International Payments Startup Costs: $350K Year 1 Marketing And More

You’re planning a regulated money movement business, so the cost to start an international payments business is bigger than an app build This guide covers capital expenditures (CAPEX), pre-opening expenses, working capital, and total funding need for the first operating year, using researched planning assumptions such as $350,000 in Year 1 acquisition marketing, $16,000 in monthly fixed overhead, and compliance costs that are not legal advice or vendor quotes

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only for an international payments launch.

!

Exclusions matter This calculator covers only capitalized startup assets. It excludes payroll runway, monthly software licenses, office rent, deposits, debt service, customer funds, FX liquidity, inventory runway, working capital, legal retainers, and other operating expenses.

Calculate Fuding Needs

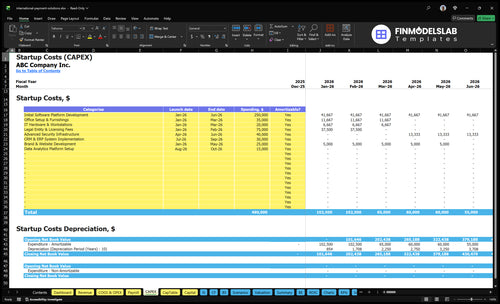

Startup cost summary

This table summarizes the main startup assets and the separate cash reserve needed before breakeven for an international payments business.

Highlighted CAPEX$430,000Base planning example

Excluded cash needs$547,000Outside CAPEX total

Funding need$977,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Initial Software Platform Development

$250,000

Core payment technology build and launch scope

Yes

Legal Entity & Licensing Fees

$75,000

Regulatory setup and licensing work

Yes

Advanced Security Infrastructure

$40,000

Compliance-grade security systems and controls

Yes

Office Setup & Furnishings

$35,000

Launch office buildout and furnishings

Yes

CRM & ERP System Implementation

$30,000

Back-office systems for customer and payment operations

Yes

Opening Working Capital Reserve

$547,000

Funds acquisition marketing, fixed overhead, compliance, and operating cash burn to Month 20 breakeven

No

How does the International Payments model connect startup costs and runway?

Lean keeps launch to one corridor with lighter staffing and licensed tech, Base matches the model's multi-corridor build, and Full adds broader coverage, more banks, and higher reserves.

Lean, Base, and Full launch cost bands for international payments.

Scenario

Lean LaunchSingle corridor

Base LaunchMulti-corridor

Full LaunchBroad coverage

Launch model

Start in one corridor or one state lane, use licensed technology, and keep customer funds ring-fenced outside operating cash.

Launch across several corridors with the model's stronger compliance build and ring-fenced customer funds.

Expand into broader state coverage, add more banking relationships, and hold higher liquidity while keeping customer funds excluded from operating cash.

Typical setup

Keep compliance, support, and sales lean while testing marketing in a small market set.

Use the base staffing plan, Month 1 fixed overhead of $16,000, and $350,000 in Year 1 acquisition marketing.

Carry deeper engineering, more compliance coverage, and a larger reserve for working capital.

Cost drivers

Limited state coverage

one corridor

licensed technology

light staffing

tighter ad tests

Multi-corridor launch

compliance build

$350k Year 1 marketing

$16k monthly overhead

standard staffing

Broad state coverage

deeper engineering

more banking partners

higher reserves

heavier compliance

Planning rangeCAPEX only

$600,000 - $900,000Lower burn

$900,000 - $1,400,000Model fit

$1,400,000 - $2,200,000Reserve heavy

Best fit

Best for founders proving demand before a wider compliance and banking build.

Best for teams that want the planned operating model and balanced growth.

Best for teams with more capital and a clear path to scale the network fast.

!

Planning note: Ranges are researched planning assumptions built from the model inputs, not exact vendor quotes or guaranteed budgets.

How should I build a funding plan for an international payments business?

Build the funding plan around licensing timing, launch month, and the first states you can cover, then size cash against Year 1 volume and spend. For International Payments, use the model with $2 fixed commission per order, the stated 150% variable commission assumption, $250 AOV for individuals, $1,500 for small businesses, and $750 for expatriates, then test CAC at $300 per seller and $50 per buyer before you raise.

