Alternative Credit Scoring Startup Costs: $255k+ CAPEX Plan

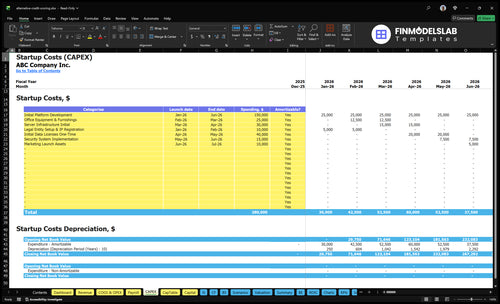

Based on researched planning assumptions, the cost to start an alternative credit scoring service is at least $255,000 in identified CAPEX before first-year operating runway The largest identified CAPEX items are $150,000 for initial platform development, $40,000 for initial data licenses, $30,000 for server infrastructure, $25,000 for equipment, and $10,000 for legal entity setup and intellectual property registration The first operating year also carries $560,000 in wages, $100,000 in marketing at a $50 customer acquisition cost, and $8,700 in monthly fixed overhead, so visible funding need before revenue-based costs is about $102 million That excludes revenue-based partner and variable costs: data aggregation at 7%, cloud hosting at 3%, support at 4%, and sales commissions at 3% of revenue in the first year

Calculate Fuding Needs

Startup cost summary

Startup costs cover platform build, data licenses, server setup, office equipment, legal registration, and a separate operating runway reserve.

Highlighted CAPEX$255,000Base planning example

Excluded cash needs$764,400Outside CAPEX total

Funding need$1,019,400CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Initial Platform Development

$150,000

Core scoring platform build

Yes

Initial Data Licenses One-Time

$40,000

Upfront data access and license fees

Yes

Server Infrastructure Initial

$30,000

Compute, storage, and hosting setup

Yes

Office Equipment & Furnishings

$25,000

Startup office setup and furnishings

Yes

Legal Entity Setup & IP Registration

$10,000

Entity formation and intellectual property filing

Yes

Operating Runway Reserve

$764,400

First-year wages, launch marketing, and fixed overhead runway

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only, so you can size the launch build without mixing in run-rate funding needs.

!

Excluded from CAPEX This calculator excludes inventory, payroll runway, deposits, debt service, working capital, monthly cloud usage, marketing, customer acquisition, recurring legal retainer, and other operating expenses. It also leaves out non-capitalized funding needs like support payroll and launch burn.

Higher launch scale means more data coverage, compliance work, integrations, and go-to-market spend. Lean, Base, and Full show how the same service can start small or build for enterprise use.

Lean, Base, and Full launch cost comparison

Scenario

Lean LaunchPilot

Base LaunchLender-ready

Full LaunchEnterprise-grade

Launch model

Pilot with a narrow data set, one or two channels, and manual review before broader rollout.

Commercial launch with the core product, active sales, and a full first-year team in the model.

Enterprise-ready launch with deeper validation, more integrations, and stronger documentation for larger lenders.

Typical setup

Use limited rent and utility data, one basic score product, and light compliance checks.

The model includes $280,000 of identified CAPEX, $560,000 of Year 1 payroll, $100,000 of marketing, and $8,700 of monthly fixed overhead.

Add broader data coverage, more lender connections, stronger security controls, and deeper proof packs.

Cost drivers

Small data feeds

manual onboarding

basic hosting

light sales spend

Data licenses

$560k first-year payroll

$100k marketing

$8.7k monthly overhead

Expanded integrations

security hardening

validation docs

higher payroll

higher marketing

Planning rangeCAPEX only

$150,000 - $400,000Pilot budget

$950,000 - $1,150,000Core build

$1,250,000 - $1,900,000Enterprise build

Best fit

Best for founders testing fit with a small lender or tenant pipeline before scaling.

Best for a team ready to sell to lenders and carry the modeled setup through Year 1.

Best for teams targeting larger lender contracts and a wider roll-out footprint.

!

Planning note: These ranges are researched planning assumptions from the model, not exact quotes or bids.

What are the biggest startup costs for an alternative credit scoring service?

The biggest startup costs for an Alternative Credit Scoring Service are engineering, data access, compliance, model validation, and security, not office space. Here’s the quick math: $150,000 for initial platform development, $560,000 in first-year wages, and $40,000 in initial data licenses, plus data aggregation partner fees at 70% of first-year revenue. Legal and compliance cost $1,500 per month, security software starts at $700 per month, and office rent at $3,500 per month is secondary.

