Dance Company Startup Costs: $170K CAPEX And $567K Cash Need

A researched planning estimate for a dance company is $170,000 in one-time CAPEX plus enough startup expense and working capital funding to cover a $567,000 cash need through Month 25 The largest early cash items are paid artistic staff, rehearsal space, production assets, costumes, insurance, website, ticketing, and launch marketing Year 1 assumes 10,000 public performance attendees at $60, 5 corporate events at $8,000, and 500 workshops at $150, yet the model still shows EBITDA of -$132,000 Treat these numbers as researched planning assumptions, not guaranteed vendor quotes

Estimate Startup Costs with Calculator

Startup CAPEX

Estimates one-time capital assets for launch only, so funded CAPEX need equals included CAPEX plus contingency.

!

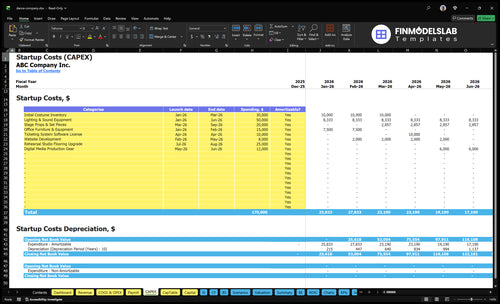

CAPEX only Includes only one-time capital assets: rehearsal studio flooring upgrade, initial costume inventory, lighting and sound equipment, stage props and set pieces, office furniture and equipment, ticketing system software license, website development, and digital media production gear. Excludes monthly rehearsal rent, dancer payroll, rehearsal stipends, insurance premiums, marketing spend, working capital, deposits, debt service, and other operating costs.

Calculate Fuding Needs

Startup Cost Summary

Shows startup assets and excluded cash needs for a dance company, using researched planning ranges.

Highlighted CAPEX$170,000Base planning example

Excluded cash needs$567,000Outside CAPEX total

Funding need$737,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Production Equipment

$62,000

Show production gear and media tools

Yes

Initial Costume Inventory

$30,000

Opening costumes and replacements

Yes

Stage Build and Flooring

$45,000

Props, set pieces, and rehearsal floor work

Yes

Digital Sales Setup

$18,000

Website and ticketing system setup

Yes

Office Setup

$15,000

Furniture and admin equipment

Yes

Operating Cash Reserve Through Month 25

$567,000

Payroll, overhead, and losses before breakeven

No

Does the CAPEX tab show opening cash needs?

This CAPEX tab in the Dance Company Financial Model Template shows startup costs, launch timing, and depreciation planning. Open it to test runway before cash runs short.

Key screenshot highlights

Startup expenses listed

Cash need: $567,000

Year 1 EBITDA: -$132,000

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Scenario size matters here because cast size, rehearsal space, and production gear drive most startup cash. Lean trims payroll and capital spending; Full pushes up working capital and runway needs.

Compare Lean, Base, and Full launch costs across three operating scales.

Scenario

Lean LaunchBest for pilot season

Base LaunchProfessional local launch

Full LaunchProduction-heavy launch

Launch model

Run project-based rehearsals with a smaller cast and rented venue equipment.

Run the modeled local company with 10,000 public performance attendees and steady workshop volume.

Build a larger leased rehearsal setup with more dancers, more productions, and heavier promotion.

Typical setup

Use short runs, limited production assets, and a lighter admin team.

Use the provided plan with $170,000 CAPEX, $12,050 monthly fixed overhead, $521,500 Year 1 payroll, and Month 25 breakeven.

Use more production assets, a bigger cast, and more cash to cover a longer build phase.

Cost drivers

Rented equipment

smaller cast

limited capital spend

light marketing

Owned production gear

full payroll

rehearsal rent

marketing

working capital

Leased rehearsal space

bigger cast

more productions

higher asset spend

larger ad budget

Planning rangeCAPEX only

$250,000 - $400,000Lower cash need

$550,000 - $700,000Core plan

$850,000 - $1,200,000Higher funding

Best fit

Best for founders testing demand before committing to a larger production build.

Best for teams ready to launch a full local operation with a defined show calendar.

Best for a company aiming for multiple shows, wider reach, and a deeper cash buffer.

!

Planning note: Scenario ranges are researched planning assumptions from the model, not vendor quotes. Use them to compare launch scale, then update with booked space, payroll, and production costs.

What is the biggest startup cost for a dance company?

