Owner income$250k

Owner income$250kHotel Acquisition Owner Income: $250K Modeled Salary, Month 33 Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$250k  Net margin257%

Net margin257% Revenue for target pay$46.7M

Revenue for target pay$46.7M Business difficultyHard

Business difficultyHard

A hotel acquisition owner can model $250,000 per year as CEO or managing partner salary in this case, but that’s separate from profit distributions The researched assumptions show EBITDA of -$48416M in Year 1 and -$55133M in Year 2 before turning positive in Year 3 Breakeven is modeled in Month 33, with payback in Month 48 Owner cash flow still depends on debt service, capex reserves, and reinvestment, which are not the same as EBITDA

Owner income$250kNet margin257%Revenue for target pay$46.7MBusiness difficultyHardWant to estimate your hotel owner cash flow?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to test the full acquisition case in Hotel Acquisition?

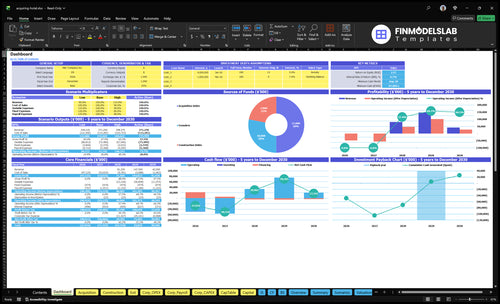

The Hotel Acquisition Financial Model Template dashboard shows revenue, margin, costs, reserves, and owner take-home; open the model.

Owner-income model highlights

- Tabs: assumptions, timing, budgets

- Ops: revenue, costs, payroll

- Returns: EBITDA, cash, owner flow

- Cash floor: -$87,884, Month 32

- Milestones: breakeven 33, payback 48

- IRR / ROE: 001%, 257%

What hotel revenue is needed to make a target owner income?

If you want a target owner income from Hotel Acquisition, don’t start with gross revenue; start with the cash needed after costs. The quick rule is: required revenue = target owner pay plus $39,500 monthly fixed overhead, $690,000 to $940,000 annual payroll, debt service, reserves, and reinvestment, then divide by the hotel’s NOI margin (net operating income margin). Use room count, occupancy, ADR (average daily rate), and ancillary revenue to test if the property can actually support that number.

Revenue formula

- Gross revenue is not take-home pay.

- Add fixed, payroll, and debt costs.

- Use NOI margin to back into revenue.

- Test against target owner income.

Revenue drivers

- Use room count as the base.

- Check occupancy and ADR together.

- Include ancillary revenue where it exists.

- Watch variable costs cited at 330% to 270% of revenue.

How does single hotel owner income compare with hotel portfolio income?

A single hotel owner-operator usually earns through salary plus property cash flow, while a Hotel Acquisition portfolio owner shifts more toward asset management income and distributions across multiple assets. Here’s the quick math: buying 6 owned properties in the first 21 months at $890M in purchase costs means about $148.3M per property, but that scale does not make income automatic.

Single owner income

- Salary plus property cash flow

- One asset, one P&L

- Fewer layers to manage

- Lower overhead than a portfolio

Portfolio owner income

- Asset management income and distributions

- Six properties in 21 months

- Costs rise with payroll and travel

- Legal, accounting, and renovation oversight grow too

Why can hotel operating margin and capex reserves reduce distributions?

For Hotel Acquisition, hotel operating margin can look fine while owner cash flow stays tight because property operating costs, franchise fees, marketing, repairs, utilities, insurance, property taxes, and management fees all cut into NOI (net operating income); see How Much Does It Cost To Open, Start, Launch Your Hotel Acquisition Business? for the acquisition-cost side. With $195M in renovations, a 12-month construction period, and minimum cash hitting -$87,884M in Month 32, capex reserve planning has to come before distributions. The quick rule: if cash is still funding the build, don’t pay it out.

Why margin misleads

- Operating margin can look positive

- NOI still falls after fees

- Costs hit cash before distributions

- Reserve cash for taxes and repairs

What to fund first

- Set aside capex reserves first

- Plan for the 12-month build

- Cover the $195M renovation load

- Protect against negative cash in Month 32

Want to see the six biggest hotel income drivers?

1

Room NightsOccupancy

More room nights lift revenue first, and faster ramp matters because breakeven does not land until Month 33.

2

$/RoomADR/RevPAR

Higher average daily rate and RevPAR raise cash without adding beds, so rate discipline matters once each hotel opens.

3

33%-27%OpEx Control

Variable costs run from 33.0% in Year 1 to 27.0% in Year 5, and fixed overhead stays at $39.5K a month.

4

Month 32Debt Service

Cash bottoms out in Month 32, so debt terms have to survive the trough if you want to reach Month 48 payback.

5

$19.5MCapex Reserves

The renovation budget totals $19.5M, and reserve overruns hit equity cash before the portfolio fully stabilizes.

6

6 HotelsManagement Strategy

Tight management across six owned hotels turns the $89M purchase base into steady cash instead of scattered losses.

