Mortgage Broker Startup Costs: Plan $55K CAPEX Plus $827K Cash

To start a mortgage broker business, the researched plan shows about $55,000 in one-time CAPEX and setup costs, plus a modeled $827,000 minimum cash requirement by Month 2 The first-year plan also includes $25,000 for marketing, $6,400 in monthly fixed overhead before payroll, and $180,000 in annual salary for the owner and first loan officer Total funding should include CAPEX, pre-opening costs, compliance setup, launch marketing, and several months of operating runway The model reaches break-even in Month 5 and payback in 11 months, but those outcomes depend on licensing scope, lead costs, close timing, and staffing pace

Calculate Fuding Needs

Startup cost summary

This table summarizes the main startup assets and excluded cash needs for a mortgage broker using researched model assumptions.

Highlighted CAPEX$55,000Base planning example

Excluded cash needs$827,000Outside CAPEX total

Funding need$882,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

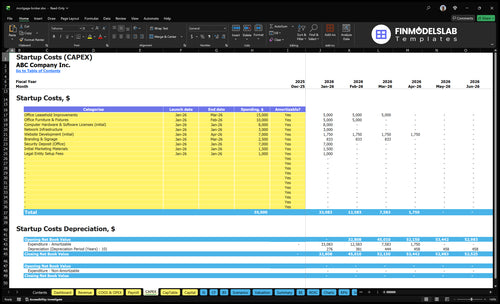

Office leasehold improvements

$15,000

Fit out the office space for launch

Yes

Office furniture and fixtures

$10,000

Desks, seating, and client-area setup

Yes

Technology stack setup

$11,000

Initial hardware, software, and network setup

Yes

Website, branding, and launch marketing

$11,000

Website build plus branding and launch materials

Yes

Office deposit and legal setup

$8,000

Office security deposit and entity setup fees

Yes

Operating reserve

$827,000

Covers the Month 2 cash trough and early fixed overhead

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates one-time capitalized startup assets and setup costs only, not the full cash needed to run the business.

!

Excluded from CAPEX This calculator covers one-time startup assets and setup only. It excludes security deposits, working capital, payroll runway, debt service, monthly subscriptions, monthly marketing, inventory, and other operating cash needs. Month 2 cash pressure is a separate funding issue.

Where do startup costs and CAPEX show up?

This tab in the Mortgage Broker Financial Model Template shows startup costs and CAPEX. Review categories, launch timing, amounts, depreciation, and assumptions.

Key model checks

$55k setup costs

$25k Year 1 marketing

$120k/$60k salary ramp

$827k Month 2 cash

Compare 3 Startup Cost Scenarios

Scenario table

Lean strips out office and staff, Base matches the model, and Full adds retail space, more licensing, support staff, and heavier lead spend. Costs rise with reach and compliance.

Lean, Base, and Full launch cost bands

Scenario

Lean LaunchHome-based

Base LaunchModel match

Full LaunchScale build

Launch model

A home-based launch with the owner handling origination, a tight tech stack, and referral-led lead flow.

This is the modeled launch with a modest office, one loan officer, and a Month 2 cash trough of $827,000.

A broader launch with a small retail office, more licensing, added support staff, and heavier marketing and compliance.

Typical setup

Lower office CAPEX, fewer states, and only the software and compliance tools needed to start.

A modest office with professional software, compliance support, and one loan officer beside the owner.

A small retail office with broader license coverage, more staff, and a larger lead-generation engine.

Cost drivers

Home office

tighter software stack

referral marketing

fewer licenses

no extra staff

$55,000 setup

$25,000 Year 1 marketing

office rent

compliance support

owner plus one loan officer

Retail office

broader licensing

support staff

higher lead gen

heavier compliance

Planning rangeCAPEX only

Below $55,000 setupLowest cash need

$55,000 setupModeled baseline

Above $55,000 setupHighest cash need

Best fit

Best for a solo founder testing demand before adding a staffed office.

Best for founders who want to follow the research-backed plan as written.

Best for operators aiming to build a larger, more visible brokerage from day one.

!

Planning note: These scenario ranges are researched planning assumptions, not exact quotes. Month 5 break-even assumes execution against the model.

How do you fund a mortgage broker startup?

Fund a Mortgage Broker startup with founder cash, partner equity, a working capital line, and seller financing for equipment, because the plan needs $55,000 in one-time CAPEX/setup plus reserve for the modeled $827,000 minimum cash point in Month 2. Tie the raise to Month 5 break-even, 11-month payback, and Year 1 EBITDA of $152,000, so the money covers the ramp, not just the launch. Commission revenue is usually 0.50% to 0.65% of loan amount, so the mortgage broker financial model should test CAC, close rate, salary timing, licensing scope, and marketing budget.

