Electronic Component Manufacturing Startup Costs For 460,000 Year 1 Units

Electronic Component Manufacturing

Key Takeaways

Machine quotes exclude facility, testing, tooling, and working capital.

Facility scope should match process sensitivity, not default cleanrooms.

RF transceivers and sensors will push test costs higher.

Raw materials reach $225M before labor, test, and packaging.

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets needed before production starts, not ongoing operating cash.

!

CAPEX only This calculator excludes inventory, payroll runway, deposits, debt service, working capital, sales ramp losses, and recurring operating costs. Use it for pre-launch capital assets only.

Electronic Component Manufacturing Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

How should you fund an electronic component manufacturing startup?

Electronic Component Manufacturing should fund this with a model that a lender and an investor can both read fast: show the CAPEX schedule, startup expense schedule, working capital assumptions, production ramp timing, revenue scenarios, and covenant cushion. Year 1 is $661M from 460,000 units, and Year 5 reaches 2,300,000 units, so the money has to cover launch assets and scale-up capacity, not just day-one output.

Lender checks

Collateral on equipment and assets

Useful life of machinery

Insurance coverage in place

Customer contracts and debt service

Investor checks

Yield ramp from start to scale

Gross margin under pressure

Price declines over time

Working capital growth with production

What hidden costs come with starting an electronic component manufacturing business?

If you’re starting Electronic Component Manufacturing, the big misses are before the first shipment: raw material minimum order quantities, supplier qualification and audits, pilot-run scrap, engineering validation, calibration, reliability testing, sample builds, quality documents, traceability, payroll, insurance, permits, and audit readiness. For the owner view, see How Much Does The Owner Make From An Electronic Component Manufacturing Business? Launch inventory and receivables are working capital, not fixed CAPEX. Source figures show $225M in Year 1 raw materials, $661M in total unit-level production costs, 30% revenue-linked production overhead, and $20,500 a month for rent, admin utilities, and insurance.

Hidden launch costs

MOQ buys tie up cash early.

Supplier audits cost time and money.

Pilot scrap can hit first runs hard.

Validation and testing come before revenue.

Working capital load

Inventory is cash, not fixed CAPEX.

Receivables also lock up cash after shipment.

Payroll, permits, insurance start before sales.

$20,500 monthly fixed costs add up fast.

What drives electronic component manufacturing equipment cost?

For Electronic Component Manufacturing, equipment cost climbs when the line needs more automation, tighter inspection, and more process steps. A Year 1 launch built for 100,000 microcontroller units, 80,000 power management ICs, 150,000 memory chips, 60,000 sensor arrays, and 70,000 RF transceivers gets pricier fast if it needs RF testing, sensor calibration, bonding, encapsulation, packaging, and automated handling. New equipment usually adds warranty and calibration support, while used gear shifts risk to downtime and spare parts.

Core cost drivers

Automation raises tool cost.

Throughput drives line size.

Component type changes process steps.

RF and sensor parts need more testing.

Hidden CAPEX

Yield targets push deeper inspection.

New equipment lowers repair risk.

Used equipment needs spare parts.

Facility readiness adds power, HVAC, ESD, air.

Calculate Fuding Needs

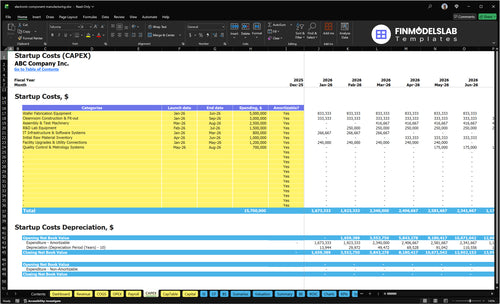

Startup Cost Summary

This table shows the main launch CAPEX for component production plus the non-CAPEX cash buffer needed at startup.

Systems scope for production control and data flow

Yes

Opening Cash Buffer

$224,000

Payroll, rent, insurance, and launch timing before cash turns

No

Electronic Component Manufacturing Core Five Startup Costs

Production Machinery And Automated Lines Startup Expense

Line Equipment Scope

Production machinery drives the first big cash outlay, and the right size depends on the five-product Year 1 mix and 460,000 total units. Plan for forming, assembly, soldering or bonding, encapsulation, handling, packaging, conveyors, feeders, and process automation. Unit cost can run from $8 for memory chips to $25 for RF transceivers before overhead.

Quote The Full Stack

Get separate quotes for new and used equipment, plus installation, commissioning, spare parts, training, warranties, and preventive maintenance. Here’s the quick math: machine price is only one line item. The rest affects launch cash and uptime, especially when five product families need different feeders, fixtures, and automation depth.

