Eyewear Manufacturing Startup Costs for a 15,000-Unit Year 1 Launch

The cost to start an eyewear manufacturing business is the sum of CAPEX, pre-opening expenses, initial materials, and working capital runway In this plan, the first operating year produces 15,000 units across five eyewear lines and generates $301M in sales, with direct unit inputs ranging from $1350 to $2950 before revenue-based factory costs Listed fixed overhead starts at $227k per month before payroll, while Year 1 channel and logistics costs add 75% of revenue Treat these as researched planning assumptions for early budgeting, not vendor quotes or guaranteed startup costs

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only for an eyewear manufacturing launch.

!

Exclusions This excludes inventory, payroll runway, deposits, debt service, working capital, launch marketing, rent, and other non-CAPEX startup costs.

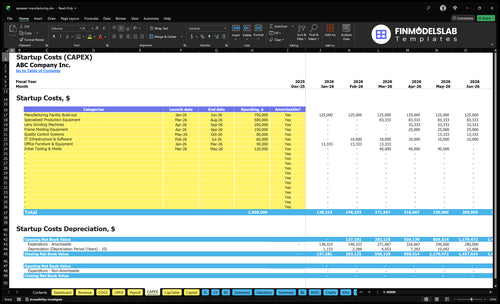

What does the Eyewear Manufacturing model screenshot show?

How much money do I need to start an eyewear manufacturing business?

You should plan funding for Eyewear Manufacturing as vendor-quoted CAPEX, meaning facility and equipment spend, plus pre-opening costs, opening inventory, and runway; equipment alone is not enough. Using the source plan of 15,000 Year 1 units and $301M Year 1 sales, start with $20.25M–$44.25M for direct unit inputs, then add payroll and overhead runway; see What Is The Current Growth Trajectory Of Your Eyewear Manufacturing Business? before locking the raise size.

Funding Stack

CAPEX: requires vendor quotes

Opening inputs: $1,350–$2,950/unit

15,000 units: $20.25M–$44.25M

Add pre-opening and factory costs

Runway Math

Fixed overhead: $227k/month

Visible salaries: $585k/year

Monthly payroll shown: $48.75k

Six-month runway: $1.65M

What hidden costs do eyewear manufacturing startups miss?

If you’re budgeting Eyewear Manufacturing, the hidden costs are the cash drains outside machines and buildout: inventory, lenses, hinges, nose pads, screws, coatings, cleaning supplies, labels, packaging, scrap, rework, testing, certification documents, insurance, payroll before revenue, rent deposits, and slow customer payments. For a quick owner view, see How Much Does The Owner Of Eyewear Manufacturing Business Typically Make? because the model shows 40% Year 1 revenue-based factory costs plus 75% channel and logistics costs, which hit working capital, not CAPEX. Direct unit inputs already run $2,600 for Classic Aviator, $2,950 for Modern Wayfarer, $2,280 for Sport Wrap, $1,920 for Blue Light Blocker, and $1,350 for Kids Durable before factory overhead.

Working cash drains

40% Year 1 factory costs

75% channel and logistics costs

Payroll starts before revenue

Customer payments can lag cash

Unit cost pressure

Classic Aviator: $2,600

Modern Wayfarer: $2,950

Sport Wrap: $2,280

Kids Durable: $1,350

How should I fund an eyewear manufacturing startup?

If you're funding Eyewear Manufacturing, lead with a lender package and an investor package: startup budget, CAPEX schedule, working capital, unit economics, production ramp, cash runway, and use of funds. Show the ramp from 15,000 units in Year 1 at $301M sales to 27,500 in Year 2 and 45,000 in Year 3, because $227k/month of fixed overhead before payroll creates a heavy burn until volume catches up. Lenders will want to separate collateralized equipment from spend that just turns into cash burn.

For lenders

Show CAPEX by asset

Tag collateralized equipment

Map monthly cash burn

State cash runway clearly

For investors

Show unit economics simply

Explain production ramp timing

Use of funds by milestone

Show Year 1 to 3 scale

Calculate Fuding Needs

Startup Cost Summary Table

This table breaks startup outlays into major CAPEX items and one excluded operating cash need for launch planning.