For Dance Company, the biggest startup cost depends on scale, but early cash pressure usually lands on payroll, then rehearsal space and production assets. Year 1 payroll is $521,500, fixed overhead is $12,050 a month, and CAPEX adds another $125,000 for lighting, sound, costumes, flooring, props, and set pieces. Venue strategy and the number of productions change the mix, so there isn’t one universal driver.

Big cash drain

$521,500 Year 1 payroll

$5,000 monthly rehearsal space

$2,500 monthly office rent

$12,050 monthly fixed overhead

Startup build cost

$50,000 lighting and sound

$30,000 costumes

$25,000 flooring

$20,000 props and set pieces

How do you fund a dance company startup budget?

To fund a Dance Company startup, build a stack that covers the $170,000 CAPEX and the early cash gap, because the model still shows -$132,000 EBITDA in Year 1 and -$25,000 in Year 2 before Month 25 breakeven. Here’s the quick math: Year 1 revenue can reach $745,000 from 10,000 attendees at $60, 5 corporate events at $8,000, 500 workshops at $150, plus $15,000 merchandise, $10,000 concessions, and $5,000 program ads. Use grants, donors, sponsorships, ticket sales, workshops, corporate events, and owner or investor capital, and test restrictions plus cash runway before you spend.

Funding sources

Grants can lower cash burn.

Donors can fund start costs.

Sponsorships add non-ticket cash.

Owner or investor capital fills gaps.

Timing and runway

CAPEX hits before revenue.

EBITDA losses need cash cover.

Check grant and donor restrictions early.

Model cash runway to Month 25.

How much money do you need to start a dance company?

You need about $567,000 of launch cash for a Dance Company under the formal plan, not just the $170,000 CAPEX; that bridge covers losses until breakeven in Month 25. Year 1 assumes $745,000 from performances, corporate events, workshops, and extras, but EBITDA (cash operating profit before financing and taxes) is still -$132,000, or -17.7%; track the driver in What Is The Most Important Indicator Of Success For Your Dance Company?.

Formal launch

$170,000 upfront CAPEX

$567,000 cash need through Month 25

$521,500 Year 1 payroll

$8,500/month space, office, insurance

Lean launch

Rent rehearsal blocks only

Buy smaller production assets

Delay full office rent

Bridge losses before Month 25

Key Takeaways

Year 1 payroll totals $521,500 before taxes.

Monthly nonpayroll overhead is $11,550, excluding payroll.

Facility costs split into deposits, setup, and rent.

Reusable assets drive the largest upfront capital spend.

Dance Company Core Five Startup Costs

Rehearsal Space And Facility Setup Startup Expense

Setup split

Separate one-time facility capital spending (CAPEX) from rent. For this dance company, the main CAPEX item is the $25,000 rehearsal studio flooring upgrade, plus lease deposits, basic buildout, mirrors, barres, sound setup, storage, utility setup, accessibility, and code needs. That keeps startup cash clean before monthly overhead starts.

Month one cash

First-month cash needs include the $25,000 flooring upgrade, lease deposits, and the first month of $5,000 rehearsal rent, $2,500 office rent, and $800 utilities. The recurring base is $8,300 a month before payroll, so get separate quotes for setup work, deposits, and move-in timing.

Run rate

Ongoing facility overhead is $8,300 per month, made up of rehearsal space rental, office rent, and utilities. Keep this out of CAPEX and model it as recurring burn. If you can use venue-owned rehearsal space, cash need can drop, but you may give up control over schedule and storage.

Space tradeoff

Venue-owned rehearsal access can cut rent and buildout cost, but it usually limits when you can rehearse and how much you can leave on site. If the company needs stable weekly blocks, compare the lower cash outlay against the risk of losing prime hours, storage, and quick access for tech rehearsals.

Costumes, Wardrobe, And Creative Materials Startup Expense

Launch Wardrobe

$30,000 of initial costume inventory is the core launch spend from Month 1 to Month 3. Treat reusable costumes as capitalized assets, but push show-specific wardrobe, cleaning, repairs, and consumables into production expense. Base the buy on the first slate and on 1 lead dancer FTE plus 4 ensemble dancer FTEs in Year 1.

Cost Drivers

Cost comes from design, fabric, fabrication, alterations, fittings, duplicates, storage racks, repair kits, props tied to wardrobe, and a replacement reserve. Here’s the quick math: units × unit price, then add months of coverage and any quote for cleaning or storage. If the first production uses more looks, the budget rises fast.

