Owner income$1.1M

Owner income$1.1MHow Much Binder Jetting 3D Printing Owners Make on $296M Year 1 Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.1M  Net margin37%–59%

Net margin37%–59% Revenue for target pay$1.39M per $100k

Revenue for target pay$1.39M per $100k Business difficultyHard

Business difficultyHard

A binder jetting 3D printing service owner can only take home cash left after materials, binder, labor, post-processing, overhead, equipment payments, reserves, and reinvestment In the researched assumptions, Year 1 revenue is $296M, direct costs plus shipping are about $8266k, and contribution is about $213M, or 721% By Year 5, revenue reaches $2513M and contribution reaches about $1786M, or 711% Those figures are planning assumptions, not guaranteed owner income, salary advice, tax advice, or promised distributions

Owner income$1.1MNet margin37%–59%Revenue for target pay$1.39M per $100kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on mix, utilization, payroll, debt, taxes, and reserves. Not guaranteed salary, tax advice, or owner distribution advice.

Want the full owner-income forecast?

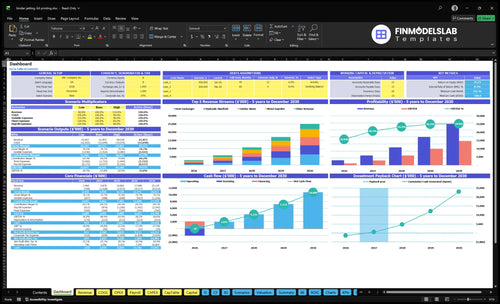

The dashboard shows owner income, revenue, contribution, operating profit, debt service, and reserves; Year 1 to Year 5 revenue grows from $296M to $2,513M, and contribution from $213M to $1,786M. Open the Binder Jetting 3D Printing Service Financial Model Template.

Owner-income model highlights

- Owner pay and reserves

- Revenue to $2,513M

- Utilization, pricing, and cost cases

What binder jetting profit margin should the owner watch?

For a Binder Jetting 3D Printing Service, the owner should watch contribution margin by job type, not just total revenue. If you want the cost side, see What Are Operating Costs For Binder Jetting 3D Printing Service? because scrap, rework, and shipping can cut take-home fast when they are not quoted.

Watch job margins

- Metal impellers: about 733% in Year 1

- Sand casting cores: about 688%

- Turbine blades: about 694%

- Hydraulic manifolds: about 750%

Price and quote risk

- Heat exchangers: about 740%

- Sand jobs start near $180 in Year 1

- Heat exchangers reach $1,500 post-processing

- Quote scrap and rework or margin drops

How does the owner role change income?

If the owner runs quoting, scheduling, and production at a Binder Jetting 3D Printing Service, early cash stays protected, but sales reach is capped. Hiring technicians or adding shifts can raise utilization, but each extra $10,000 a month of payroll or overhead has to be covered by booked demand before owner pay. At the stated 72.1% contribution margin, that’s about $13,900 in added monthly revenue for every new $10,000 of fixed cost.

Owner-led cash control

- Quoting stays in the owner’s hands.

- Scheduling protects cash timing.

- Production decisions stay tight.

- Owner draws wait for booked work.

When to hire

- Hire only after demand is booked.

- More shifts lift utilization.

- Extra payroll needs revenue coverage.

- Machine optimism does not pay bills.

What revenue is needed to pay the owner?

For a Binder Jetting 3D Printing Service, the revenue needed to pay the owner is the owner pay target plus fixed overhead, equipment payments, and reserves, divided by contribution margin. Using the Year 1 model margin, $100k of target owner pay before other overhead needs about $1.387M in revenue, and $20k per month of target pay alone needs about $277k per month. Keep target pay separate from taxable salary, distributions, and benefits so you don’t blur owner pay with operating costs.

Quick math

- Revenue = pay + overhead + reserves

- $100k pay needs about $1.387M

- $20k/month needs about $277k/month

- Higher margin lowers required sales

Pay setup

- Separate pay from distributions

- Separate pay from benefits

- Track equipment payments outside owner pay

- Test pay before hiring grows

Want to see the six biggest income drivers?

1

5.9k-49kUtilization

More machine hours spread fixed labor and facility costs across more parts, which lifts owner take-home fast.

2

$25.1MPipeline

Repeat industrial accounts keep the build queue full, so the plant earns more before overhead bites.

3

$180-$1.5KPricing Mix

Higher-priced turbine, manifold, and exchanger jobs lift revenue per part without adding the same overhead.

4

82%-87%Metal Share

Metal work carries most of the revenue, so a heavier metal mix improves margin more than sand-core volume alone.

5

$874K/yrFixed Load

Lease, software, and salaried staff set the base owner income must clear before cash gets strong.

6

$8-$40/URework Yield

Extra finishing and rework burn powder, labor, and machine time, so small defects cut take-home quickly.

