Invoice Financing Startup Costs: Plan For $35M Funding Capacity

You’re planning a finance business where setup costs are only part of the cash need This guide covers US invoice financing business startup costs, including CAPEX, pre-opening expenses, working capital, and first-year funding capacity, with $8,250 in opening-month fixed overhead, $315,000 in first-year initial payroll, and $40 million in first-year receivable finance assets These are planning assumptions, not vendor quotes, and the capital used to advance invoices is separate from basic setup costs

Estimate Startup Costs with Calculator

Startup Cost Example

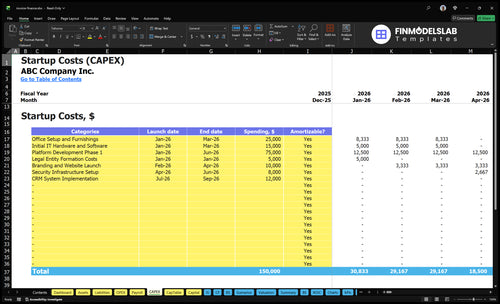

Estimates capitalized startup assets only for an invoice financing business, not operating cash needs.

!

CAPEX limits This tool covers startup assets only. It excludes invoice advance capital, payroll runway, deposits, debt service, working capital, marketing spend, legal retainers, and monthly software or rent unless you capitalize them under your accounting policy. The JSON gives monthly operating costs, not asset purchase quotes.

Calculate Fuding Needs

Startup Cost Summary

This table covers one-time setup costs and excluded funding needs for launching an invoice financing business.

Costs rise as you add staff, compliance, and funding capacity. The three models show how much control and scale you buy at each launch step.

Lean, base, and full launch cost bands

Scenario

Lean LaunchLight launch

Base LaunchModel fit

Full LaunchScale-ready

Launch model

Start with a broker-led model and keep most underwriting manual.

Run as a direct originator with a standard platform and in-house credit controls.

Build a full-service platform with heavier compliance, larger staff, and higher advance capacity.

Typical setup

Use light software, outsourced broker support, and a narrow compliance workflow.

Use the model's $8,250 monthly fixed overhead, $315,000 first-year payroll, and $35M to $40M of funding and receivable capacity.

Add stronger tech, deeper reviews, more marketing, and more capacity for invoice advances.

Cost drivers

Light software

broker support

manual underwriting

narrow compliance

low direct payroll

Core platform

in-house underwriting

sales payroll

compliance retainer

funded receivables

Deeper compliance

stronger platform build

larger payroll

marketing spend

higher advance capacity

Planning rangeCAPEX only

$5M - $15MLowest lift

$35M - $40MCore launch

$50M - $75MHighest lift

Best fit

Best if you want to test demand with less fixed cost and less direct control.

Best if you want a balanced control-and-scale setup with room to grow.

Best if you are set up for faster scale and can carry more fixed cost.

!

Planning note: These scenario ranges are research-based planning assumptions, not exact quotes, and they are not promises of funding access, client volume, or revenue.

How much cash do invoice financing companies need to fund invoices?

Invoice Financing needs cash as working capital, not CAPEX, because the business is advancing invoices and waiting to get paid back. In the first-year model, that means about $15 million for invoice advances, $10 million for trade receivables, $750,000 for working capital lines, $500,000 for factoring facilities, and $250,000 for supply chain finance.

What drives cash need

Invoice size sets exposure.

Advance rate changes cash use.

Debtor mix affects concentration risk.

Collections timing ties up cash longer.

Unit economics and risk

Invoice advances yield 155%.

Factoring facilities yield 160%.

Default reserve is 15%.

Processing fees add 0.5%.

Why build an invoice financing business financial plan before raising capital?

