Digital Wallet Startup Costs: Plan Beyond $25M In Year 1

The cost to start a Digital Wallet is not a single app-development quote the provided model already shows $250M in first-year launch funding pressure before CAPEX and regulatory reserves Here’s the quick math: $150M in buyer and seller acquisition marketing, $785k in Year 1 payroll, and $2124k in fixed overhead CAPEX, pre-opening legal setup, licensing work, payment partner deposits, customer balances, and transaction float should be modeled separately because the provided CAPEX schedule is incomplete Year 1 acquisition assumptions imply 200,000 buyers at a $5 CAC and 2,000 sellers at a $250 CAC

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets for a digital wallet launch, not ongoing operating burn.

!

Excluded costs This calculator covers capitalized startup assets only. It excludes payroll runway, customer balances, transaction float, debt service, working capital, post-launch marketing, ongoing processing fees, and operating expenses. Use founder-entered CAPEX if your build scope differs, since the model's initial platform figure is not exposed here.

What should you check in the CAPEX tab?

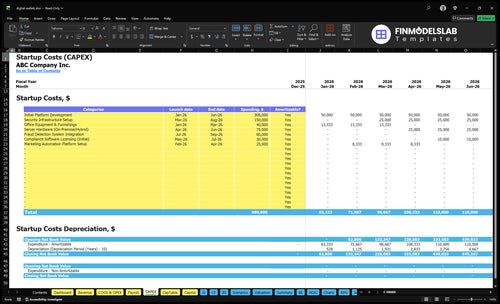

This CAPEX tab in the Digital Wallet Financial Model Template lists expense categories, launch timing, cost amounts, and amortization; validate CAPEX and review assumptions.

Screenshot checks

Cost amounts by line

Transaction volume assumptions

Runway and working capital

Digital Wallet Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

How much money do you need to start a Digital Wallet?

You need about $152.909M for the visible Year 1 Digital Wallet launch burn, and the broader funding pressure can reach $250M before CAPEX and regulatory reserves; track this against What Is The Most Critical Metric To Measure The Success Of Your Digital Wallet Business?. Here’s the quick math: $150M marketing + $785k payroll + $2.124M fixed overhead.

Startup bill

$150M launch marketing budget

$785k first-year payroll

$2.124M fixed overhead

$152.909M visible Year 1 burn

Funding need

$250M total funding pressure

$5 buyer CAC

$250 seller CAC

Add float, deposits, customer-fund obligations

Why do founders need a Digital Wallet financial model?

Founders need a Digital Wallet financial model because it turns a cost guess into a funding plan. With 200,000 buyers at $5 CAC and 2,000 sellers at $250 CAC, the model shows whether commission, subscriptions, fraud, compliance, and cloud costs can cover burn. It also tests the impact of $25 to $100 buyer AOV and $0, $4.99, and $9.99 buyer plans on runway and break-even.

What the model connects

Users: 200,000 buyers, 2,000 sellers

Acquisition: $10M buyer marketing

Acquisition: $500k seller marketing

Fees: commission, subscriptions, fixed order fee

What the model stress-tests

Runway: burn versus cash reserve

Break-even: order volume and AOV

Risk: fraud losses and compliance cost

Sensitivity: CAC and subscription mix

What hidden costs of starting a Digital Wallet get missed?

The hidden cost of a Digital Wallet is not just launch spend; it’s the mix of compliance, fraud, support, and partner cash needs that hit before you scale. If you want the owner view, see How Much Does The Owner Of A Digital Wallet Business Usually Make?; but customer balances, stored-value obligations, and transaction float are not revenue and should not fund operations. Year 1 fraud detection and security operations can run at 20%, while payment processing fees can take 40% and cloud hosting another 30%.

This table shows digital wallet startup CAPEX and the excluded operating reserve needed before breakeven.

Highlighted CAPEX$615,000Base planning example

Excluded cash needs$149,000Outside CAPEX total

Funding need$764,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Initial Platform Development

$300,000

Core software build and app features

Yes

Security Infrastructure Setup

$150,000

Security controls and secure data handling

Yes

Server Hardware (On-Premise/Hybrid)

$75,000

Infrastructure needed for launch capacity

Yes

Fraud Detection System Integration

$60,000

Fraud checks and risk controls

Yes

Compliance Software Licensing (Initial)

$30,000

Initial compliance tooling and setup

Yes

Operating Reserve

$149,000

Payroll, overhead, and launch burn before breakeven

No

Digital Wallet Core Five Startup Costs

Digital Wallet App Development Startup Expense

Build Scope

The software build covers the iOS and Android apps, web admin portal, wallet ledger, transaction logic, APIs, QA, security-by-design, developer environments, testing, and product management. Keep that separate from Year 1 engineering payroll, which anchors at $430k for 2 Senior Software Engineers at $130k each plus a CTO at $170k.

