ACH Payment Processing Startup Costs: $240k CAPEX Plus Reserves

Starting an ACH payment processing service in this researched plan requires $240,000 in capitalized launch assets plus funding for compliance, staff, reserves, and runway Year 1 revenue is modeled at $128 million from 2,000,000 standard transactions, 250,000 same-day transactions, and 15,000 return-handling events, but EBITDA is still -$399,000 during the first operating year A practical funding target should cover CAPEX, the Year 1 operating loss, and the $334,000 minimum cash need in Month 12, before any extra sponsor bank reserve or loss reserve Sponsor bank underwriting, licensing posture, platform depth, and transaction risk can materially change the ACH processing startup cost estimate

Calculate Fuding Needs

Startup Cost Summary

Shows startup CAPEX and excluded reserve cash for an ACH payment processing service.

Highlighted CAPEX$240,000Base planning example

Excluded cash needs$334,000Outside CAPEX total

Funding need$574,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

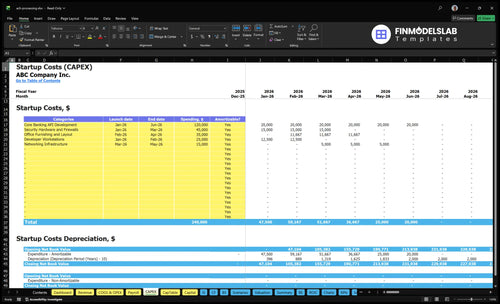

Core Banking API Development

$120,000

Month 1-6 build scope and integration complexity

Yes

Security Hardware and Firewalls

$45,000

Security stack size and control requirements

Yes

Office Furnishing and Layout

$35,000

Office setup scale and fit-out scope

Yes

Developer Workstations

$25,000

Headcount needs and workstation specs

Yes

Networking Infrastructure

$15,000

Network buildout scope and hardware needs

Yes

Working Capital Reserve

$334,000

Month 12 reserve for pass-through fees, transaction losses, bank holdbacks, and settlement timing

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only, so you can see launch CAPEX before non-CAPEX funding needs.

!

CAPEX limits This covers capitalized startup assets only. It excludes inventory, payroll runway, deposits, debt service, working capital, compliance subscriptions, cloud hosting, marketing, legal fees, and other operating costs. Launch spend is concentrated in Month 1 to Month 6, and the capitalized assets may be depreciated or amortized based on your accounting policy. Non-CAPEX funding is still required.

Lean setups keep more work with partners, while the base model buys owned tech and staff, and the full build adds deeper control, bigger teams, and more reserve cash.

Lean, Base, and Full launch cost bands for ACH processing.

Scenario

Lean LaunchPartner-led

Base LaunchCommercial plan

Full LaunchControl-heavy

Launch model

Launches faster in the startup period by using partner rails and a sponsor bank, with lighter compliance work in house.

Uses the modeled commercial launch with direct operations, sponsor bank setup, and Month 13 breakeven.

Launches slower because more of the stack, risk tools, and controls are built before scale.

Typical setup

Uses limited owned technology, a smaller internal team, and leaner reserve cash.

Builds the $240,000 CAPEX package and the $950,000 Year 1 payroll, with $28,200 monthly fixed overhead.

Expands the technology team, compliance staff, fraud tools, and reserve cash beyond the base model.

Cost drivers

Partner fees

lighter tech stack

outsourced compliance

small team

lower reserves

Core banking build

compliance and audits

payroll

fixed overhead

fraud tools

Platform build

risk tooling

added engineers

more compliance staff

higher reserve cash

Planning rangeCAPEX only

$250,000 - $400,000Low cash need

$550,000 - $650,000Model base case

$800,000 - $1,100,000Highest cash need

Best fit

Fits founders validating demand before a full build; partner dependence is the main tradeoff.

Fits a team ready to fund the modeled plan, including the $334,000 minimum cash need.

Fits operators who want more control and can fund a larger build; longer setup time is the tradeoff.

!

Planning note: These ranges are researched planning assumptions, not exact quotes; use them to frame launch funding, staffing, and reserve needs.

What are the hidden costs of starting an ACH payment processing service?

The hidden cost of an ACH Payment Processing Service is working capital, not just build spend: you still need prefunding, settlement reserves, and risk cash, even after the What Does It Cost To Run ACH Payment Processing Service? math is done. In the model, minimum cash hits $334,000 in Month 12 and Year 1 EBITDA loss is $399,000, which is separate from $240,000 CAPEX and from ongoing variable costs like 85% ODFI access and 40% fraud monitoring in Year 1.

