Why test Sugar Mill launch assumptions before opening?

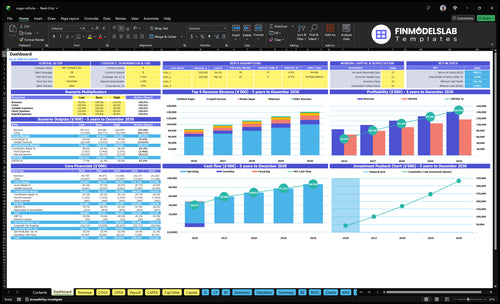

Launch validation: Sugar Mill Financial Model Template maps the 60-month ramp, Year 1 revenue of $8475M, Year 5 revenue of $14126M, cash, and break-even.

Launch model checks

60-month production ramp

Revenue by product line

Cash gap during commissioning

Break-even and overhead

What are the biggest sugar mill launch risks?

The biggest launch risk at a Sugar Mill is starting before feedstock, permits, wet commissioning, or buyer acceptance are ready, so if any of those are missing, delay the launch. Here’s the quick check: weak cane or beet commitments, slow permitting, poor wastewater planning, underpowered utilities, untested equipment, missing spares, thin staffing, and no quality system can break Year 1 before crushing season.

Launch readiness

Feedstock commitments are signed

Permits are fully in hand

Wastewater plan is approved

Utilities support full load

Model stress test

Test 175,000 forecast units

Keep logistics at 35% revenue

Check a slower ramp case

Delay launch if buyers are missing

How do sugar mills get first customers?

A Sugar Mill gets first customers by lining up letters of intent and offtake agreements before production, then selling to distributors, wholesalers, food manufacturers, beverage producers, bakeries, confectionery companies, and byproduct buyers; if you’re sizing the launch, see What Is The Estimated Cost To Open The Sugar Mill Business?. Revenue should start only after validated production runs, not trial batches, because buyers want product specs, lab results, packaging, delivery terms, credit checks, and sample approval. Modeled Year 1 sales are $600M refined sugar, $90M liquid sucrose, $75M brown sugar, $60M molasses, and $225M beet pulp.

Who to line up first

Letters of intent first

Offtake agreements next

Distributors and wholesalers

Food and beverage manufacturers

Bakeries and confectionery firms

Byproduct buyers for molasses and beet pulp

What buyers need ready

Product specs and grade

Lab results and sample approval

Packaging format and delivery terms

Credit checks before shipment

Use validated runs for first revenue

Match supply to each contract type

What permits are needed to open a sugar mill?

A Sugar Mill needs federal, state, and local approvals before it buys major equipment: zoning, building, environmental, safety, food facility, boiler, fire, wastewater, stormwater, and solid-waste permits. This is not legal advice; confirm the list by jurisdiction and discharge path, because permitting can control an 18–36+ month greenfield timeline and should be tracked alongside What Is The Most Critical Measure Of Success For Sugar Mill?.

Core launch permits

Confirm industrial zoning and land use.

Get building and site-plan approvals.

Secure boiler and pressure-vessel permits.

Pass local fire inspections.

Operating compliance

File US Environmental Protection Agency or state air permits.

Get wastewater and stormwater discharge approvals.

Register with the US Food and Drug Administration; renew every 2 years.

Prepare Occupational Safety and Health Administration readiness under 29 CFR 1910.

Confirm whether the sugar mill is ready to open safely and sell

Launch readiness checklist

Use this go-live approval checklist to confirm the sugar mill is ready before opening.

1Compliance

Zoning approval securedCritical

The site must be allowed for industrial food processing before buildout.

FDA facility registration filedCritical

Food plants need registration before they ship product.

State food license clearedCritical

State food rules can block production if they are missing.

OSHA and boiler review passedCritical

Worker safety and boiler controls must pass before hot operations start.

Emissions and discharge controls readyHigh

Air, stormwater, and wastewater controls must work before commissioning.

2Feedstock

Cane or beet contracts signedCritical

The mill needs secure feedstock before it can feed the line.

Grower pickup routes confirmedHigh

Harvest timing and haul routes protect crush volume and cut idle time.

Water, power, fuel lockedCritical

Processing stops fast if water, power, or boiler fuel is short.

Waste handling vendor bookedHigh

Byproducts and waste need a legal path out of the plant.

3Equipment

Extraction line wet-testedCritical

The extraction step must run before any steady output starts.

Evaporation and crystallization passCritical

These units set sugar yield and quality.