Binder Jetting 3D Printing Service Core Six Income Drivers

Machine Utilization and Build Capacity

Machine Utilization

Utilization is what turns binder jetting equipment from a cost center into billable output. In Year 1, the model assumes 5,900 units and $296M revenue; by Year 5, that grows to 49,000 units and $2,513M. Each 1% of Year 1 revenue utilization is about $296k revenue and about $213k contribution before fixed costs.

Owner pay improves only after labor, material, maintenance, financing, and reserves are covered. So the real test is not printed parts alone; it’s whether the build schedule keeps machines busy enough to clear those recurring costs and leave cash for the owner.

Track build hours, not just parts

Measure nesting density, scheduled build hours, idle days, and on-time release of jobs to the printer. These inputs show whether the machine is earning or sitting. If a week has open build slots, revenue leaks fast because the fixed equipment cost still exists even when the chamber is half full.

Use the same forecast for labor, powder, binder, maintenance, financing, and reserves before you count profit as take-home. The clean rule: more units only help if each extra build lifts contribution faster than it adds rework, changeovers, and downtime.

1

Job Pricing and Industrial Customer Mix

Job Pricing and Customer Mix

Pricing power varies by part type and buyer need. In Year 1, prices run from $180 for sand casting cores to $1,500 for heat exchangers, with turbine blades at $850 and hydraulic manifolds at $1,200. That spread matters because inspection, finishing, and setup time change gross margin. If you underprice prototype jobs, quoting and changeovers eat owner profit fast.

Repeat production work gives steadier cash flow, but prototype work should carry a higher price to cover engineering, quoting, and setup. The owner’s take-home rises when the mix shifts toward jobs that pay for their own handling time, not just machine time. Here’s the quick math: a higher unit price only helps if rework, inspection, and admin time stay contained.

Price to the job, not just the part

Track unit price, setup hours, inspection hours, and repeat order rate by part family. That shows which customers support margin and which ones only fill capacity. Use separate pricing for prototype work, because quoting and engineering time are real costs even before the first unit ships.

Watch the mix between recurring industrial accounts and one-off RFQs. A stable repeat account can protect revenue, but a low-price prototype that needs extra finishing can cut cash for owner pay. Price higher when buyer specs are tighter, lead time is shorter, or acceptance testing is heavier.

- Track RFQ-to-order conversion

- Price by inspection burden

- Separate prototype and repeat rates

- Test margin by part family

2

Metal Versus Sand Material Mix

Metal vs Sand Mix

When the product mix shifts, owner income shifts with it. A sand casting core sells for $180 with $40 unit COGS, while a heat exchanger sells for $1,500 with $240 unit COGS. That means gross margin is about 78% on sand cores and 84% on heat exchangers, but the higher-value metal mix also ties up more cash in powder, binder, storage, and scrap.

Here’s the quick math: owner take-home rises when the mix favors higher gross dollars per unit and lower scrap. The key inputs are unit price, unit COGS, powder and binder cost from $23 per sand core to $140 per heat exchanger, plus reuse, waste, and inventory days. If scrap or slow-moving stock climbs, cash gets stuck before profit reaches the owner.

Track Mix by Gross Margin

Measure each job type separately, not as one blended average. Track mix share, gross margin per unit, powder reuse rate, binder waste, and scrap rate. A mix that looks strong on revenue can still weaken cash if it needs more material on hand or holds finished goods longer.

Test pricing and scheduling against inventory impact. If heat exchanger work uses more powder and binder upfront, keep tighter reorder points and shorter storage windows. If sand cores move faster, use them to support cash conversion. Owner pay improves when the mix keeps contribution margin high and working capital low.

3

Post-Processing Yield and Rework

Post-Processing Yield and Rework

Post-processing can turn a good print into profit or drag it down. Listed costs include $4 for sand-core cleaning and de-powdering, $8 for secondary finishing on metal impellers, $20 for internal channel inspection on hydraulic manifolds, $35 for pressure testing on heat exchangers, and $40 for HIP on turbine blades. At $850 per blade, HIP is 4.7% of sales.

Model first-pass yield separately from print output. If a part needs rework, you burn labor, queue time, and machine slots, so fewer units ship per day and cash comes in slower. On a $1,500 heat exchanger, the $35 test is only 2.3% of revenue, but repeated rework can wipe out that cushion fast.

Track First-Pass Yield

Track first-pass yield by part type, plus rework hours, scrap rate, and outside test fees. Keep sand cores, impellers, blades, manifolds, and heat exchangers separate, because the touch cost is not the same. If one line needs repeat cleaning or testing, quote it as a yield problem, not a one-time hiccup.

- Units shipped by part type

- Rework rate and scrap rate

- Post-process cost per unit

- Queue time added by rework

Use that data to raise prices on messy jobs and protect capacity. When post-processing stays tight, the same machine time produces more billable parts, cash comes in faster, and owner pay is less exposed to surprise labor.