Lead dancer sizing and fittings

Ensemble duplicates and backups

Cleaning and repair quotes

Keep It Lean

Buy a small reusable core first, then add show-specific pieces only after the first blocking and sizing pass. Keep repairs and cleaning separate from the asset ledger so the books stay clean. One clean rule: if it can be reused across productions, capitalize it; if it gets used up, expense it.

Watch the Turnover

The biggest budget swing is wardrobe turnover. If fittings change late, duplicates and alterations go up; if the first slate stays stable, one inventory can serve more than one show. Tie the reserve to actual wear, not guesswork, and recheck the order when the cast mix shifts.

Legal, Insurance, Licensing, And Launch Admin Startup Expense

Launch admin stack

This budget covers entity formation, dancer and choreographer contracts, liability insurance, workers’ compensation review, music and performance rights, accounting setup, ticketing, donor and sponsor tracking, launch marketing, and sales channels. The one-time setup is $18,000: $10,000 for ticketing software and $8,000 for website development. This is launch control, not optional polish.

Monthly admin burn

Recurring admin costs run $3,250 per month: $1,000 insurance, $1,200 legal and accounting, $750 software, and $300 office supplies and admin. Here’s the quick math: $3,250 × 12 = $39,000 a year. Use months of coverage to size cash need, and keep these costs separate from production spend.

Contracts and coverage

Start with the entity, then lock dancer and choreographer contracts, rights clearances, and insurance. The main risk is paying for rehearsals and tickets before liability, workers’ compensation, and music rights are clean. One simple rule: if a document or policy protects the show, it belongs in launch admin, not in the art budget.

Keep marketing out of capex

Marketing is modeled at 40% of Year 1 revenue, so do not bury it inside startup assets. Treat it as operating spend tied to ticket sales and sponsorship pace. That keeps the launch budget honest: one-time systems at $18,000, plus recurring admin at $3,250 a month, plus marketing as revenue grows.

Production Assets And Equipment Startup Expense

What it covers

This CAPEX, meaning capital spending, covers reusable gear for rehearsals and shows: $50,000 lighting and sound, $20,000 props and set pieces, and $12,000 digital media gear, or about $82,000 total. Price it with unit counts, vendor quotes, shipping, storage, cases, and maintenance. Leave out venue rent and show-night staffing unless you buy and capitalize the equipment.

How to buy smarter

Buy only the gear that must travel or get reused across productions. If venues provide lighting and sound, skip duplicate systems and keep the spend on portable lights, media capture, storage, transport cases, and repair parts. Touring pushes up wear and transport needs, so quote those costs before you lock the budget.

Ask who owns the house lights.

Count productions opening in Year 1.

Confirm whether touring is in scope.

What drives the number

The big drivers are venue equipment, Year 1 show count, and touring. One local production can lean on house gear; a multi-show season or tour needs more owned lighting, sound, cases, and backup parts. Get the quote after you confirm what the venue supplies and how often the gear will move.

Budget mix

Use the $82,000 baseline as a start, then split it by function: lighting and sound first, then sets and props, then digital capture tools. The clean check is simple: if a venue supplies key equipment, shift that spend to reusable items that support more than one show and protect the next production run.

Artistic Payroll And Rehearsal Readiness Startup Expense

Pre-opening pay

Rehearsal compensation belongs in pre-opening expense or working capital, not CAPEX. Year 1 payroll is $521,500 before payroll taxes or benefits. That covers auditions, rehearsal direction, contractor payments, payroll setup, and worker classification review, which all happen before ticket cash starts to come in.

Year 1 payroll

Use the staffing plan to build the budget: Artistic Director $100,000, Executive Director $90,000, Lead Dancer $55,000, 4 Ensemble Dancers at $40,000 each, plus 0.5 Choreographer at $70,000, 0.5 Production Manager at $65,000, 0.5 Marketing Manager at $60,000, and 0.5 Administrative Assistant at $38,000. That totals $521,500.

Split half-time roles cleanly

Budget taxes and benefits separately

Match pay to rehearsal calendar

Control cash burn

The fastest control is timing, not cuts. Keep contractors and half-time roles tied to actual rehearsal weeks, and review worker status before work starts. If payroll is spread evenly, the base run rate is about $43,458 per month, before taxes and benefits. That is the cash load to cover until shows begin paying back.

Delay starts until rehearsal dates lock

Use contractor reviews early

Avoid misclassifying dancers

Budget fit

Put this line in startup cash, beside rehearsal space and launch admin. It is not a fixed asset; it is the cost of getting the company stage-ready, paying people during build-out, and covering the gap before performance revenue starts to arrive. Treat it as cash you must have on hand, not equipment you can depreciate.