Hotel Acquisition Core Six Income Drivers

Occupancy And Room Demand

Occupancy And Room Demand

Occupancy rate is the share of rooms sold each night. It drives room nights sold and room revenue first, so owner income starts only after that. Higher occupancy can lift NOI (net operating income), but it also pushes up staffing, laundry, utilities, repairs, and guest service costs. The key math is simple: available rooms × occupancy rate × days.

What this estimate hides is timing. Demand shifts with market strength, seasonality, and renovation timing. If occupancy stays low during acquisition or construction, cash burn gets worse before Month 33 breakeven. One clean rule: empty rooms don’t pay debt, payroll, or the owner.

Track Demand By Night, Not Just Month

Measure occupancy by weekday, weekend, and season, then compare it with rooms out of service during the 12-month construction period. That tells you whether weak demand is the real issue or the renovation is suppressing sales. Use the same forecast to test how much added occupancy still clears extra labor and housekeeping costs before it reaches owner cash flow.

Track these inputs each week:

- Available rooms and rooms out of service

- Occupancy rate by day and month

- Room nights sold

- Staffing and laundry cost per occupied room

- Guest-service and repair spikes during busy periods

If occupancy rises but per-room costs rise faster, owner draw still lags. So set staffing and supply plans around demand bands, not averages.

1

ADR And RevPAR Pricing

ADR and RevPAR Pricing

ADR means average daily rate, and RevPAR means revenue per available room. RevPAR = ADR × occupancy, so rate growth can lift room revenue without adding keys. But the gain only reaches owner income if the property’s location, renovation quality, guest mix, and independent or branded positioning can hold the higher rate.

A price increase is not the same as more rooms sold. If ADR rises but occupancy slips, cash flow can stall. Higher ADR helps only after franchise fees, marketing costs, operating expenses, debt service, and reserves are paid. In the source model, franchise and marketing fees run 80% of revenue in Year 1 and 70% by Year 5.

Track Rate, Then Protect the Margin

Watch ADR, RevPAR, occupancy, and net cash together. A clean rate lift should show up in room revenue, then survive payroll, utilities, repairs, fees, and reserves. If the property needs heavy discounting to keep occupancy, the rate story is weak even if RevPAR looks fine.

Test rate by segment, not just by date. Compare weekday vs. weekend, renovated vs. older rooms, and guest mix by channel. Use the result to set floor rates, because a small ADR gain that holds across the year usually matters more to owner pay than a short spike that disappears after fees.

- ADR by room type

- RevPAR by month

- Occupancy by demand source

- Net cash after fees

2

Operating Expenses And NOI Margin

Operating Expenses And NOI Margin

Operating expenses decide how much hotel revenue turns into NOI (net operating income). In the provided model, source variable costs, including property operating costs plus franchise fees and marketing, run at 330% of revenue in Year 1 and improve to 270% by Year 5. That leaves very little room for owner cash until costs fall or room revenue rises.

The expense stack includes payroll, utilities, repairs and maintenance, insurance, property taxes, and management costs. Here’s the quick math: NOI = revenue minus operating expenses. Cut costs too hard, though, and guest service can slip, which can hurt demand and ADR (average daily rate). That’s the tradeoff.

Control the Cost Line

Track labor per occupied room, utilities per available room, repairs and maintenance, and fee load every month. Also separate fixed costs from variable costs so you can see what moves with occupancy and what does not. If revenue rises but expense ratios do not fall, owner distributions stay thin.

Test service cuts before you lock them in. For example, lower staffing may save cash, but if reviews, repeat stays, or ADR drop, NOI can shrink anyway. The best lever is disciplined spending that protects the guest experience while bringing the expense ratio down from 330% toward 270%.

- Watch payroll against occupied rooms.

- Review franchise and marketing fees.

- Forecast repairs and property taxes early.

- Protect ADR while cutting waste.

3

Financing And Debt Service

Financing and Debt Service

Debt service is the cash needed to pay principal and interest on the hotel loan. It sits below EBITDA and can block owner take-home even when operations are profitable. To size it, you need loan-to-value, interest rate, amortization term, and refinance timing. The source data does not show debt service yet, so DSCR cannot be calculated.

Here’s the quick math: if EBITDA is positive but loan payments are larger, cash still gets squeezed. That matters in a hotel deal because operating profit is not distributable profit. The real test is whether EBITDA, reserves, and the Month 32 minimum cash of -$87884M can absorb debt before the owner draws money.

Test the loan before you pay yourself

Build the debt schedule separately from hotel operations. Track loan amount, rate, amortization, and refinance date, then compare monthly debt service with EBITDA and reserve burn. Keep owner salary and distributions out of the debt model so you can see true cash pressure.

- Calculate DSCR once debt is known.

- Test cash at Month 32.

- Hold back draws if cash dips.

- Stress rate and refinance timing.

If the model cannot cover debt and still hold the cash floor, the deal may look good on paper but still trap the owner’s income.