Cost Inputs

The estimate needs a real build quote, because the provided Initial Platform CAPEX is incomplete. Use the scope, number of screens, payment and ledger integrations, test cycles, and vendor rates to fill it in. One-time software build should sit in capitalized startup cost; payroll for the engineering team stays separate unless your accountant capitalizes eligible dev labor.

List every build module.

Get vendor quotes in writing.

Split build and payroll cleanly.

Keep It Tight

Keep cost down by shipping in phases and reusing core APIs, but don’t trim QA or security work. A wallet handles payment data, so bugs and weak controls cost more than they save. Start with the minimum safe release, then add features after the ledger, transaction flow, and test environment are stable.

Budget Check

Before launch, lock the build quote, confirm what is capitalized software, and keep the $430k Year 1 engineering payroll out of the platform CAPEX line. If the final software number is still blank, the startup budget is not finished yet.

Digital Wallet Compliance And Licensing Startup Expense

Licensing Scope

A wallet launch needs legal structure, licensing analysis, AML policies, KYC, sanctions screening, privacy terms, consumer disclosures, regulatory filings, and partner diligence. Cost moves with the custody model, money flow, partner bank setup, and launch states. The recurring floor is $3k/month for legal and compliance plus $12k/month for audit and tax support.

Price It Right

Here’s the quick math: model one-time setup separately from ongoing monitoring. Use quotes for filings, policy drafting, and partner reviews, then add monthly retainers. The Year 2 Compliance Officer salary is $110k, so recurring cost rises fast once oversight moves in-house.

Quote state filing fees.

Map each money flow.

Price partner bank reviews.

Keep It Lean

Start with the narrowest custody model and the fewest launch states that still fit the product. That cuts legal work, filings, and partner diligence. Don’t compress AML or sanctions work; weak controls usually cost more later through rework, bank pushback, or delayed launch.

Limit states at launch.

Reuse policy templates.

Keep bank scope tight.

Ongoing Load

$15k/month in legal, compliance, audit, and tax support is the baseline before headcount. Add the $110k Year 2 Compliance Officer when monitoring, regulatory filings, and vendor oversight move inside the company. What this estimate hides: one-time setup can swing a lot based on custody, bank structure, and state count.

Digital Wallet Security And Fraud Startup Expense

Launch Security

For a wallet that handles payment data, security is a launch cost, not a cleanup cost. Budget for encryption, tokenization, penetration testing, device fingerprinting, fraud rules, account takeover prevention, monitoring, incident response prep, vendor risk review, and security docs before users arrive. Year 1 fraud detection and security ops run at 20% of revenue, with cloud hosting and infrastructure at 30%.

Cost Inputs

Price this in two buckets: one-time launch work and ongoing controls. Launch work covers security design, vendor review, testing, and incident runbooks. Ongoing spend covers monitoring and fraud rules. To estimate it, use vendor quotes, months of coverage, and the revenue share you expect in Year 1 versus Year 5.

One-time setup scope

Monthly monitoring coverage

Quote-based vendor fees

Cost Control

Keep costs down by using managed tools first and custom rules only where fraud justifies them. Standardize security docs, keep one incident response plan, and review vendors before launch. Don’t wait for live fraud to fund controls; this budget belongs before checkout opens. The model still falls to 10% of revenue by Year 5.

Budget Pressure

This line sits beside cloud and infrastructure, so it can’t be treated as a small add-on. In Year 1, 20% of revenue goes to fraud detection and security operations and 30% goes to cloud and infrastructure, so early cash needs are front-loaded. Fund controls first, then scale traffic.

Digital Wallet Payment Integration Startup Expense

Payment Rails Setup

For a digital wallet, this cost covers processor onboarding, bank partner implementation, ACH and card network connections, plus settlement, reconciliation, APIs, sandbox testing, and production certification. Keep one-time setup separate from ongoing fees. Deposits and reserves belong in working capital, not CAPEX.

What To Budget

Model the setup with vendor quotes and launch scope: number of payment rails, partner banks, test cycles, and certification rounds. The cost usually includes integration work, payment ops setup, and reconciliation tools. Here’s the quick math: one-time build plus launch testing, then monthly operating fees after go-live.

Keep Fees Separate

Do not bury transaction fees inside startup spend. The source figures show payment processing fees at 40% of revenue in Year 1, easing to 30% by Year 5. Seller payment processing extra fees are listed at $0, so treat processing as a platform cost unless the model changes.

Protect Cash

Spend on compliance-ready rails before launch, but keep reserves and settlement float out of startup CAPEX. If the wallet holds funds or delays settlement, the real cash need is working capital. That matters because payment timing, not just build cost, can strain early cash.