Highlighted CAPEX$1,720,000Base planning example

Excluded cash needs$328,000Outside CAPEX total

Funding need$2,048,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Manufacturing Facility Build-out

$750,000

Space fit-out and production line setup

Yes

Specialized Production Equipment

$500,000

Machine count and automation level

Yes

Lens Grinding Machines

$200,000

Grinding capacity and precision spec

Yes

Frame Molding Equipment

$150,000

Mold complexity and throughput

Yes

Initial Tooling & Molds

$120,000

SKU count and mold revisions

Yes

Operating Reserve

$328,000

Month 8 cash trough and fixed overhead

No

Eyewear Manufacturing Core Five Startup Costs

Manufacturing Equipment Startup Expense

CAPEX Scope

Treat machinery as CAPEX. For 15,000 Year 1 units across five product lines, budget for frame cutting or forming, lens edging, assembly benches, polishing and finishing, inspection tools, production support equipment, maintenance tools, and installation. Scope drops if frame production, lens finishing, coating, or specialty steps are outsourced.

Cost Inputs

Use vendor quotes and install costs to build this line. Keep machinery separate from raw materials, direct labor, rent, and working capital. Here’s the quick math: size the line for output, then add enough capacity for changeovers and daily uptime. That keeps the equipment budget tied to real throughput, not just average unit counts.

Cost Control

Keep the machine set lean and outsource the steps that do not need to sit in-house yet. Tie annual upkeep to the model’s 0.5% equipment maintenance allocation, and fund repairs from the equipment budget, not inventory cash. A common mistake is counting tooling or repairs as materials, which distorts payback.

Scope Control

If frame production, lens finishing, coating, or specialty work stays internal, the startup machine list gets bigger fast. If those steps are outsourced, you still need inspection gear and maintenance tools on site, because quality checks do not go away. Keep the equipment plan separate from inventory, labor, rent, and working capital.

Molds, Tooling, And Product Development Startup Expense

Tooling Scope

Molds, dies, and other durable tooling belong in CAPEX. For a 15,000-unit Year 1 plan across five launch lines, you’ll need frame molds, CAD files, prototypes, sample runs, fit testing, and SKU setup for size and color changes. Narrowing the first launch lowers cash tied up before revenue starts.

Cost Inputs

Estimate this cost from number of SKUs, tool count, sample rounds, and revision cycles. The launch mix includes Classic Aviator, Modern Wayfarer, Sport Wrap, Blue Light Blocker, and Kids Durable, so material, size, and colorway differences can multiply setup work fast. One clean line: more variants, more cash before sales.

Count molds and dies by style

Price each prototype and sample run

Add setup for every size and color

Design Labor

Put durable tooling in CAPEX, but treat CAD work, design revisions, prototypes, sample work, and fit testing as pre-opening expense when they happen before first revenue. The listed $120k annual Head of Design role equals about $10k per month, so every extra pre-launch month adds real cash burn. Design speed matters.

Use one revision log

Limit early colorway sprawl

Gate new SKUs by demand

Launch Mix

A narrow launch cuts tooling pressure because one mold can support fewer variants, while a broad SKU plan spreads setup across more parts, more tests, and more inventory. With five lines, the same frame can still need separate fit checks for material and size changes, so launch order should follow the lowest-cost, highest-confidence styles first.

Facility And Buildout Startup Expense

Buildout Scope

Count lease deposits, production layout, electrical upgrades, compressed air, ventilation, dust control, storage, receiving, packing space, and installation as startup cash, not monthly rent. With $15k monthly rent, $25k utilities, and $700 security, operating facility cost is about $40.7k/month before buildout.

Space Needs

Size the site around in-house production scope, equipment power load, inventory volume, and QA layout. The 15,000-unit first-year plan needs room for materials, work-in-process, finished goods, and packaging, so storage and flow matter as much as machine floor space. One bad aisle plan can slow every shift.

Separate raw, WIP, finished goods

Leave packing near shipping

Plan QC near production

Cost Control

Keep buildout lean by quoting each trade separately and tying upgrades to real equipment loads, not guesses. The usual mistake is paying for unused power, overbuilt storage, or a bigger QA area than the first 15,000 units need. Save money without hurting flow or safety.

