Owner income$150k

Owner income$150kHow Much Does An ATS Software Owner Make? $150K Salary Plus Upside

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k  Net margin-57% to 65%

Net margin-57% to 65% Revenue for target pay≈$230k

Revenue for target pay≈$230k Business difficultyHard

Business difficultyHard

You’re building an applicant tracking system (ATS) company, so owner income depends on recurring revenue, payroll, margins, and cash reserves This model separates $860k to $9082M revenue, EBITDA, the $150k CEO salary, distributions, and reinvestment over five years

Owner income$150kNet margin-57% to 65%Revenue for target pay≈$230kBusiness difficultyHardWant to test your ATS owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and cash timing.

Want to see owner income in the Applicant Tracking System Software financial model?

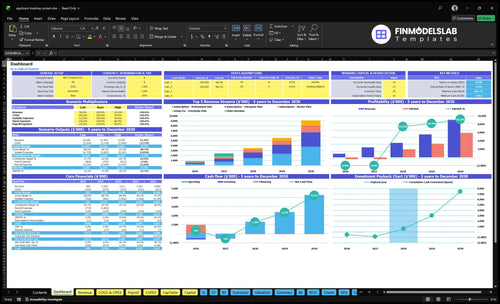

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Applicant Tracking System Software Financial Model Template. It also maps the dashboard, revenue build, plan mix, pricing, transaction revenue, marketing funnel, customer acquisition cost (CAC), cost of goods sold (COGS), variable expenses, payroll, fixed costs, capex, cash flow, breakeven, payback, and scenarios; charts show revenue from $860k to $9082M, EBITDA from -$487k to $5921M, minimum cash at -$224k, and Month 25 breakeven, so the model stays focused on planning, not product promotion.

Owner-income model highlights

- Owner take-home follows profit

- Revenue spans $860k-$9082M

- Break-even hits Month 25

- Scenarios test cash downside

How much revenue does an ATS business need to pay the owner?

For Applicant Tracking System Software, there is no single revenue number that guarantees the owner gets paid. In this model, $860k of Year 1 revenue does not cover the full cost base: $150k CEO salary, $670k payroll, $240k marketing, and $144k fixed overhead, so breakeven lands around Month 25 as the business moves toward Year 3 economics. By Year 3, revenue reaches $3.511M and EBITDA is $1.932M, but the real threshold still depends on customer count, pricing, churn, gross margin, and fixed costs.

Cost base

- $150k CEO salary

- $670k payroll

- $240k marketing

- $144k fixed overhead

What drives break-even

- $860k Year 1 revenue falls short

- Breakeven lands near Month 25

- Year 3 revenue hits $3.511M

- Year 3 EBITDA reaches $1.932M

How much can an ATS founder pay themselves?

An Applicant Tracking System Software founder can pay themselves $150,000 per year if the plan funds it from launch, but that salary is not the same as cash available for owner distributions; see What Are Operating Costs For Applicant Tracking System Software? for the cost base behind that call. With Year 1 EBITDA at -$487,000 and Year 2 EBITDA at -$490,000, early founder pay needs outside cash, not operating profit.

Founder Pay

- Model salary: $150,000/year

- Starts in launch month

- Runs through Year 5

- Needs cash backing early

Cash Reality

- Breakeven comes after Month 25

- Year 5 EBITDA: $5.921M

- Year 5 revenue: $9.082M

- Distributions depend on taxes, debt, reserves

Is an applicant tracking system software business profitable?

Yes—Applicant Tracking System Software can become profitable, but not right away. In this model, EBITDA is negative in Year 1 and Year 2, breaks even in Month 25, and pays back in Month 35. By Year 5, EBITDA reaches $5,921M on $9,082M revenue, so owner income is more reliable only after retention and cash reserves are proven.

Profit timing

- Year 1 EBITDA stays negative.

- Year 2 EBITDA stays negative.

- Breakeven lands at Month 25.

- Payback arrives by Month 35.

Main risks

- Technical maintenance can raise costs.

- Integrations and compliance audits add load.

- Support, sales cycles, and payroll grow fast.

- Competition can press pricing and retention.

Want the six ATS income drivers?

1

$860K-$9.1MRevenue Scale

More ARR is the main take-home lever, with revenue rising from $860K in Year 1 to $9.082M in Year 5 and breakeven in Month 25.

2

4.0%-22.0%Customer Flow

More visitors turning into trials, and more trials turning into paid accounts, lifts customer count without raising spend as fast.

3

78%-83%Gross Margin

With total load falling from 22.0% to 16.7%, each revenue dollar keeps more cash for owners.

4

$99-$699Pricing Power

Higher monthly prices and a larger Enterprise mix raise ARPU, and the setup fee adds extra revenue on bigger deals.

5

$350-$450CAC Efficiency

Lower CAC means the same marketing budget buys more customers, so growth burns less cash.

6

$670K-$1.53MPayroll Build

Payroll climbs fast as headcount grows, which can speed product and sales but also keeps cash tied up before breakeven.