4

Fixed Overhead, Financing, and Reserves

Fixed Overhead and Cash Reserve Load

Accounting profit can look fine while owner cash is still tight. This driver includes 15% maintenance reserves on certain revenue lines, 10% equipment insurance on sand-related revenue, plus utility, inspection, compliance, and software allocations. Rent, admin payroll, loan payments, and taxes are separate inputs, so don’t bury them inside margin.

Here’s the quick math: if monthly cash burden is $50k, you need about $694k revenue before owner pay. That implies an effective contribution margin near 7.21%. One clean rule: fixed cash load, not accounting profit, decides when the owner can draw cash.

Track Cash Burden by Revenue Line

Model reserves and overhead by product mix, not as one blended number. Keep separate inputs for revenue on sand jobs, revenue on other lines, and each fixed cost bucket, then test how the 15% reserve and 10% insurance hit owner cash. If you miss one cost, the payback date moves fast.

- Track reserve by line item.

- Separate rent and payroll.

- Forecast debt and taxes.

- Watch monthly cash burn.

- Set owner pay last.

5

Sales Pipeline and Repeat Industrial Accounts

Repeat Industrial Accounts

Repeat industrial accounts keep the printers busy, cut quoting waste, and protect cash flow. Year 1 needs 5,900 units across five job types, so the pipeline has to refill fast enough to cover setup, finishing, and ship dates. If orders slip, idle machine time and labor still hit profit, and owner pay gets squeezed.

The key inputs are qualified RFQs, quote conversion, average order value, repeat order rate, and days from quote to cash. Year 5 rises to 49,000 units, so the goal is not more leads; it is more billed builds from accounts that reorder, pay on time, and keep volume steady across job types.

Track RFQs and Reorders, Not Lead Count

Measure how many RFQs are qualified, how many turn into quotes, and how many quotes become shipped orders. Tie each account to repeat rate and days from quote to cash. One slow-paying customer can trap cash and still leave capacity idle, so watch concentration and collect terms early.

- Qualified RFQs per month

- Quote-to-order conversion

- Average order value

- Repeat order rate

- Days from quote to cash

Use the pipeline to smooth build slots. If repeat industrial work falls, you lose utilization, waste more quoting time, and need more new business just to hold the same owner draw.

6

Compare low, base, and growth owner-income scenarios

Owner income scenarios

Owner income swings with utilization, pricing, scrap, and fixed plant costs. The same shop can look thin in a slow start and very strong once the five part lines scale.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | The low case assumes weak utilization and softer pricing, so owner income stays tight until volume improves. | The base case assumes the modeled ramp, with Year 1 revenue of $2.96M and EBITDA of $1.09M. | The high case assumes the Year 5 run rate, with revenue at $25.125M and EBITDA at $14.768M. |

| Typical setup | Orders run below plan, scrap stays higher, and delayed collections pressure cash while the fixed team and plant costs stay in place. | The shop runs the five product lines as planned, covers fixed overhead early, and starts to support owner pay after launch. | Volume is strong across all five parts, unit pricing holds, and the plant stays loaded enough to absorb overhead and reinvestment. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Thin early drawDownside planning | Modeled drawBaseline planning | Strong scale drawUpside planning |

| Best fit | Use this to stress-test a slow launch, cash strain, and the point where the shop stops funding itself. | Use this as the core planning case for budget, hiring, and cash timing. | Use this to test what the business can support once capacity, sales, and quality are all working. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Binder Jetting 3D Printing Service Porter's Five Forces Analysis

- Binder Jetting 3D Printing Service BCG Matrix

- Binder Jetting 3D Printing Service Business Model Canvas

- What Five Core KPIs Should Binder Jetting 3D Printing Service Business Track?

- Binder Jetting 3D Printing Service Business Plan Template in Pre-Written Word

- How Increase Profits Binder Jetting 3D Printing Service?

- What Are Operating Costs For Binder Jetting 3D Printing Service?

- Binder Jetting 3D Printing Startup Costs: $213M CAPEX To Open

- Binder Jetting 3D Printing Service Financial Model Template in Excel

- How To Open A Binder Jetting 3D Printing Service In 6-12 Months

- How To Write A Business Plan For Binder Jetting 3D Printing Service?

- Binder Jetting 3D Printing Service Marketing Mix

- Binder Jetting 3D Printing Service Marketing Plan

- Binder Jetting 3D Printing Service Business Proposal

- Binder Jetting 3D Printing Service PESTEL Analysis

- Binder Jetting 3D Printing Service Pitch Deck Example Editable PPTX

- Binder Jetting 3D Printing Service Business SWOT Analysis

- Binder Jetting 3D Printing Service Value Proposition Canvas

Frequently Asked Questions

It can show strong contribution early, but full profitability depends on fixed costs The supplied Year 1 assumptions show $296M revenue, about $8266k in direct costs, and about $213M contribution Rent, admin payroll, equipment financing, taxes, and reinvestment are not supplied, so operating profit and owner draw need those inputs