Main cost drivers

$150,000 platform build.

$560,000 first-year wages.

$40,000 data licenses upfront.

70% of first-year revenue to partners.

Secondary operating costs

$1,500 monthly legal retainer.

$700 monthly security software.

$3,500 monthly office rent.

Compliance and validation stay ongoing.

How should a funding plan for an alternative credit scoring startup connect to the financial model?

The funding plan for the Alternative Credit Scoring Service should track the model in two parts: $255,000+ for build CAPEX, then enough cash for Year 1 runway. Here’s the quick math: $560,000 wages + $100,000 marketing + $8,700 monthly fixed costs equals $764,400 for the first year, so the total funding need starts around $1,019,400. Keep release points tied to software build, compliance gates, hiring, $50 CAC, 30% visitor-to-free-trial conversion, 200% trial-to-paid conversion, and the revenue mix of $9 basic, $29 premium, $49 one-time fee, plus $5 B2B report access.

Build funding first

$255,000+ covers build CAPEX.

Link spend to compliance gates.

Hire only before launch dates.

Pause if CAC rises above $50.

Runway and revenue

First-year runway needs $764,400.

Model 30% trial conversion.

Use $9, $29, and $49 pricing.

Add $5 B2B report fees.

What hidden costs of starting an alternative credit scoring service should founders plan for?

Founders of an Alternative Credit Scoring Service should plan for more than the $255,000 CAPEX anchor, because hidden operating costs keep hitting every month. If you want the revenue side too, see How Much Does The Owner Make From The Alternative Credit Scoring Service? The recurring load includes $1,500 for legal review, $1,000 for accounting and audit, $400 for insurance, $700 for base security software, and customer support/onboarding at 40% of first-year revenue.

Recurring monthly costs

$1,500 legal review per month

$1,000 accounting and audit per month

$400 insurance per month

$700 security software base per month

Setup and runway costs

Privacy documentation before launch

Adverse action workflow readiness

Data-use agreements and security testing

Vendor minimums, pilot support, payroll runway

Key Takeaways

Compliance setup is core pre-opening work, not optional overhead.

Data costs start at $40,000 and scale with revenue.

Platform build and cloud security need upfront funding.

Model validation and monitoring stay ongoing after launch.

Alternative Credit Scoring Service Core Five Startup Costs

Compliance, Legal, and Regulatory Setup Startup Expense

Legal setup

$10,000 covers entity formation and intellectual property registration in the CAPEX schedule, while $1,500/month funds the legal and compliance retainer. For a consumer credit product, this is core pre-opening work, not optional overhead. It should cover policy review, contract drafting, and ongoing compliance advisory before any consumer data flows.

Rules and documents

FCRA means you must handle consumer credit data correctly and support disputes. ECOA means decisions must be fair and explainable, with adverse action notices when needed. GLBA means you must protect financial privacy. Budget also needs privacy policies, data-use agreements, consent records, and adverse action workflows.

Collect opt-in consent records.

Test adverse action notices.

Lock down data-use terms.

Keep it lean

Keep scope tight by using one outside counsel lead and a fixed monthly retainer. Ask for a quote that breaks out formation, IP filings, policy drafting, and workflow review. The key is not cutting the spend; it’s avoiding rework. A weak launch here can force costly fixes after data starts moving.

Bundle filings and policy work.

Reuse templates where fit.

Review before onboarding starts.

Launch gate

Build compliance into the opening checklist, not the cleanup list. If the privacy policy, data-use agreements, consent logs, and adverse action steps are not ready, the product should not open. For a consumer credit business, legal readiness is part of the operating model.

Platform, API, and Software Build Startup Expense

Core Build

The core platform build should start at $150,000. That covers the scoring engine, backend platform, API endpoints, data ingestion, lender portal, admin dashboard, documentation, QA, and implementation work. Treat $30,000 of server infrastructure as separate capitalized infrastructure, so software build and hosting are tracked cleanly from launch.

Run Costs

Here’s the quick math: add $800 per month for core software licenses, $140,000 for the CTO lead engineer salary, and cloud hosting at 30% of first-year revenue. The estimate depends on months of coverage, vendor quotes, and launch revenue. Keep those as operating costs, not build capex.