Funding inputs

$350,000 Year 1 marketing

$16,000 monthly fixed overhead

Test payroll and reserves

Match cash to launch timing

Runway checks

$192,000 annual overhead

Set cash for state coverage

Fund licensing before launch

Keep liquidity ahead of volume

What hidden costs of starting an international payments business should founders plan for?

Founders of International Payments need to budget for more than setup bills: the real drag is working capital for customer float safeguards, FX prefunding, settlement delays, bank reserves, chargebacks, compliance, audits, cybersecurity checks, and customer support before revenue settles. The economics can bite fast: 60% Year 1 transaction processing fees, 30% currency conversion costs, 50% cloud hosting and data security, plus $16,000 in monthly fixed overhead. If you want the owner-side view too, see How Much Does The Owner Of International Payments Business Make?

Hidden cash needs

Keep customer funds separate from owner capital

Plan for regulated safeguarding obligations

Prefund foreign exchange before settlement

Hold extra cash for bank reserves

Cost drivers to fund

Model chargebacks and payment disputes

Budget for compliance reviews and audits

Expect cybersecurity checks and controls

Cover support before revenue is stable

What does a money transmitter license cost?

For International Payments, a money transmitter license is a state-by-state planning cost, not one national fee. A practical anchor is $4,000 per month for legal and regulatory compliance plus professional support, before state filings, surety bonds, anti-money laundering (AML) policies, and exam prep. Coverage strategy also drives timing, banking access, and launch scope, so this is planning context, not legal advice.

Cost drivers

FinCEN Money Services Business registration

State money transmitter licenses

Surety bonds by state

Legal filings and forms

Launch impact

Compliance program setup

AML policy work

Examination readiness

Coverage strategy shapes timing

Key Takeaways

Compliance setup is launch infrastructure, not optional admin.

Platform build costs run beyond licenses into engineering and security.

Liquidity and settlement need separate prefunding and reserve planning.

Sales and support budgets must fund acquisition and onboarding.

International Payments Core Five Startup Costs

Regulatory Setup And Licensing Startup Expense

License first

Regulatory setup is launch infrastructure, not back-office admin. For an international payments startup, the base load is $4,000 a month for legal and regulatory compliance, plus $1,500 for accounting and $1,000 for insurance. That $6,500 monthly anchor sits behind FinCEN MSB registration, state money transmitter filings, surety bonds, manuals, AML rules, and sanctions screening.

What it covers

This budget covers the filings and controls that let you open: FinCEN Money Services Business registration, state money transmitter license applications, legal filings, compliance manuals, anti-money laundering policies, and sanctions screening procedures. The key input is state scope, because more states mean more applications, more review, and more bond and legal work.

How to manage it

Keep the first launch state narrow, then expand only after the core compliance stack is live. Ask for fixed quotes on filings and monthly retainers, and do not skip manuals or screening rules to save a little cash; that usually gets expensive later. The clean benchmark here is the $6,500 monthly readiness base.

Start with one-state scope.

Use fixed-fee counsel.

Update policies before launch.

Readiness stack

MSB registration, state licenses, bonds, and compliance controls should be in place before customer onboarding starts. If the filing set is incomplete, bank due diligence and payment partner setup slow down too, so the real cost is not just legal spend, it is lost launch time and blocked revenue.

Staffing Readiness And Go-To-Market Startup Expense

Launch Team

For an international payments launch, treat staffing as two buckets: pre-opening coverage and payroll runway. The launch team usually includes a compliance officer, operations, support, treasury or finance help, and contractors for the website and trust content. Year 1 tech and sales anchors already reach $610,000: $180,000 Head of Engineering, 2 senior engineers at $140,000 each, and a $150,000 Head of Sales.

Acquire Users

Launch marketing is separate from payroll. The anchor spend is $150,000 for seller marketing and $200,000 for buyer marketing, or $350,000 total. At $300 seller CAC and $50 buyer CAC, that spend maps to about 500 sellers and 4,000 buyers, before channel mix and conversion losses.

Test seller channels first.

Track CAC by source.

Stop weak campaigns fast.