Keep The Budget Honest

Do not treat equipment quotes as the full startup budget. Facility work, testing, tooling, inventory, and working capital sit outside the machine purchase, and they can be large. One clean rule: if the line is funded but the site, quality lab, or launch stock is not, the startup is still short on cash.

Buy For Ramp, Not Just Capacity

Use a staged buy plan that matches the first-year build and leaves room for spares, ramp loss, and service. One practical test: if the line cannot support the 460,000-unit mix with acceptable uptime, it is too small or too fragile. That is where avoiding overbuying and underbuying pays off.

Facility Buildout And Leasehold Improvements Startup Expense

Facility Scope

For component manufacturing, start with ESD flooring, ESD benches, controlled production areas, and the basics: power upgrades, HVAC, compressed air, ventilation, fire safety, and utility drops. A full cleanroom is not automatic. Size the buildout to process sensitivity and customer requirements, then place material flow, secure storage, receiving, shipping, and production layout around that scope.

Budget Split

Keep lease deposits and buildout payments separate from recurring rent, utilities, and insurance. The operating assumptions are $15,000 monthly facility rent for admin and R&D, $3,000 monthly general utilities, and $2,500 monthly business insurance, or $20,500 per month before any buildout cash.

Right-Size It

Cut cost by matching the shell to the process, not the other way around. If the products do not need cleanroom-grade control, skip it. Ask for phased quotes on floors, HVAC, power, and compressed air, and avoid overbuying capacity on day one. The costly mistake is paying for a lab-grade shell when stable production space is enough.

Flow First

Lay out receiving, storage, kitting, production, and shipping in a straight path so you do not spend on extra handling, rework, or change orders. Keep sensitive or regulated materials in secure storage and separate admin and R&D from the production zone. One clean flow decision can reduce space waste and labor friction fast.

Testing, Inspection, And Quality Systems Startup Expense

Test Stack

This budget covers electrical testers, automated inspection systems, environmental chambers, calibration tools, measurement equipment, traceability systems, and quality documentation setup. It rises fast when specs are tight, end markets are regulated, or warranty risk is high. With 70,000 RF transceivers and 60,000 sensor arrays in Year 1, test and calibration work is heavier than for simpler parts.

Cost Inputs

Estimate it from quote-by-quote needs: tester count, chamber count, calibration scope, software, installation, and validation. Use unit volume, product mix, and re-test time, then add setup, training, and spare parts. The 0.2% quality assurance overhead is only an operating marker; it does not replace buying the equipment.

Spend Control

Buy to the spec, not to the biggest wish list. Match tools to the five-product mix, start with shared stations where possible, and ask for new and used quotes plus commissioning, warranties, and preventive maintenance. The mistake is underbuying test capacity, then paying in scrap, delays, and customer returns.

Main Drivers

Regulated end markets, RF performance, and sensor calibration push this line item up fastest. If customer specs change often, budget for extra documentation control, more measurement checks, and longer validation runs. One clean rule: the more critical the part, the more upfront test spend you need.

Tooling, Fixtures, Jigs, And Process Engineering Startup Expense

Tooling Scope

Tooling is not a generic add-on. Custom fixtures, test sockets, molds, dies, feeders, and workholding must match each product family, so microcontroller units, power management ICs, memory chips, sensor arrays, and RF transceivers can each need separate setup and validation. Durable tools usually go to CAPEX; short-life prototypes and pilot materials often hit pre-opening expense.

Budget Inputs

Build the estimate from quotes, not a guess. Ask for tool counts, engineering hours before revenue, first article builds, tolerance studies, setup scrap, and repeatability testing for each of the 5 product families. With a 460,000-unit Year 1 mix, small startup losses can add up fast, so keep tooling beside launch inventory and test spend.

Control Waste

Phase tooling by family and avoid overbuilding fixtures before process data is stable. Reuse workholding only where fit and tolerance allow, and lock changes after repeatability tests pass. The common mistake is buying one “universal” setup that still needs rework for each line. That pushes scrap up, slows launch, and hides the real cost of process engineering.

Accounting Split

Under the chosen policy, capitalize durable tooling as CAPEX and book short-life prototypes, pilot runs, and validation scrap as pre-opening expense. That split matters because the spend lands before revenue, and first article work plus repeatability testing happen before steady output. Keep the budget clean so launch cash need is visible.

Initial Materials, Supplier Setup, And Launch Inventory Startup Expense

Launch stock

Most launch materials should sit in working capital, not fixed assets, unless your policy capitalizes specific items. That basket includes conductive materials, substrates, plastics or resins, metals, packaging materials, consumables, supplier audits, qualification builds, and pilot scrap tied to the first runs.