Cash you must hold

Prefund customer settlements

Cover returned-item exposure

Hold sponsor bank reserves

Protect payroll runway

Costs people miss

Pay fraud losses

Buy cyber liability coverage

Carry E&O and fidelity coverage

Fund audits and legal reviews

How much money do you need to start an ACH payment processing company?

To start an ACH Payment Processing Service, plan on about $973,000 before extra bank reserves: $240,000 CAPEX + $399,000 Year 1 negative EBITDA + $334,000 minimum cash in Month 12. That is the launch-funding view, not just a software-build budget; see How Increase Profitability Of ACH Payment Processing Service? for margin levers. The model reaches breakeven in Month 13 and payback in Month 19.

Launch funding

$240,000 upfront CAPEX

$950,000 Year 1 payroll

$28,200 monthly fixed overhead

$399,000 Year 1 EBITDA loss

Cash caveats

Hold $334,000 cash in Month 12

Sponsor bank reserves can raise funding

Funds flow affects cash timing

Licensing posture and risk profile matter

How should founders build an ACH payment processing funding plan?

Build the ACH Payment Processing Service funding plan by splitting CAPEX, pre-opening expenses, cash runway, and reserve needs, then tie each one to transaction volume. Use the model as planning support, not the operating plan: Year 1 revenue is $128 million, Year 2 revenue is $4,378 million, breakeven is Month 13, and payback is Month 19. Price the base case at $0.45 per standard ACH, $1.25 per same-day ACH, and $4.50 per return in Year 1.

Base-case funding

Separate CAPEX from launch spend

Fund runway through Month 13

Set reserves for returns

Use volume assumptions first

Downside checks

Test slower volume cases

Test higher return rates

Test larger reserve needs

Test longer sponsor-bank onboarding

Key Takeaways

Compliance costs run $9,200 monthly before variable fees.

Core build needs $160,000 before launch.

Year 1 payroll is $950,000.

Minimum cash should cover $334,000 and losses.

ACH Payment Processing Service Core Five Startup Costs

Compliance, Regulatory, and Sponsor Bank Setup Startup Expense

Setup Scope

This cost covers legal structuring, licensing analysis, Nacha Operating Rules readiness, sponsor bank due diligence, risk reviews, compliance policies, audit planning, and ODFI onboarding. Use the fixed monthly baseline of $9,200, made up of $4,200 for Nacha Compliance and Audits plus $5,000 for Legal and Regulatory Counsel.

Fee Drivers

ODFI Network Access Fees sit at 85% of Year 1 revenue, so this line can dwarf fixed legal spend fast. The right estimate depends on operating model, funds flow, states served, and whether customer funds are held. One clean line: the more regulated the flow, the heavier the fee load.

Model funds flow first

Map each state served

Check customer-funds handling

Estimate Inputs

Here’s the quick math: start with the $9,200 monthly fixed base, then add ODFI access fees using 85% of Year 1 revenue. If you change banking flow, add states, or hold customer funds, reprice the legal and sponsor bank work before launch. Small changes here can change the whole budget.

Use year-one revenue forecast

Set months of coverage

Request sponsor bank quotes

Launch Risk

If onboarding takes longer than planned, these costs keep running while revenue is still thin. That makes sponsor bank diligence, audit planning, and compliance policy work a launch gate, not a back-office task. Budget it early, because the fee stack changes with every decision on flow, footprint, and custody.

Risk, Fraud, KYC, AML, and Security Startup Expense

Launch-Critical Controls

Risk controls are part of launch, not a later add-on. This spend covers business verification, identity checks, transaction monitoring, return-rate controls, Office of Foreign Assets Control screening, fraud tools, audit logs, security reviews, and incident response readiness. If these are weak, ACH processing can fail fast on fraud, returns, or bank review.

Cost Build

Budget $45,000 for Security Hardware and Firewalls, then add Fraud Monitoring and Security Services at 40% of Year 1 revenue plus $2,800 per month for Cybersecurity Insurance. Here’s the quick math: insurance is $33,600 a year, before any fraud-loss reserves or audit work.

Control Spend

Keep coverage tight by starting with rules that block bad accounts early and tune alerts to your payment mix. Don’t underbuy monitoring to save cash; one missed fraud pattern can cost more than the subscription. Use clear KYC thresholds, daily exception review, and staged vendor quotes so the recurring spend stays tied to real volume.