Invoice Financing needs a financial plan before raising capital because the business only works if advance volume, collections lag, debtor concentration, funding cost, bad debt, and operating expenses all fit together. With $40 million in first-year interest-earning receivables and $35 million in liability funding, the model has to absorb a 15% default provision, 0.5% processing fees, $8,250 opening-month fixed overhead, and $315,000 in first-year payroll. Gross yield is assumed at 140% to 160%, while liability costs are listed at 850% to 900%, so runway depends on the spread surviving real collections, not just funded volume.

What the model must prove

Advance up to 90% of invoices.

Match cash to 30, 60, 90-day pay cycles.

Cover 15% default risk.

Hold fees to 0.5%.

Why investors will care

Test the $40 million asset base.

Test the $35 million funding stack.

Fund $8,250 overhead first.

Then size the product template.

How much capital do you need to start an invoice financing business?

To start an Invoice Financing business, separate the operating setup from lending capacity: opening-month fixed overhead is $8,250 before payroll, while first-year payroll is $315,000. The bigger capital need is funding invoices: first-year receivable finance assets total $40 million, backed by $35 million from $25 million bank credit lines and $10 million institutional funding; see What Is The Current Growth Rate Of Invoice Financing Business? for growth context. Don’t blend setup costs with funding capacity, because the founder still needs to model equity cushion, startup CAPEX, legal setup, and timing gaps.

Setup Capital

Budget $8,250 opening-month fixed overhead

Add $315,000 first-year payroll

Model legal setup separately

Include startup CAPEX and equity cushion

Funding Capacity

Plan for $40 million receivable assets

Secure $25 million bank credit lines

Add $10 million institutional funding

Track the $5 million timing gap

Key Takeaways

Legal setup needs a $1,000 monthly retainer.

Tech ops assume $2,000 monthly hosting and licenses.

Underwriting protects $40M of first-year exposure.

Insurance adds $600 monthly and launch readiness checks.

Invoice Financing Core Five Startup Costs

Legal, Regulatory, And Compliance Startup Expense

Launch scope

Before launch, decide whether the company will buy receivables, lend against receivables, broker deals, or do all three. That choice drives the legal stack, because US rules vary by state and product structure. Plan a clean launch checklist and a recurring $1,000/month legal and compliance retainer.

Setup checklist

The setup cost covers entity formation, financing agreements, invoice purchase or advance documents, client onboarding packets, debtor notices, UCC procedure setup, privacy policies, collections language, state regulatory review, and counsel review. Estimate it from the number of states, document versions, and product paths that need review.

Map every state you serve.

Split buy, lend, and broker docs.

Review debtor notices before launch.

Cost control

Keep the spend down by using one core form set and swapping only the state-specific and structure-specific language. Don’t blend receivables purchase terms with lending terms unless counsel signs off. The biggest mistake is drafting once and assuming it works everywhere; that can force rework and delay launch.

Reuse a core document pack.

Change only local clauses.

Get counsel signoff on collections.

Monthly retainer

Use $1,000/month as the recurring base for counsel to handle ongoing compliance, policy updates, debtor language, and state review. Treat one-time formation and document build as separate from the monthly retainer, and refresh counsel whenever the product, states, or collection flow changes.

Technology Platform And Secure Operations Startup Expense

Core Platform

The base stack covers the client portal, application intake, invoice tracking, payment reconciliation, customer relationship management, document storage, e-signature, secure access controls, and hosting. Model the recurring floor at $1,200/month for hosting plus $800/month for software licenses, or $2,000/month before support and any one-time build work.

Estimate Inputs

Use build vs. buy, number of users, portal needs, integrations, audit logs, and data retention to size the budget. Separate one-time implementation or a capitalized software build from monthly subscriptions. The clean model is: setup quote + monthly run rate + security tools, not one blended number.

Count active user seats

Price each integration

Set retention period

Keep It Lean

Trim cost by starting with standard workflows, fewer seats, and only the integrations that change cash speed or control. Put cybersecurity setup and device controls into the CAPEX calculator only when they create asset-like value. The common mistake is burying those launch costs inside monthly software spend.