Applicant Tracking System Software Core Six Income Drivers

ARR And Customer Count

ARR and Customer Count

ARR is the recurring subscription base, so more paying employers lift revenue fast. But owner pay only comes after delivery costs, payroll, CAC, reserves, and reinvestment. Here, Year 1 revenue is $860k, so the real question is not just how many customers you sign, but how much each one adds after service load.

ARR = paying customers × average contract value. That sounds simple, but support-heavy accounts can hurt cash even when topline grows. Track active customers, expansions, cancellations, and plan mix every month. If low-fit customers need more help than they pay for, revenue rises while take-home shrinks.

Keep Customer Growth Profitable

Measure active customers, gross additions, cancellations, and expansion revenue together, not alone. A rising customer count only helps if net revenue retention stays strong, meaning upgrades and renewals outrun churn. That is the cleanest way to grow recurring income without bloating support.

Watch plan mix closely. If smaller accounts need more onboarding, admin help, or custom fixes than expected, they can add payroll pressure faster than ARR. The fix is simple: price for service load, set fit rules early, and reject deals that look good on paper but drain the team.

- Track ARR by plan

- Separate new, renewed, expanded

- Flag high-support accounts fast

- Review cancellations monthly

1

Pricing And Contract Size

Pricing Mix Drives Contract Value

Pricing quality matters more than sticker price. The tiers start at $99 Starter, $249 Professional, and $599 Enterprise, then move to $119, $289, and $699 by Year 5. Enterprise also adds $1,500 to $2,500 in one-time fees, so one higher-end logo can create $8,688 to $10,888 in year-one cash before support costs.

That matters for owner pay because contract size changes how fast fixed costs get covered. A bigger Enterprise mix lifts average contract value, but only if discounting stays tight. Starter-heavy revenue is easier to sell, yet each customer still has to pay for payroll, hosting, and sales overhead.

Protect Enterprise Margin

The main risk is selling complex accounts that need heavy onboarding and custom support. If the setup fee does not cover the work, the extra revenue looks good but profit gets thinner. The goal is not just higher price; it is a deal size that pays for the actual service load and still leaves cash for the owner.

Track average contract value (ACV), setup revenue, onboarding hours, support tickets, and discounting by tier. If Enterprise deals need more time than the fee covers, raise the price, narrow the scope, or slow the sale. Simple rule: sell the tier that funds the work, not the tier that only fills the pipeline.

2

Churn And Retention

Retention And Churn

Lower churn protects ARR, cuts replacement sales pressure, and makes owner pay steadier. Because the source data does not give a churn rate, model it as a sensitivity input tied to renewal rate, logo churn, net revenue retention (NRR), and expansion revenue. If those weaken, the CAC drop from $450 to $350 may never reach the owner’s draw.

Here’s the quick math: every lost account has to be replaced before profit feels safe. Higher churn also raises support workload, because more time goes into save calls, re-onboarding, and account cleanup. That pushes cash toward retention work instead of distributions, so the owner gets higher cash consistency only when renewals and expansions hold up.

Measure Retention Weekly

Track renewal rate, logo churn, NRR, expansion revenue, and support hours per account. Then test whether lower churn actually reduces replacement sales enough to lift owner income. If support load rises faster than ARR, margin tightens and cash for distributions shrinks.

- Renewals by month

- Lost logos by plan

- Expansion revenue per cohort

- Support time per customer

- CAC recovered before payout

Keep the forecast simple: if retention slips, assume more sales spend and slower payback. If it improves, more of each subscription dollar can stay in cash and reach the owner.

3

Gross Margin And Support Cost

Gross Margin and Support Load

For an ATS, gross margin is set by hosting, API fees, payment processing, commissions, onboarding, support, integrations, and maintenance. In the model, cloud hosting drops from 80% to 60%, API fees from 40% to 30%, processing from 30% to 27%, and commissions from 70% to 50%. The total delivery and variable load falls from 220% to 167%, so more subscription revenue can reach owner pay.

The risk is enterprise support work that gets buried in payroll. If customer count, active jobs, onboarding time, and integration requests rise faster than pricing, the margin gain disappears in labor. A one-line check: if support is not tracked by account, you can’t see which customers are paying for the extra work they create.

Track Support Cost Per Account

Measure gross margin by plan, then split support into onboarding hours, integration work, and ongoing tickets. Tie each cost to active customers, job postings, and feature use so you can see which accounts pull margin down. If enterprise accounts need custom setup, price that work separately or cap scope before it starts eating take-home income.

- Track support hours by account.

- Separate payroll from delivery cost.

- Price custom integrations up front.

- Watch variable load each month.

Here’s the quick test: if a new customer adds more onboarding and support than recurring fee, gross margin weakens even when revenue grows. The goal is simple: keep variable delivery below the price you collect, so the owner can keep more cash after payroll and still fund product upkeep.

4

Sales Efficiency And CAC

Sales Efficiency and CAC

Owner income improves when each new ATS contract repays acquisition spend fast. Here, marketing rises from $240k to $15M while CAC falls from $450 to $350, so growth can create more recurring revenue with less cash tied up per sale. At $240k and $450 CAC, that’s about 533 customers; at $15M and $350, it’s about 42,857.