Funding stack

$55,000 CAPEX/setup

Cover the Month 2 cash dip

Use founder and partner equity

Add a working capital line

Model the raise

Target Month 5 break-even

Plan for 11-month payback

Year 2 EBITDA reaches $617,000

Stage hiring to protect cash

How much money do you need to start a mortgage broker business?

You don’t need one universal number to start a Mortgage Broker business; the practical range depends on home-based versus office launch, state licenses, licensed loan originators, and lead strategy. In the modeled plan, use $55,000 for one-time setup and plan for a $827,000 minimum cash need in Month 2; track the core driver in What Is The Most Critical Indicator Of Success For Your Mortgage Broker Business?.

Startup cash drivers

$55,000 setup and launch CAPEX

Home-based costs less than office launch

More states mean more licensing cash

More loan originators increase payroll pressure

Year-one commitments

$180,000 owner plus loan officer salary

$25,000 annual marketing budget

$6,400 monthly fixed overhead before payroll

11% Year 1 variable and direct costs

What are the biggest costs to start a mortgage broker business?

The biggest startup costs for a Mortgage Broker are licensing and compliance, tech, marketing, and the cash to stay open long enough to win loans. Here’s the quick math: the fixed launch stack here is about $2,050/month for CRM and loan origination software, licensing fees, E&O insurance, and accounting/legal help, plus about $40,000 in startup CAPEX for leasehold improvements, furniture, hardware/software, and the website. Add a $25,000 Year 1 marketing budget, with $500 CAC and an 8% paid/referral marketing load on revenue, and the budget gets tight fast.

Core startup costs

$15,000 leasehold improvements

$10,000 furniture

$8,000 hardware and software

$7,000 website build

Monthly run rate

$800 CRM and LOS subscriptions

$200 licensing and regulatory fees

$300 E&O insurance

$750 accounting and legal retainer

What this hides: payroll runway, because a broker still needs cash before closings fund commissions. If lead flow is slow, that $500 CAC can stretch the budget fast, so the first year lives or dies on keeping fixed costs low and closing enough loans to cover the 8% marketing drag.

Budget pressure points

Licensing and surety bonds first

Compliance setup before scaling

Tech stack before lead spend

Payroll runway before expansion

Cost control moves

Keep software to one stack

Delay office upgrades if possible

Use referral channels early

Watch CAC against commissions

Key Takeaways

Licensing costs vary by states, branches, and credentials.

Tech setup needs $11,000 upfront plus $900 monthly.

Office choice can add $32,000 upfront and $4,250 monthly.

Marketing and compliance spend rises with loan mix.

Mortgage Broker Core Five Startup Costs

Licensing, NMLS, And Surety Bond Startup Expense

Licensing stack

NMLS sits at the center of mortgage broker setup. Budget $200 per month for licensing and regulatory fees plus $1,000 for legal entity setup, then add state broker applications, background checks, testing or education, sponsorship, branch licensing where needed, and surety bond costs. The total swings hard with state count, branch count, loan originator count, and whether the owner already holds the needed credentials.

What drives the bill

Here’s the quick math: more states, more branches, and more licensed loan originators mean more filings, more renewals, and more compliance work. One clean one-liner: the cheapest launch is a single-state, owner-led shop with no extra branches. Ask these before you price it: which states, how many loan originators, what bond amount, what continuing education plan, and which renewal month applies.

List all launch states first

Count licensed loan originators

Confirm bond requirement early

Bond and filings

Surety bond requirements protect the state and are part of the licensing cash plan, not an optional extra. Pair the bond quote with state applications, sponsorship, and branch filings so you see the real startup load. If the owner already has required credentials, some upfront work drops; if not, testing, education, and background checks add both time and cost.

Plan the timing

Match your launch budget to the renewal month so cash is ready before fees hit. The smartest version is a calendar: application dates, education deadlines, branch filings, bond renewals, and sponsorship approvals in one place. That keeps the first-year licensing spend visible and stops small compliance delays from turning into a bad opening month.

Office, Equipment, And Secure Operating Setup Startup Expense

Office Choice

A home-based launch can keep overhead low, but it still needs secure files, a locked device plan, and clear borrower communication. A shared office works when you need client meetings or referral partner visits. A small retail office only makes sense when state rules, image, and traffic can justify the extra fixed cost.

