Owner income$150k

Owner income$150kHow Much Does a Business Coaching Owner Make? $150K Salary

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k  Net margin42%

Net margin42% Revenue for target pay$2.2M

Revenue for target pay$2.2M Business difficultyHard

Business difficultyHard

You’re trying to separate coach revenue from real owner pay This breakdown covers business coaching revenue and profit, a modeled $150,000 founder salary, operating costs, reserves, and small-team growth from launch through a mature year Income depends on pricing, client load, delivery model, lead flow, costs, and reinvestment, not employee salary benchmarks or tax advice

Owner income$150kNet margin42%Revenue for target pay$2.2MBusiness difficultyHardWant to test your own coaching income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay. The model reaches breakeven in Month 32 and payback takes 56 months, so early owner draw can be tight.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. The model breaks even in Month 32 and pays back in 56 months, so owner pay is tighter before scale.

How do I check owner income in the Business Coaching model?

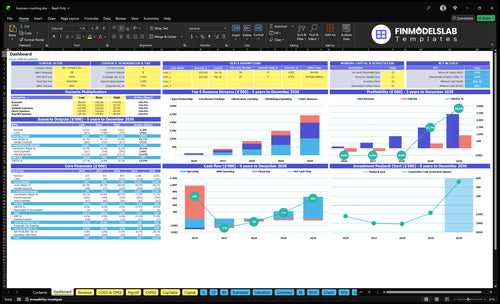

Yes — the Business Coaching Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions, with charts from about $78k to $221M in revenue and -$253k to $925k in EBITDA; open it to see the full income model.

Owner-income model highlights

- Owner take-home assumptions

- Revenue and EBITDA charts

- Pricing and CAC sensitivity

How much can a solo business coach make?

If you're coaching solo, Business Coaching can generate $1,400 from 4 billable hours at $350/hour before overhead; the ceiling is set by price, client capacity, delivery hours, and sales time. For focus and positioning, see What Is The Main Focus Of Your Business Coaching Business?.

Revenue Math

- $250/hour coaching low-end price

- $500/hour coaching high-end price

- $400/hour Year 1 workshop rate

- $1,400 from 4 hours at $350/hour

Time Limits

- Deduct discovery calls

- Deduct prep and follow-up

- Deduct content and admin

- Reserve cash for marketing, tools, support

How much revenue does a business coach need to pay themselves?

If the owner wants $150k pay in Business Coaching, the plan needs about $415k revenue at breakeven before profit; Year 1 revenue of about $78k explains the -$253k EBITDA. Here’s the quick math: with 75% contribution after direct and variable costs, the model also carries $80k non-owner payroll, $612k fixed overhead, and $20k marketing. By Year 5, about $221M revenue supports the same $150k salary and positive EBITDA, but that pay is a planning output, not guaranteed compensation.

Year 1 math

- $150k target owner pay

- 75% contribution rate

- $415k breakeven revenue

- $78k Year 1 revenue

Pay guardrails

- $80k non-owner payroll

- $612k fixed overhead

- $20k marketing cost

- -$253k EBITDA in Year 1

What is a realistic business coaching profit margin?

A realistic profit margin for Business Coaching starts with 82%-86% gross margin, because direct delivery costs are only 18% of revenue in Year 1 and 14% in Year 5; if you’re sizing launch spend, see What Is The Estimated Cost To Open And Launch Your Business Coaching Service?. The real squeeze is the fixed base: $51k/month overhead, payroll rising from $230k to $610k, and marketing from $20k to $180k, which is why EBITDA moves from -$253k to $925k as revenue scales.

Gross margin

- 18% direct delivery cost in Year 1

- 14% direct delivery cost in Year 5

- 82%-86% gross margin range

- Labor and tools drive most delivery cost

Scale pressure

- $51k/month fixed overhead

- Payroll grows from $230k to $610k

- Marketing grows from $20k to $180k

- EBITDA rises from -$253k to $925k

Want the six biggest income drivers?

1

$250-$580Pricing Mix

Higher hourly rates and package tiers lift revenue fast, from $250 for Momentum Coaching to $580 for Apex Partnership.

2

$51K/moCost Control

Fixed overhead starts near $51K a month, so rent, payroll, and tools hit EBITDA hard until breakeven in Month 32.

3

1.5-10hBillable Hours

More billable hours per client pushes revenue up without adding much overhead, especially in the higher-tier packages.

4

60%-40%Client Retention

Keeping clients in the stack longer shifts mix away from Momentum Coaching and supports steadier take-home.

5

$1K->$800Acquisition Cost

Lower customer acquisition cost (CAC) means each marketing dollar buys more clients as spend rises from $20K to $180K.

6

15%-20%Delivery Mix

Workshops and speaking can add reach, but if this share grows too fast it can pull time from higher-margin coaching.

Business Coaching Core Six Income Drivers

Pricing And Package Structure

Tiered Pricing

This driver is the rate card and package scope: entry coaching at $250-$280/hour, mid-tier coaching at $350-$400/hour, top-tier advisory at $500-$580/hour, and workshops at $400-$450/hour. The inputs are client count, billable hours, tier mix, and whether work is sold by the hour or as a package. Higher tiers lift revenue per client without a matching rise in delivery time.