Centrifuge and tanks stableHigh

Separations and storage faults can stop the whole line.

Packaging line at speedHigh

Packaging must hold throughput so finished goods can ship.

4Quality

Lab methods validatedCritical

Quality tests need repeatable results before sale.

Sanitation program signed offCritical

Food plants need clean-down steps to protect product and audits.

Traceability records workHigh

Traceability helps isolate issues fast if a lot fails.

Product specs approvedHigh

Buyers need agreed sugar specs before first delivery.

5Staffing

Operators and supervisors hiredCritical

The line needs trained people on shift before start.

Maintenance coverage in placeHigh

Breakdowns are expensive if no mechanic is available.

Sanitation and QA staffedCritical

Food plants need cleaning and release checks every day.

Safety training completedCritical

Hazards rise fast around boilers, hot process, and forklifts.

6Launch economics

Year 1 output hits 175,000Critical

The model expects 175,000 total units across all products in Year 1.

Freight stays near 35% revenueHigh

Transport costs can erase margin if route density slips.

Commissions hold at 20%High

Selling costs need to stay inside the model or EBITDA drops.

Opening cash cushion confirmedCritical

Month 1 needs enough cash for delays, permits, and ramp-up.

Go-live signoff approvedCritical

Do not start shipments until permits, buyers, and wet commissioning are done.

Which six launch drivers decide sugar mill readiness?

1Feedstock Supply

100K units

Protects the first crushing season by locking contracted feedstock volume before you commit capital.

2Site Utility Readiness

Utility set

Cuts commissioning delays by confirming water, power, storage, and haul access before install.

3Permitting Controls

Permit gate

Lowers shutdown risk by tying permits and wastewater approvals to construction and start-up milestones.

4Equipment Procurement Commissioning

18–36+ mo

Reduces failed runs by completing dry runs, wet runs, lab checks, and performance tests before first sales.

5Operations Staffing QA

Shift-ready

Speeds buyer approval by staffing shifts and QA controls before commissioning starts.

6Buyer Offtake Readiness

$8.5B

Turns valid production runs into invoices faster when specs, samples, packaging, and credit are set.

Feedstock Supply

Feedstock Supply Gate

For a sugar mill, feedstock is a launch gate, not a buying task. Lock sugarcane supply contracts or sugar beet supply contracts before site commitment, or the plant can open with no crop to crush. Check grower volume, harvest timing, transport distance, storage limits, quality specs, and backup supply.

If contracted volume does not support the Year 1 plan of 100,000 refined sugar units plus byproduct streams, the first crushing season can slip and expensive equipment may sit idle while fixed costs keep running.

Contract the Crop First

Build the launch plan around signed volume, not verbal intent. Ask growers for delivery windows, haul distance, storage limits, and quality specs that match your process. One clean rule: no crop, no crush.

Match volume to Year 1 output.

Map harvest timing to opening date.

Verify backup supply before site lock.

Test transport distance and storage fit.

Before ordering major equipment, confirm that contracted tonnage can cover day-one operations. If the crop lands late, too far away, or below spec, the mill can miss its opening window and start with weak output instead of steady production.

1

Site And Utility Readiness

Site and Utility Readiness

A sugar mill cannot open on time if the site is still waiting on industrial zoning, water access, wastewater capacity, high-power service, or boiler fuel. If those basics are not locked before equipment install, the project turns into utility upgrades, blocked permits, or long-haul logistics fixes that push the launch back.

The readiness signal is simple: confirmed utility capacity before equipment installation. For a harvest-driven plant, that matters on day one because shutdowns in water, power, or storage flow straight into commissioning delays and missed production windows. That can stretch a build that is already sitting inside an 18-36+ month equipment and commissioning timeline.

Prebuild Utility Check

Start with the site, not the machinery. Confirm the parcel can handle truck or rail logistics, bulk storage, and proximity to growers before you sign a build plan. Then document the utility loads, wastewater path, and fuel supply so the engineering team can size the plant to the site instead of forcing a redesign later.

Verify zoning before lease or purchase.

Confirm water and wastewater capacity.

Lock power service with the utility.

Test truck and rail access routes.

Map storage space for harvest peaks.

If utility upgrades are still open when equipment arrives, cash gets tied up in idle assets and the first operating season becomes fragile. A clean launch needs the site ready to support intake, processing, storage, and outbound loading without stop-start workarounds.