Setup Cost

Price the office in three parts: $32,000 upfront for $15,000 leasehold improvements, $10,000 furniture and fixtures, and $7,000 security deposit; then $4,250 a month for $3,500 rent, $500 utilities and internet, and $250 supplies and minor equipment. That excludes computers, phones, and scanners.

Computers and phones

Scanners and printers

Locked file storage

Secure Wi-Fi

Shredding access

Signage and meeting space

Save Smart

The cheapest clean setup is home base plus shared meeting space. It cuts rent and buildout, but it does not cut compliance or data-security needs. Don't pay for empty desks; only move to a leased office when referral meetings or lender visits are frequent enough to cover the fixed monthly burn.

Secure Basics

For a secure operating setup, budget for computers, phones, scanners, printers, locked file storage, secure Wi-Fi, shredding, signage, and a meeting room. Those are the tools that protect borrower data and support a professional client experience, whether the office is at home, shared, or leased.

Mortgage Broker Software And Technology Startup Expense

Launch stack

Your upfront tech bill is mostly setup, not monthly spend. Use $11,000 for launch: $8,000 in computer hardware and software licenses plus $3,000 for network infrastructure. That covers loan origination software (LOS), point-of-sale portal, customer relationship management system (CRM), pricing, credit pulls, e-signature, secure file transfer, cloud storage, email, cybersecurity basics, phones, and backup.

Monthly run-rate

Plan on $900/month in core tech run-rate: $800 for CRM and LOS subscriptions plus $100 for website hosting and maintenance. That excludes add-ons tied to user seats, compliance tools, and lender connections. Here’s the quick math: annualized, that is $10,800 before usage-based fees.

Cost drivers

Costs climb when you add more seats, more integrations, stronger compliance features, and tighter lender connectivity. One loan officer with a lean stack costs far less than a multi-user team with automated credit pulls and pricing tools. Ask vendors for quotes by seat, by integration, and by lender link, so you can compare apples to apples.

Price each seat separately.

Quote every integration.

Check lender connectivity fees.

Keep it lean

Keep setup tight by buying only what you need for day one, then add features after volume proves them. Do not pay for unused seats or duplicate tools. A clean launch budget separates one-time setup from monthly subscriptions, which makes break-even easier to track and prevents tech spend from hiding in overhead.

Website, Launch Marketing, And Lead Generation Startup Expense

Launch Spend

Launch spend starts with $7,000 for the website, then $2,500 for branding and signage, and $1,500 for launch collateral. That $11,000 upfront stack covers local SEO, business profile setup, email campaigns, and CRM workflows. Add the $25,000 Year 1 marketing budget for paid leads and partner outreach, and keep it separate from one-time build costs.

Budget Mix

Do not mix setup with lead buying. Treat the $25,000 Year 1 budget as a live funnel, with 50% variable marketing and lead generation and 30% referral partner fees. Track cost by loan type, because purchase, refinance, and commercial leads do not cost the same. One clean rule: pay for what closes.

Channel Fit

Year 1 customer mix is 70% residential purchase, 20% residential refinance, and 5% commercial property, so channel spend should follow volume. A $500 CAC means a $25,000 budget supports about 50 customers if the mix holds. Purchase usually needs more paid leads; referral partners matter more for refinance and commercial.

Run-Rate

Averaged across the year, the marketing budget is about $2,083 per month, but cash use will swing with launches, referral payouts, and paid lead buys. Keep CRM workflows tight so every lead is tagged by source, loan type, and close date; otherwise CAC math gets muddy fast.

Insurance, Legal, Accounting, And Compliance Startup Expense

Coverage Set

Pre-opening legal and compliance work covers errors and omissions, general liability, cyber insurance, entity formation, an operating agreement, privacy policy, compliance manuals, disclosures, contract review, bookkeeping setup, payroll setup, and outside compliance consulting. Frame these fees as planning costs that lower regulatory and operating risk before the first closing.

Budget Math

Here’s the quick math: monthly professional insurance is $300 and the accounting and legal retainer is $750, so the run-rate is $1,050 a month. Add $1,000 for legal entity setup, then budget 10% of Year 1 revenue for external compliance checks.

Scope Control

Keep the spend tight by limiting review scope to what you need at launch. The biggest cost drivers are multi-state compliance, independent contractor agreements, lender agreements, and written information security procedures. Don’t cut core documents to save a small fee; that usually costs more later.

Key Questions

Before you set the budget, answer this: How many states will you serve, how many loan originators are launching, and which contracts need review first? If you need lender agreements or a written information security program on day one, the legal work gets wider fast.