Budget inputs

Build the launch inventory budget from days of inventory on hand, supplier payment terms, import lead times, reorder cycles, yield loss, and customer sample requirements. Here’s the quick math: Year 1 raw materials = $225M, and total unit-level production costs reach $661M after direct labor, wafer fabrication, assembly and test, and packaging.

Count customer sample units separately.

Price pilot scrap into cash need.

Match buffers to lead times.

Control spend

Cut cash burn by locking supplier terms before volume ramps, then tightening reorder points to actual lead times. Don’t use one blanket stock target; different parts need different buffers. The cleanest savings come from lower minimum order quantity (MOQ) exposure, fewer rush imports, and better yield on qualification builds.

Cash timing

What this estimate hides is timing: supplier audits, qualification builds, and pilot scrap can hit cash before revenue starts. If customer sample demand is heavy or import lead times stretch, launch inventory becomes a bigger funding need even when unit economics look fine. Treat it as cash tied up, not just a procurement line.

Compare 3 Startup Cost Scenarios

Scenario table

Lean, base, and full launch plans change this business's startup cash need fast because equipment, cleanroom controls, testing depth, and staffing scale before revenue does.

Lean pilot, base launch, and full-scale facility compare startup spend and operating pressure.

Scenario

Lean LaunchPilot mode

Base LaunchModeled plan

Full LaunchScale ahead

Launch model

Start with fewer products, limited automation, and more outsourced steps to keep the launch tight.

Run the modeled five-product Year 1 plan at about 460,000 units and about $661M revenue.

Build capacity ahead of Year 5 volume, which reaches 2,300,000 units across the five products.

Typical setup

Use smaller launch inventory, basic facility controls, and lower test capacity with a leaner team.

Use the core equipment set, full cleanroom controls, in-house test capacity, and the modeled staffing base.

Add deeper automation, broader facility controls, higher test throughput, larger inventory, and more staff.

Cost drivers

Outsourced steps

smaller inventory

lighter test capacity

basic controls

fewer staff

Wafer equipment

cleanroom fit-out

assembly and test machinery

raw inventory

core staffing

Automation depth

facility controls

high test capacity

larger inventory buffer

added staff

Planning rangeCAPEX only

$8,000,000 - $12,000,000Lower cash need

$15,000,000 - $18,000,000Model-aligned

$20,000,000 - $30,000,000High cash need

Best fit

Fits founders testing demand before they commit to full in-house production.

Fits teams ready to launch the full Year 1 product mix with in-house control.

Fits operators chasing scale early and willing to carry more working capital risk.

!

Planning note: These scenario ranges are researched planning assumptions, not exact quotes or bids.

Carry enough inventory to support supplier lead times, minimum order quantities, pilot scrap, and the first production ramp The model shows $225M of Year 1 raw materials and $661M of total unit-level production costs across 460,000 units The right opening balance depends on payment terms, yield, and how much stock customers require before approval

The provided model uses annual production steps, not a calendar ramp schedule, so do not convert it into exact launch dates It starts at 460,000 units in Year 1, grows to 790,000 in Year 2, and reaches 2,300,000 by Year 5 Your real ramp depends on equipment commissioning, yield learning, customer qualification, and test capacity

Not always, but many electronics customers expect a documented quality system before awarding production work ISO 9001 is the common quality management benchmark, while RoHS compliance may matter when parts enter regulated supply chains Budget time and cost for procedures, traceability, audits, and records, especially with a Year 1 plan of five product families and 460,000 units

Reduce fixed CAPEX first by narrowing the first product set, outsourcing selected wafer fabrication or assembly steps, and buying only the test capacity needed for early customers The model’s Year 1 mix spans five products, $661M of revenue, and 460,000 units A lean launch can validate demand before you fund full automation and larger inventory buffers

Used equipment can make sense when it is supportable, calibratable, and matched to the required tolerances The tradeoff is downtime, missing warranties, spare-part risk, and slower commissioning For a launch tied to $661M Year 1 revenue, 460,000 units, and 50% sales and shipping costs, cheap equipment is expensive if it delays qualified shipments

About the author

Oliver Pierce

Startup Cost Researcher

Oliver Pierce is a startup cost researcher at Financial Models Lab, where he writes practical guides for people planning their first business. He focuses on break-even planning and on comparing business ideas by cost and effort, with a clear, realistic approach to small business planning. His work is aimed at non-finance readers and is written to make business planning easier to understand and use.

Choosing a selection results in a full page refresh.