Return Reserve

Plan around 15,000 returns in Year 1, because return handling drives monitoring load, fraud review, and reserve needs. That volume means you need enough cash and staff time for investigations, alerts, and dispute work. Treat the reserve as part of launch funding, not an optional cushion.

Working Capital, Reserves, Insurance, and Launch Readiness Startup Expense

Cash Floor

Keep working capital separate from build costs. For an ACH payment service, the launch buffer needs to cover operating runway, sponsor bank reserves, and launch spend. The stated minimum cash is $334,000 in Month 12, and Year 1 EBITDA is -$399,000, so cash burn is part of the plan, not an exception.

Reserve Inputs

Reserve needs depend on funds flow, states served, and whether customer funds are held, so there is no universal target. Model sponsor bank reserves, returned-item exposure, and fraud losses off volume and policy terms. Use the launch cash floor plus expected downside, then test it against return handling and bank requirements.

Model by funds flow

Separate reserves from CAPEX

Update as volume changes

Launch Spend

Launch-readiness spend covers website launch, sales collateral, and first customer acquisition. Use the monthly inputs: Cybersecurity Insurance at $2,800, Marketing and SEO Content at $8,500, and Sales Commissions and Channel Fees at 30% of Year 1 revenue. That mix can move fast, so tie it to revenue timing and onboarding speed.

Risk Buffer

Don’t underfund controls that sit between launch and loss. Cyber liability, errors and omissions, and fidelity coverage protect against payment failures, bad setup, and internal fraud. For this model, the buffer should sit beside compliance and platform build, because a weak reserve plan can break the launch even when the tech is ready.

Staffing Readiness and Pre-Opening Payroll Startup Expense

Payroll Base

This launch team carries $950,000 in Year 1 payroll: $185,000 CEO, $170,000 CTO, two Lead Fintech Engineers at $155,000 each, $125,000 Compliance and Risk Manager, $95,000 Sales and Account Executive, and $65,000 Customer Support Specialist. That’s the core staffing cost before taxes, benefits, or any contractor spend.

Cost Setup

Classify pre-launch payroll and contractor fees as pre-opening expenses or working capital unless the work is tied to a specific build that can be capitalized. Estimate it with headcount, pay rates, launch date, and months of coverage. One line: if the work does not create a clear asset, it is startup burn, not software value.

Use start date and ramp months

Separate capitalizable dev work

Keep launch burn fully funded

Contractor Mix

Use contractors for short, narrow tasks like implementation help or testing when headcount is still fluid. Keep employees for compliance, risk, core engineering, and support, where control and continuity matter. Contractors can trim fixed burn, but they can also slow handoffs and weaken accountability. The clean rule: outsource the spikes, hire the core.

Outsource temporary launch spikes

Employ core control functions

Watch handoff and response risk

Cash Timing

For a payments platform, this payroll is a cash timing issue first. Unless specific development work is capitalized, the $950,000 Year 1 staff plan sits in startup cash needs, not fixed assets. Build runway for the full team before launch, because compliance, risk, engineering, support, and sales all need to be live before volume shows up.

Payment Technology and Processing Platform Startup Expense

Build Scope

The platform build covers ACH file creation and transmission, the API layer, merchant onboarding, ledgering, reconciliation, reporting dashboards, bank connectivity, admin controls, and implementation assets. Base capitalized build is $120,000 for Core Banking API Development, plus $25,000 for Developer Workstations and $15,000 for Networking Infrastructure where needed.

Budget Inputs

Price this cost from scope, not guesswork. Use developer quotes, the number of banking connections, onboarding steps, and reporting depth. Add recurring Cloud Infrastructure Hosting at 35% of Year 1 revenue and Software Subscriptions at $1,200 per month. More depth in ledgering and controls raises both build time and launch spend.

Count bank and API integrations.

Price workstations and network gear.

Model hosting from Year 1 revenue.

Keep It Lean

Trim cost by shipping the core payment flow first, then adding dashboards, admin tools, and reporting in phases. Don’t overbuild reconciliation on day one. That said, don’t cut bank connectivity or ledgering basics. The fastest path is a narrow first release with clean APIs and enough controls to pass onboarding review.

Phase non-core screens later.

Reuse tested components.

Keep the first release narrow.

Launch Timing

Platform depth changes the launch date as much as the budget. A simple ACH workflow is faster to ship than a full ledgered admin system with reconciliation, dashboards, and multi-bank connectivity. So the real decision is scope: every added control or integration pushes more build hours, more testing, and a longer path to first live volume.