Price electrical work by load

Stage storage by volume

Push noncore work out

Startup Cash Line

Deposits and buildout should sit in the startup budget as one-time cash needs, while $15k rent, $25k utilities, and $700 security stay in monthly operating expense. That split keeps launch funding clean and shows how much cash is needed before the first unit ships.

Compliance, Testing, And Quality Control Startup Expense

Quality Scope

This planning bucket covers product testing, inspection tools, quality documentation, labeling review, standards review, testing records, and outside guidance for US eyewear. The model sets quality control at 0.08% of revenue, or about $241k in Year 1 on $301M of sales, before adding related support costs.

Budget Build

Here’s the quick math: use revenue × 0.08%, then add $12k per month for professional services and $1k per month for business insurance. Build the estimate around five product lines, since each line adds test scope, label checks, and recordkeeping. Keep this separate from equipment, materials, and payroll.

0.08% of revenue

$12k monthly guidance

$1k monthly insurance

Cost Control

Reduce spend by grouping tests across variants, reusing approved documentation, and locking labels early so you do not pay for avoidable retests. The risk is underfunding QA at launch and again in Year 5, when higher volume means more inspections, records, and follow-up work even if unit cost improves.

Test shared parts together

Freeze labels early

Plan for higher volume

Budget Gate

This is a control cost, not raw materials or machine CAPEX. It protects all five product lines, and it should scale with revenue and batch count. If testing records, labeling checks, or professional reviews slip, rework can turn into delays and scrap, so fund it from day one.

Initial Inventory And Materials Startup Expense

Inventory First

Most of this spend is inventory or working capital, not CAPEX. Buy acetate, metals, lenses, hinges, nose pads, screws, coatings, cleaning supplies, packaging, labels, and inbound freight as unit inputs. For Year 1, direct unit inputs total about $3,647k before revenue-based factory overhead, so cash needs start well before sales do.

Unit Cost Build

Here’s the quick math: source direct unit input costs are $2,600 for Classic Aviator, $2,950 for Modern Wayfarer, $2,280 for Sport Wrap, $1,920 for Blue Light Blocker, and $1,350 for Kids Durable. Estimate this cost as units × unit input cost, then add supplier minimum order quantities and scrap.

Cash Control

MOQ pressure can make cash use bigger than month one output. Buy to the supplier minimum only where you need it, and track scrap by material line. The fastest savings come from tighter order timing, lower colorway counts, and smaller first buys on lenses and coatings. Don’t mix these materials into equipment spend; that hides the real cash burn.

Working Capital Buffer

Keep a separate buffer for materials because inbound freight, packaging, and reorders move with production volume. With five launch styles and no factory overhead inside this line, the real risk is not price alone; it’s cash tied up in stock. If scrap or MOQ runs high, the first production month will not fully explain the cash you need.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Eyewear costs change fast with scale. Lean uses more outsourcing and less equipment, Base fits the Year 1 build, and Full adds machinery, molds, and inventory for higher volume.

Lean, Base, and Full launch models compared by setup and cost intensity.

Scenario

Lean LaunchVendor dependent

Base LaunchBalanced

Full LaunchInventory strain

Launch model

Small-batch production keeps CAPEX low by outsourcing specialty steps.

In-house frame assembly and finishing is sized around the Year 1 plan of 15,000 units.

Broad integrated production adds more molds, more machinery, and higher internal capacity.

Typical setup

Use a tight SKU set and lighter tooling; working capital stays lean, but vendor lead times matter.

Most core steps stay in-house, with manageable SKU complexity and working capital.

Build for larger inventory and broader SKU coverage, with less reliance on vendors.

Cost drivers

Outsourced finishing

fewer molds

lower tooling

smaller inventory

In-house assembly

finishing equipment

moderate inventory

core tooling

More machinery

more molds

larger inventory

higher internal labor

Planning rangeCAPEX only

Lower six figuresLow CAPEX

Mid seven figuresModel-size CAPEX

High seven figuresScale build

Best fit

Fits a cautious start that wants to test demand before adding full in-house capacity.

Fits a founder who wants control on quality and unit economics without building for full scale on day one.

Fits a team aiming for Year 3 volume of 45,000 units or Year 5 volume of 75,000 units.

!

Planning note: Scenario ranges are researched planning assumptions from the model, not exact vendor quotes or fixed bids.