Digital Wallet Staffing And Operations Startup Expense

Year 1 payroll

For a wallet launch, treat staffing as pre-opening expense or working capital unless you can clearly capitalize software labor. Year 1 payroll is $785k: CEO $180k, CTO $170k, Head of Marketing $120k, two Senior Software Engineers at $130k each, and a Customer Support Specialist at $55k.

What it covers

This team covers engineering, product leadership, customer support setup, and launch management. Year 2 adds a Compliance Officer at $110k and an Account Manager at $80k if risk controls and seller support need more depth. Keep any capitalized build work separate from payroll, because only specific software development labor belongs on CAPEX.

Separate build labor from payroll

Add compliance after launch

Hire support before volume spikes

How to control it

Use staged hiring and outsource non-core work where possible. The bigger drag is fixed overhead at $177k/month, or $2.124m/year, for office, software, legal retainer, insurance, utilities, professional services, and supplies. One line: fixed costs can outrun payroll fast.

Cash burn

Here’s the quick math: $785k payroll plus $177k/month overhead means about $2.909m of Year 1 operating cash before any capitalized build. What this estimate hides: platform development quotes, reserves, and any labor you can legitimately capitalize into software.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Lean, Base, and Full launch costs move with compliance, integrations, and acquisition spend. This table sizes the first funding ask without pretending there is one exact number.

Lean, Base, and Full launch cost bands for a digital wallet.

Scenario

Lean LaunchLow reg, few integrations, small team, tight paid spend

Base LaunchModerate reg, standard integrations, mid-size team, ready CAC

Full LaunchHigher reg, more integrations, larger team, stronger readiness

Launch model

A limited MVP with a narrow feature set and selective rollouts.

Matches the Year 1 operating plan with standard rollout scope and core support.

Expands coverage, security, and risk operations for a wider rollout.

Typical setup

Uses smaller integrations, founder-led compliance coordination, and tighter paid acquisition.

Uses about $1.5M in combined launch marketing, $785k payroll, and $212.4k fixed overhead.

Adds broader state coverage, deeper security work, more integrations, and higher reserve needs.

Cost drivers

MVP build

fewer integrations

founder-led compliance

tighter paid acquisition

Year 1 payroll

combined marketing

core compliance

standard security

moderate integrations

Broader state coverage

more integrations

larger risk team

deeper security

higher reserves

Planning rangeCAPEX only

$500,000 - $1,000,000Lean band

$2,500,000 - $4,000,000Base band

$5,000,000 - $8,500,000Full band

Best fit

Best for founders testing one narrow use case before scaling coverage.

Best for teams launching a full Year 1 plan with normal acquisition targets.

Best for operators planning a wider launch with heavier compliance and support load.

!

Planning note: These ranges are researched planning assumptions, not exact quotes, and they can shift with launch scope, compliance needs, and acquisition mix.

The provided model does not give a complete MVP CAPEX figure, so don’t treat app build as known What it does show is $250M of first-year funding pressure before CAPEX: $150M marketing, $785k payroll, and $2124k fixed overhead A lean MVP should still budget separately for compliance setup, security reviews, payment integrations, and reserves

Plan beyond the launch month because the model starts major costs in Month 1 Fixed overhead alone is $177k per month, and Year 1 payroll is $785k Acquisition spending is also heavy at $10M for buyers and $500k for sellers, so runway should cover product, compliance, support, fraud, and customer acquisition ramp-up

It depends on the wallet design, custody model, payment flow, partner bank structure, and states served A Digital Wallet that holds or moves customer funds can create state-by-state money transmission exposure The model includes a $3k monthly legal and compliance retainer and later adds a Compliance Officer at $110k, but those are planning costs, not legal advice

Tie launch marketing to CAC and user targets, not a flat guess In Year 1, the model budgets $10M for buyer acquisition at $5 CAC, or about 200,000 buyers, plus $500k for seller acquisition at $250 CAC, or about 2,000 sellers If CAC slips, funding needs rise fast

Some setup work may be pre-opening, but the model treats cloud hosting and fraud operations as ongoing percentage costs Year 1 cloud hosting and infrastructure run at 30% of revenue, while fraud detection and security operations run at 20% Budget one-time implementation separately from monthly monitoring, payment processing at 40%, and security reviews

About the author

Brian Fox

Local Business Observer

Brian Fox writes for Financial Models Lab with a focus on simple cash flow planning for early-stage founders turning a service idea into a real business. As a local business observer, he explains business costs in plain language and uses startup budget examples to show how revenue, expenses, and profit fit together. His practical, realistic style helps readers understand the numbers behind starting small and building with clarity.

Choosing a selection results in a full page refresh.