4

Capex, Renovations, And Reserves

Capex Reserves

Capex reserve is cash held for property improvements, replacements, and deferred maintenance. In this deal set, renovation budgets total $195M across 6 owned assets, or about $32.5M per hotel. Each construction period lasts 12 months, so the reserve blocks cash while the work is in flight. That lowers near-term distributions, but it protect s asset value and guest experience.

For owner income, the key issue is timing. Reserve funding covers PIP costs, FF&E replacement, repairs, and brand standards, so cash that could have been paid out stays inside the asset. If the reserve is too thin, repairs get deferred, rooms soften, and future NOI drops. If it is sized well, the hotel can support better rates, cleaner reviews, and stronger exit value.

Track the Draw Schedule

Here’s the quick math: $195M spread across 6 assets means the owner needs tight project-by-project tracking, not one pooled guess. Measure planned spend, actual spend, and months of cash tied up on each 12-month build. The reserve should match the renovation scope, not the hope for future profits.

Use a simple control set: budget vs. actual, cash remaining, work completed, and days of disruption. If a project slips, distributions slip too, because reserve dollars stay trapped longer. The clean rule is this: every dollar delayed in capex is a dollar not available for owner pay, so forecast the draw curve before you promise cash.

- Track PIP, FF&E, repairs

- Separate each asset’s reserve

- Update cash needs monthly

- Test owner draw timing

5

Management, Brand, And Asset Strategy

Brand And Management Load

Management fees and franchise fees sit between hotel revenue and owner cash. Good management can lift occupancy, ADR (average daily rate), guest reviews, and cost control, but weak execution burns cash fast. With franchise and marketing fees at 80% of revenue in Year 1 and 70% by Year 5, the margin left for payroll, repairs, debt, and owner pay gets thin.

Here’s the quick math: if revenue is $1.0M, Year 1 fees take $800k, leaving $200k before other hotel costs. By Year 5, fees still take $700k. The real test is whether higher demand survives those charges while the team keeps labor, service, and maintenance tight enough to protect NOI (net operating income).

Track Fee Load And Cash Control

Model this driver with occupancy, ADR, fee %, payroll, and monthly NOI. Watch fee burden as a share of revenue, not just in dollars, because a rate lift can still leave less cash after brand and management charges. If reviews slip or labor rises faster than revenue, owner distributions fall even when gross sales grow.

- Track fee % by month.

- Test ADR against reviews.

- Separate brand and management fees.

- Watch payroll per occupied room.

- Stress cash flow before draws.

6

Compare hotel acquisition owner income scenarios without treating them as promises

Owner income scenarios

Cash is negative until Month 32, so owner income is delayed. Once breakeven hits in Month 33, earnings improve, but payback still stretches to Month 48.

| Scenario | Lean CaseLean case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Owner income stays delayed while the portfolio ramps and cash remains negative. | Owner income follows the modeled path, with breakeven in Month 33 and payback in Month 48. | Owner income improves in a stronger path, but the upside is still editable because no researched upside range was provided. |

| Typical setup | Early acquisitions are still in buildout, fixed payroll and overhead are in place, and there are no owner distributions yet. | The plan follows the source model with $89.0M in purchases, $19.5M in renovations, and EBITDA moving from -$48,416k in Year 1 to $28,244k in Year 5. | The same acquisition base is assumed, with better timing, tighter cost control, and stronger EBITDA conversion after ramp-up. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No distributionsDelayed ramp | Breakeven-led incomeModeled path | Upside not modeledEditable upside |

| Best fit | Use this to stress-test the cash strain before breakeven and any owner draw timing. | Use this as the core planning case for lender talks, cash planning, and owner draw timing. | Use this to test what better execution could do after the base case is already working. |

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Hotel Acquisition Porter's Five Forces Analysis

- Hotel Acquisition BCG Matrix

- Hotel Acquisition Business Model Canvas

- 7 Critical Financial KPIs for Hotel Acquisition Success

- Hotel Acquisition Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Hotel Acquisition Profitability

- How to Budget Corporate Overhead for Hotel Acquisition Operations

- Hotel Acquisition Startup Costs: Plan For $1085M In Property CAPEX

- Hotel Acquisition Financial Model Template in Excel

- How to Start a Hotel Acquisition Company in 90–180 Days

- How to Write a Hotel Acquisition Business Plan in 7 Steps

- Hotel Acquisition Marketing Mix

- Hotel Acquisition Marketing Plan

- Hotel Acquisition Business Proposal

- Hotel Acquisition PESTEL Analysis

- Hotel Acquisition Pitch Deck Example Editable PPTX

- Hotel Acquisition Business SWOT Analysis

- Hotel Acquisition Value Proposition Canvas

Frequently Asked Questions

The model includes a $250,000 annual CEO or managing partner salary, but that is not the same as owner distributions EBITDA is negative in Year 1 and Year 2, then turns positive in Year 3 True take-home depends on debt service, reserves, reinvestment, and whether the owner actually works in the business