2

Permitting And Environmental Controls

Permitting And Controls

A sugar mill can’t open on time if air emissions, wastewater treatment, boiler approvals, stormwater, and solid waste approvals are still open. Wastewater is the usual pinch point because sugar processing creates high-volume process water, and local inspections have to line up with buildout and start-up.

The readiness signal is permit status matched to construction and commissioning milestones. In a project with an 18–36+ month equipment timeline, permit delays are not paperwork; they can move the launch date, delay first commercial sugar sales, and raise shutdown risk in the first operating weeks.

Map The Permit Path Early

Start with the items that can stop startup: discharge limits, boiler specs, stormwater controls, waste handling, and inspection dates. Tie each one to the schedule so the team knows what must be approved before equipment tests, wet runs, and first production.

Map each permit to a milestone.

Document wastewater volumes early.

Confirm inspection timing in writing.

Assign one owner per agency.

What this hides: a late permit can leave labor, utilities, and installed equipment sitting idle while the mill waits to legally operate.

3

Equipment Procurement And Commissioning

Equipment Procurement and Commissioning

Equipment procurement and commissioning is a launch gate, not a shopping list. A sugar mill needs process engineering, cane or beet prep, juice extraction, evaporation, crystallization, centrifuges, tanks, controls, packaging, sanitation, spares, and maintenance access in place before first production. Long-lead equipment can stretch the timeline to 18-36+ months, so one late order can push the whole opening past the first crushing season.

Readiness is not “installed”; it’s completed dry runs, wet runs, lab checks, and performance validation. That’s what gives you clean buyer samples and fewer failed production runs on day one. If controls, sanitation, or spare parts are weak, you may open with a line that looks built but cannot hold spec or sustain output.

Lock the critical path early

Start with the longest items first and tie each one to a date, vendor, and install window. Keep a single tracker for lead times, utility hookups, spare parts, commissioning steps, and test results. One clean rule: if the line can’t pass a wet run, it’s not ready to sell.

Freeze equipment specs before ordering.

Map install access for maintenance.

Verify controls before commissioning.

Hold spares for startup failures.

Document lab checks and performance tests.

Assign one owner for each package so gaps don’t hide between vendors. If the mill can’t validate output against buyer specs, first shipments get delayed and rework costs rise right when cash is tight.

4

Operations Staffing And Quality Assurance

Operations Staffing and QA

For a sugar mill, staffed shift coverage before commissioning is what keeps opening on time. You need trained operators, maintenance technicians, QA staff, sanitation, safety, and shift supervision in place before first runs, or the mill can’t stabilize equipment, document controls, or fix defects fast enough to avoid launch delays.

Quality assurance means testing product specs and logging production controls. Food safety readiness also needs procedures, training, records, and corrective-action steps. Without that paper trail on day one, you may be able to make sugar, but you may not be able to prove consistent quality to industrial buyers.

Staff the Line Before the First Run

Map each shift role before startup: operators, mechanics, QA, sanitation, safety, and supervisors. Then verify coverage for nights, absences, and harvest peaks. Train the team on sampling, cleaning, hold-and-release, and incident reporting before the first wet run.

Procedures ready before commissioning

Training records signed and filed

Spec sheets set for release

Corrective-action steps tested on a real deviation

Use a launch file that lets the lab release product, the floor log deviations, and supervisors close issues the same day. That is what cuts rework, safety risk, and buyer approval delays.

5

Buyer And Offtake Readiness

Offtake Before First Run

Buyer and offtake readiness is what turns test production into cash. If bulk buyers, distributors, food manufacturers, beverage producers, bakeries, confectionery companies, and molasses or beet pulp buyers are not lined up early, the mill can finish a valid run and still have no invoice to send. That pushes opening risk from operations into cash flow, even when the plant is technically ready.

The key gate is signed terms before production readiness: product specs, sample plan, packaging decision, delivery lane, and credit approval. Without those, first-day sales can stall, shipments can wait on buyer setup, and early revenue can slip against the $8,475M Year 1 modeled revenue plan.

Lock Buyer Terms Early

Build the buyer file before startup. Get spec sheets, sample approval, packaging format, freight route, and credit limits agreed before the first commercial run. That lets you move from validated production to invoice-ready orders fast, instead of using finished inventory as a holding cost.

Track each buyer in the launch checklist: who approved quality, who approved packaging, who approved transport, and who approved credit. One clean line: no offtake, no smooth launch. If any step is missing, first shipments can miss the opening window and working capital needs go up fast.