work.

The readiness signal is simple: a customer can ask for paperwork on day one and get it fast. That lowers trust friction, speeds commercial approval, and keeps launch from slipping while you fix compliance gaps.

2

Equipment, Vehicle, And Supply Setup

Equipment And Vehicle Readiness

Your opening date depends on whether you can actually do the work you sell. The minimum viable setup is squeegees, scrubbers, buckets, towels, scrapers, cleaning solution, basic safety gear, and vehicle storage. That gets you started, but it only supports limited jobs. If you plan to sell harder-to-reach or higher-value work, you need the expanded setup ready before first revenue.

The modeled launch package adds up fast: 2 vans at $60,000, specialized equipment at $25,000, safety equipment and training gear at $7,000, and initial supplies at $3,000, or $95,000 total. Here’s the risk: if your tools can’t match your sales promises, you get delays, reschedules, and weak first-day service quality.

Stage The Right Kit Before Booking

Build the checklist in two layers. First, verify the minimum tools are on hand and packed for same-day use. Then confirm the expanded items are ordered, delivered, and tested before you sell jobs that need ladders, a water-fed pole system, screen and track tools, or training gear. That keeps your launch plan tied to real capacity, not hopeful selling.

Use one simple test: can the crew complete the exact work promised on the first invoice without borrowing gear? If the answer is no, delay those bookings or narrow the service scope. One clean rule helps here: sell only what the truck can carry and the crew can use safely.

3

Pricing, Quoting, And Scheduling

Pricing and Route Scheduling

Window cleaning can’t market until pricing is set. If you start with vague quotes, you’ll leak margin on every hard-access job, then lose time to callbacks and rework. Year 1 planning prices are $65 residential monthly, $45 residential quarterly, $250 commercial bi-weekly, and $150 one-time, so the offer has to be clear before the first lead comes in.

The launch risk is simple: bad pricing slows opening and breaks day-one cash flow. The quote process should capture window count, access height, screens, tracks, hard water, travel time, and frequency. Scheduling should cluster jobs by ZIP code to protect route density, or you’ll waste drive time and lose clean-ups that should have fit the route.

Build the Quote Before Ads

Set the rate card, then lock the quote form, then open marketing. That order matters because every lead needs the same math on day one, not a custom guess. Use one pricing rule for each service type, and document when a job moves from standard cleaning to an exception because of height, heavy buildup, or extra travel.

Confirm all four price points first.

Test the quote form on real jobs.

Group routes by ZIP code.

Track quote adds for hard water.

Reject jobs that kill route density.

What this setup hides is calendar waste. If estimates are slow or inconsistent, openings slip, crews wait, and your first booked jobs won’t turn into reliable repeat service.

4

Launch Marketing And Lead Flow

First-30-Day Bookings

This launch lives or dies on getting paid jobs in the first 30 days. If lead flow is weak, the schedule stays thin, cash burns, and the team can’t prove route density or daily operating rhythm from day one.

Here’s the quick math: the Year 1 marketing budget is $15,000 and modeled CAC is $75, so the plan expects about 200 customers if channels perform. The inputs are a local business profile, simple website, neighborhood outreach, door hangers, referral asks, real estate agents, storefront canvassing, property managers, and reviews.

Test Channels Fast

Set up lead source tracking before spending a dollar, or you won’t know which channel fills estimates. The readiness signal is simple: booked estimates, a review workflow, and clean tracking by source so you can cut weak channels fast and scale the ones that book jobs.

Track every estimate by source.

Ask for reviews after each job.

Test channels before scaling spend.

Use booked estimates as the trigger.

One clean rule: if a channel does not produce booked work in the launch window, it is a delay risk, not a growth asset. That matters because a service business needs customers ready to pay before the first route day, not just awareness.

5

Staffing, Training, And Quality Control

Crew Training and QC

Opening on time depends on the crew being trained before the first route. The Month 1 model is lean: 1.0 owner or operations manager, 0.5 customer service or dispatch, and 0.5 bookkeeper/admin. That mix only works if one person can cover scheduling, job follow-up, and cash capture without gaps. If onboarding slips, arrival windows and repeat-service quality slip too.

Training has to cover safety, arrival windows, job checklists, photo proof, customer notes, payment capture, and review requests. One missed checklist can turn into a callback, and callbacks eat route capacity fast. The 0.5 FTE sales and marketing coordinator in Month 13 only helps if the service team already delivers clean first visits.

Day-One QA

Train on a live schedule before launch, not after. Use one written checklist for every job, then test it on a small route until arrival times, photos, notes, and payment capture are done the same way every time. If callback rates rise in the first weeks, pause new bookings and fix the process before adding demand.

Start with a narrow residential or storefront route and only sell jobs you can complete safely Use the same launch basics: registration, local license checks, insurance, tools, pricing, booking, and review requests The planning case uses $150 one-time jobs, $65 monthly residential jobs, and a $75 Year 1 CAC, so track whether part-time leads pay back

The researched model reaches breakeven in Month 22 and payback in Month 46 That assumes a broader launch with vehicles, equipment, staff, marketing, and fixed overhead A lean owner-operator path may behave differently, so use the model to test actual job volume, pricing, route density, and hiring timing before committing to a larger setup

Yes, plan for general liability before taking paid jobs, even on residential work The model carries business insurance at $400/month If you hire, workers compensation may apply based on state rules Insurance also helps with trust, property damage concerns, ladder work, and commercial prospects that ask for certificates before approving work

Delays usually come from insurance approval, safe equipment sourcing, website and booking setup, first customer acquisition, and hiring The launch range is 2-6 weeks for a small operator, but larger setups add more dependencies In this plan, vans, specialized equipment, safety gear, supplies, and online booking are staged across the early launch months

Define the service area and job type before buying too much equipment Residential monthly, residential quarterly, commercial bi-weekly, and one-time jobs have different prices, sales cycles, and safety needs Then verify local rules, bind insurance, write a quote process, and book a few test jobs before adding staff or heavier commercial work

About the author

Nicholas Webb

Founder-Focused Content Writer

Nicholas Webb is a founder-focused content writer for Financial Models Lab who helps online business beginners make sense of business expense analysis and what it really costs to operate. He writes practical founder checklists and planning guides that support decisions before money is invested. With a calm, structured approach, he explains business costs clearly and without unnecessary jargon.

Choosing a selection results in a full page refresh.