Control Burn

Keep launch costs from bleeding into fixed burn. Hire only the roles needed for compliance coverage, order handling, and support, then use contractors for website launch and trust-building content. The clean test is simple: if the hire does not cut risk or speed acquisition, delay it. One-line rule: build the team for control, not headcount.

Runway Buckets

Run the budget in three lines: setup, launch, and monthly runway. Setup covers staff needed before go-live; launch covers seller and buyer acquisition tests; runway covers recurring payroll after launch. What this hides: if onboarding or support takes longer than planned, staffing burn rises fast, so buffer the recurring team before you push paid growth.

Payment Technology And Platform Build Startup Expense

Build Scope

A cross-border payments platform is not one app; it’s onboarding, KYC, AML screening, transaction monitoring, FX rate display, payout routing, API integrations, data security, audit logs, and reporting. The budget must split build, implementation fees, and ongoing SaaS, or launch cash will be too low.

Year 1 Tech Spend

Year 1 engineering payroll is $460,000: $180,000 for the Head of Engineering plus 2 × $140,000 senior software engineers. Add $2,500/month in general software licenses, then treat cloud hosting and data security as a separate line item. That is the core platform cost before banking or compliance work.

Count headcount × salary

Buy only needed licenses

Price vendor setup fees

Keep The Build Lean

Start with the smallest safe release. Use SaaS for compliance checks and monitoring where it saves time, and avoid custom-building reporting or audit logs until the money flow works. The fastest way to waste cash is to overbuild before the payment rails, FX display, and payout routing are stable.

Ship core flow first

Reuse approved APIs

Delay nice-to-have analytics

Budget Risk

What this budget hides is time. If onboarding, KYC, and API integration slip, payroll keeps running while launch stalls. So the real test is whether the team can ship risk checks, reporting, and payout routing fast enough to justify the $460,000 engineering base plus recurring licenses.

Banking, Payment Rails, Liquidity, And Settlement Startup Expense

Rails Cost

This line covers bank onboarding, processors, payout networks, correspondent banks, settlement accounts, reserve deposits, and FX prefunding. Treat customer money, reserves, and operating cash as separate buckets. Model 60% Year 1 transaction processing costs, 30% Year 1 FX conversion costs, plus a $2 fixed commission per order and the stated 150% variable commission rule.

Budget Inputs

Estimate it with orders × fee per order, volume × processing %, volume × FX %, plus the cash locked in reserves and prefunding. Use the AOV cases of $250, $750, and $1,500; the $2 fixed fee equals 0.8%, 0.27%, and 0.13% of order value.

Cost Control

Cut cost by funding only the minimum reserve and prefunding needed for the settlement window, and route volume through the fewest compliant rails. Don’t mix customer funds with startup cash. On $250 orders, every extra $2 fee is 0.8%, so small pricing leaks add up fast.

Liquidity Guardrail

Reserve deposits and FX prefunding are tied-up cash, not ordinary operating spend, so keep them off the burn-rate line. Build daily treasury forecasts for balances, settlement timing, and corridor-level funding needs; if settlement lags or volume spikes, a healthy P&L can still run short on cash.

Professional Services, Insurance, And Audit Readiness Startup Expense

Launch Shield

Legal, compliance, and audit prep are launch controls, not optional overhead. For this MSB setup, use the anchors of $4,000 monthly legal and regulatory work, $1,500 monthly accounting, and $1,000 monthly insurance, then add cloud hosting and data security at 50% of the Year 1 line.

What It Covers

Estimate this cost by service quotes, months of coverage, and launch scope. It should cover attorneys, compliance consultants, accountants, cybersecurity reviews, risk assessments, insurance policies, audit preparation, and banking due diligence support. The biggest driver is how many states and bank partners are in scope.

Count months of advisory coverage

Price state filing scope

Add security review quotes

Keep It Tight

Save money by bundling legal and compliance work, reusing policy templates, and narrowing filings to the states you need at launch. Don’t cut bank-readiness work or insurance to move faster; that usually creates delays, rework, and higher total fees later. The savings lever is scope, not quality.

Run-Rate Floor

The known monthly floor is $6,500 before cloud hosting and data security, so budget that line separately. What this estimate hides is state-by-state license work and any extra bank due diligence, which can raise both cash need and launch timing fast.