$800 monthly licenses

$140,000 CTO payroll

30% revenue-based hosting

Scope Control

Don’t let the build creep past the first release. Lock the $150,000 scope to the minimum needed for scoring, data flow, and partner access, then push later enhancements into maintenance. The main mistake is mixing ongoing hosting, licenses, and payroll into the capitalized build, which hides burn and makes launch budgets look too small.

Budget Line

For planning, separate three buckets: $150,000 software development, $30,000 capitalized server infrastructure, and ongoing run-rate items like $800 per month licenses, $140,000 CTO payroll, and cloud hosting at 30% of first-year revenue. That split keeps your launch budget audit-ready and easier to manage.

Model Development, Validation, and Explainability Startup Expense

Model Build Cost

This build is anchored by a $130,000 lead data scientist in Year 1 and a $140,000 CTO lead engineer working together on feature engineering, training data prep, bias testing, and scorecard design. Add validation reports, reason-code logic, and lender review materials. It sits beside platform build and legal spend, not after launch.

What It Covers

This cost covers the work lenders actually need: explainable scoring, validation, and monitoring. The inputs are staff time, test data, review cycles, and documentation hours. Here’s the quick math: one Year 1 data scientist at $130,000 plus one engineer at $140,000 creates a $270,000 core talent base before tools or outside reviews.

Feature engineering

Bias testing

Reason-code logic

How To Control It

Keep scope tight and build the first scorecard around the data you can verify now, not every possible signal. Reuse lender review templates and start monitoring on day one, because model monitoring is an ongoing post-launch cost. The big mistake is chasing fancy models before clear approval, denial, pricing, and adverse action reasons are documented.

Reuse review templates

Limit first-launch features

Budget for ongoing monitoring

Why Explainability Matters

Lenders need clear drivers for approvals, denials, pricing, and adverse action notices, so the model has to be easy to defend in plain English. That means scorecard documentation, validation reports, and lender-ready materials are not extras. They are part of launch readiness, and they reduce rework when compliance asks for proof.

Alternative Data Acquisition and Partnership Startup Expense

Data Buy-In

Initial data licenses are a one-time $40,000 opening cost. This is the base spend for permitted alternative data sources like rent, utilities, and cash-flow records, before any partner minimums, API access, historical datasets, sandbox testing, or match-rate testing. Treat it as core pre-opening work, because the first datasets shape both product quality and lender trust.

What Drives Cost

Budget for setup fees, vendor minimums, partner integration, data quality checks, and testing work. Ongoing aggregation fees are modeled at 70% of first-year revenue, then 50% by Year 5. Here’s the quick math: this cost scales with volume, data type, rights, and the commercial deal, so two partners with the same source can still price very differently.

Keep It Tight

Use the smallest data set that proves match quality first. Start with opt-in rent and utility feeds, then expand only after sandbox testing and data quality checks work cleanly. Push for volume-based terms and clear rights on historical data. The biggest mistake is paying for broad access before you know the match rate.

Test match rates before scaling

Limit unused data rights

Separate one-time from recurring fees

Budget Timing

Plan this as a launch-period cash need, not a back-office line item. If partner fees run at 70% of first-year revenue, they will pressure early cash flow fast, so pair each agreement with a clear usage forecast, integration timeline, and monthly review of match rates, returns, and data quality before adding more sources.

Cloud, Cybersecurity, and Operational Readiness Startup Expense

Launch Security Base

Cloud hosting is priced at 30% of first-year revenue, plus $30,000 for initial server infrastructure and $700 per month for security software. For a consumer financial product, that spend covers encryption, access controls, audit logs, backups, monitoring, and incident response setup before launch.

What It Covers

This cost is the base for secure operations: servers, cloud capacity, data protection tools, and control testing. The monthly fixed layer is $2,100 for security software, accounting and audit services at $1,000, and insurance at $400. Here’s the quick math: add 30% of first-year revenue on top of that.

Encrypt consumer financial data

Limit access by role

Test backups and alerts

How To Control It

Keep the setup tight by buying only the cloud capacity you need, then scaling with usage. Don’t skip penetration testing or incident response planning to save a few thousand dollars; that usually costs more later. The main savings come from avoiding overbuilt infrastructure, not from weakening controls or delaying audit readiness.

Scope cloud to launch volume

Use standard security controls

Reprice after first revenue run

Non-Negotiable Spend

For a business handling sensitive consumer financial data, security is a launch requirement, not a nice-to-have. The budget needs the $30,000 server start, 30% of first-year revenue for cloud, and the ongoing controls that prove the platform is ready for real customer data.