Delay custom features

Review unused seats

Buy security once

Budget Line

For startup planning, treat $2,000/month as the recurring platform base, then layer in the one-time build quote, security controls, and any capitalized software work. Ask whether the system needs tighter audit logs, longer data retention, or more user roles, because each of those pushes implementation cost up fast.

Underwriting, Credit Data, And Fraud Control Startup Expense

Risk checks

This spend covers business credit reports, debtor verification, bank account validation, know your business checks, invoice authenticity review, customer concentration monitoring, and collections readiness. Know your business means checking that a client is real, authorized, and not obviously high-risk. It’s not optional research; it protects approval quality and loss control on the model’s 15% Year 1 default and bad debt provision.

Cost inputs

Price this by file volume, vendor checks, and analyst time per invoice. Start with the first-year $40 million finance asset base that controls protect, then estimate cost per credit pull, validation, and manual review. The loss model steps from 15% in Year 1 to 11% by Year 5, so tighter screening should lower bad debt as the book matures.

Control spend

Cut cost with automation on bank validation and debtor checks, then reserve human review for exceptions, large tickets, and concentrated buyers. Don’t trim invoice authenticity review or collections readiness to save a few dollars; weak files are expensive later. One clean rule: cheaper checks are good, weaker checks are not.

Exposure base

Judge this budget by the losses it avoids, not by admin spend alone. If the control stack protects $40 million of Year 1 finance assets, the real win is fewer bad approvals, cleaner debtor files, and faster collections when a customer slips. That’s what keeps invoice funding moving without turning small data gaps into cash losses.

Marketing, Broker, And Client Acquisition Startup Expense

Launch Stack

Build the go-to-market setup as one-time launch spend: website, search engine optimization foundations, paid search tests, referral partner materials, broker outreach, sales collateral, onboarding content, and borrower credibility assets. Keep this separate from monthly acquisition cost so you can see what it takes to open the funnel versus keep it running.

Monthly Burn

After launch, the recurring budget should cover ad tests, broker follow-up, partner outreach, and content refresh. The model starts a sales manager at half-year in Year 1, equal to $45,000 of first-year salary from a $90,000 annual role, so staffing ramps with pipeline instead of day one spend.

Test direct sales and brokers.

Track cost by channel.

Pick niches that convert.

Asset Target

Anchor the plan to $40 million in first-year receivable finance assets, but do not turn that into promised approvals or revenue. The real issue is whether direct sales or broker-led sourcing gets there faster, and which industry niches give the cleanest pipeline for staffing, consulting, manufacturing, or wholesale borrowers.

Sourcing Mix

Use broker materials, borrower onboarding content, and credibility assets to cut friction early. If the direct-sales path is slow, shift more spend into partner channels; if brokers bring poor-fit deals, tighten niche filters and keep paid search small until the cost per qualified lead is clear.

Insurance, Cybersecurity, And Operational Readiness Startup Expense

Insurance base

Before launch, bind errors and omissions (E&O), cyber liability, general liability, and fidelity or crime coverage. Use $600/month as the recurring insurance base, and keep payroll runway separate. The big risks here are invoice fraud, employee access, client data loss, and payment redirection, so counsel should confirm state-specific wording.

Launch checklist

Cover secure devices, data protection, staff training, and collections process setup. Estimate it from user count, device quotes, months of coverage, and whether any cybersecurity tools are capitalized. Simple rule: no access without controls.

Lock admin access by role

Verify invoice and payment changes

Train staff on fraud red flags

Control spend

Keep this bucket tight by standardizing workstations, removing extra admin rights, and buying cyber tools only when they qualify as capitalized assets. Don’t mix insurance with payroll. The best savings come from clean setup and a short training script, not from cutting controls that protect cash and customer data.

Recurring assumption

Use $600/month for recurring insurance premiums, which equals $7,200/year. That is the planning base for launch, not a quote. Put one-time secure workstation or cybersecurity build costs in CAPEX only when they are capitalized, and keep the launch readiness checklist separate from ongoing operating cash.