The catch is timing. CAC is paid before subscription revenue comes back, so cash gets tight if trials convert slowly or churn shows up early. Visitor-to-free-trial conversion improves from 40% to 60%, and trial-to-paid conversion rises from 150% to 220%, but the owner still needs proven retention before scaling spend. Otherwise, paid growth can lift revenue and still delay profit draw.

Tighten CAC Payback

Track paid spend, CAC, visitor-to-trial rate, trial-to-paid rate, and first renewal rate together. That shows whether the ATS is buying customers who stay long enough to cover the sales cost. Fast payback matters more than cheap clicks because the owner can only pay themselves from cash left after acquisition spend, support, and hosting are covered.

Use the funnel to test where money leaks out. If 40% of visitors start trials but only a small share pay, fix onboarding and sales follow-up before adding budget. If conversion holds near 60% into trial and 220% from trial to paid, scale paid channels in steps and watch retention by cohort so CAC savings turn into real profit.

- Measure CAC by channel.

- Watch trial-to-paid by cohort.

- Test payback before scaling.

- Hold spend if retention slips.

5

Payroll And Product Investment

Payroll Protects the Product

When the applicant tracking system (ATS) adds more engineers, customer success staff, and sales development reps, payroll protects roadmap speed, onboarding, integrations, compliance, and uptime. But it also pulls cash away from owner pay. With wages rising from $670k in Year 1 to $153M in Year 5, plus $12k/month of fixed overhead, the owner’s $150k salary sits behind reinvestment needs, not ahead of them.

Here’s the quick math: engineering grows from 20 to 50 FTE, customer success from 10 to 30 FTE, and sales development from 10 to 40 FTE. That staffing mix can improve service and product quality, but if hiring outruns subscription growth, take-home income gets squeezed even when the platform looks stronger.

Track Payroll Against Payback

Separate the owner’s $150k salary from reinvestment spend for product work, support, and system reliability. Track payroll by function, monthly burn, and how much cash is left after recurring wages and the $12k/month overhead. The key test is whether each new hire protects revenue or just adds cost.

- Track FTE by function.

- Forecast wage run-rate monthly.

- Cap overhead at $12k/month.

- Review pay versus roadmap needs.

- Delay hires until workload proves it.

If onboarding gets slow or uptime slips, customer success and engineering headcount rise again, and owner draws usually move last. That is the real tradeoff: more payroll can support ARR durability, but only if revenue growth and cash collections keep pace.

6

Compare lean, base, and high ATS owner-income scenarios

Owner income scenarios

Income shifts fast here because Year 1 runs at a loss, breakeven lands in Month 25, and Year 5 has room for distributions after reserves and taxes.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | This case keeps owner pay at salary only if the business is funded. | This case supports a steady salary and limited draws after breakeven. | This case adds salary plus distributions as margins widen and cash builds. |

| Typical setup | Year 1 revenue is $860k with -$487k EBITDA, $240k marketing, $450 CAC, and a 4.0% free-trial to 15.0% paid funnel. | By Year 3, revenue reaches $3.511M, EBITDA is $1.932M, CAC is $400, and breakeven has already landed in Month 25. | By Year 5, revenue reaches $9.082M, EBITDA is $5.921M, CAC is $350, and the mix shifts toward 30% Enterprise with stronger conversions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary only if fundedCash tight | Salary plus limited drawBreakeven path | Salary plus distributionsDistribution upside |

| Best fit | Use this to stress test the first operating year before breakeven. | Use this as the main planning case for a funded operator with normal execution. | Use this to test upside when growth, pricing, and retention all hold. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Applicant Tracking System Software Porter's Five Forces Analysis

- Applicant Tracking System Software BCG Matrix

- Applicant Tracking System Software Business Model Canvas

- What Are The 5 KPIs For Applicant Tracking System Software Business?

- Applicant Tracking System Software Business Plan Template in Pre-Written Word

- How Increase Applicant Tracking System Software Profits?

- What Are Operating Costs For Applicant Tracking System Software?

- How Much It Costs To Start An ATS Software Company: $135K+ CAPEX

- Applicant Tracking System Software Financial Model Template in Excel

- How To Start An ATS Software Company: 4-9 Month Launch Roadmap

- How To Write Applicant Tracking System Software Business Plan?

- Applicant Tracking System Software Marketing Mix

- Applicant Tracking System Software Marketing Plan

- Applicant Tracking System Software Business Proposal

- Applicant Tracking System Software PESTEL Analysis

- Applicant Tracking System Software Pitch Deck Example Editable PPTX

- Applicant Tracking System Software Business SWOT Analysis

- Applicant Tracking System Software Value Proposition Canvas

Frequently Asked Questions

The model includes a $150k CEO salary, but early cash may not support extra distributions EBITDA is -$487k in Year 1 and -$490k in Year 2, then reaches $5921M by Year 5 Treat salary, profit, and distributions as separate pools