Here’s the quick math: a $50/hour increase matters most when a client books 4 to 10 billable hours, because that adds $200 to $500 per client. If hours stay flat, more of each sale becomes profit and owner pay. What this estimate hides is scope creep; extra calls or prep can erase the margin gain.

Price by Outcome

Track realized rate, not just list price. Compare booked hours, prep time, revisions, and renewals by tier so you can see which package actually pays. Premium pricing depends on niche, credibility, offer clarity, and client outcomes, not wishful positioning. If clients need heavy hand-holding to get results, the higher rate will not hold.

Test price changes in small steps and tie them to a clear promise. If a package takes the same time but closes at $400/hour instead of $350/hour, the extra $50/hour drops straight into gross profit before fixed overhead. Keep workshops priced for facilitation time, not just seat count, and update the package when delivery hours start to drift.

1

Client Capacity And Utilization

Client Load And Billable Time

Owner income rises when more of the week is sold to clients and less is lost to non-billable work like discovery calls, proposals, prep, notes, content, follow-up, billing, and renewals. In this model, delivery assumptions range from 15 hours for lighter coaching to 8 to 10 hours for higher-touch advisory, so a fuller client load can lift revenue fast.

Here’s the tradeoff: one more high-touch client can add more income than several low-touch clients, but only if the owner still has time for sales and delivery control. If the week gets packed, quality slips first, then retention and referrals follow. That’s the real cap on owner pay.

Track Billable Capacity Weekly

Track paid clients, billable hours, and non-billable hours each week. That mix tells you whether income growth is coming from better utilization or just from overload. If client work is creeping toward the full week, the owner may need to raise prices, narrow scope, or cut admin time before quality drops.

- Measure hours sold per client.

- Separate billable and admin time.

- Watch for sales time squeeze.

- Protect delivery quality first.

Simple test: if adding one client forces slower follow-up, weaker prep, or missed renewals, the practice is past its safe capacity. The fix is not always more clients; sometimes it is tighter packaging, clearer boundaries, or a better mix of higher-touch and lighter-touch work.

2

Retention And Recurring Revenue

Retention and Recurring Revenue

When clients stay longer, the owner keeps billing without replacing lost accounts. That matters here because acquisition cost starts at $1,000 in Year 1 and only improves to $800 by Year 5, so early churn burns marketing cash fast. Track renewal rate, average client months, churn, and revenue per retained client to see how much income is really recurring.

More retention spreads CAC over more billed sessions, so take-home income rises even if top-line growth stays flat. Here’s the quick math: a client kept for 10 months carries less acquisition drag than one kept for 5 months. What this hides is fit risk; retention depends on perceived value, measurable progress, and consistent delivery, not just contract terms.

Measure Renewal, Not Just New Sales

Start with a simple retention dashboard. If renewal rate drops, churn rises, and owner pay gets squeezed because replacement work eats time and cash. For coaching retainers, watch whether each client is seeing clear progress by month 1, 2, and 3; if not, the account is at risk.

Use this checklist to protect recurring revenue:

- Renewal rate by cohort

- Average client months

- Churn by offer type

- Revenue per retained client

Then fix the real drivers: tighter client fit, clearer goals, and steady follow-through. If clients can point to measurable wins, retention improves and the owner keeps more of each dollar already spent to win the account.

3

Delivery Model Mix

Delivery Mix and Revenue per Owner Hour

The mix of 1:1 coaching, group programs, workshops, and advisory retainers changes how much revenue each owner hour can produce. Coaching rates here run from $250 to $580 per hour, while workshop rates run from $400 to $450 per hour. One-on-one is easier to sell and customize, but it caps capacity.

Group and workshop formats can raise revenue per hour, but they also add curriculum, sales, logistics, and facilitation work. If associate coaches deliver part of the offer, quality control gets harder, so margin can slip even when topline revenue grows. The key inputs are billable hours, delivery mix, prep time, and labor tied to each format.

Track Mix by Margin, Not Just Sales

Measure revenue per owner hour by format, not just total bookings. Here’s the quick math: if a workshop brings in $450 per hour but takes heavy prep and logistics, the real margin can trail simpler coaching at $250 to $580 per hour. One clean rule: price the delivery burden, not just the session length.

- Track owner billable hours weekly.

- Separate prep, sales, and delivery time.

- Test margin by format each month.

- Watch quality scores on associate-led work.

If the mix shifts toward groups and workshops, forecast extra curriculum build, support labor, and follow-up time. If onboarding associates takes too long, service quality drops and renewals weaken, which cuts owner pay fast. Keep the mix simple until you can prove higher hourly revenue after all delivery costs.

4

Lead Generation Efficiency

Lead Generation Efficiency

Lead generation efficiency is how much of each marketing dollar turns into qualified clients. With budget rising from $20k in Year 1 to $180k in Year 5, the key math is simple: clients acquired = marketing spend ÷ CAC. When CAC improves from $1,000 to $800, the same spend buys more clients and protects owner take-home. Broad messaging usually lifts CAC because prospects cannot see the fit.

For a coaching business, this driver includes referrals, partnerships, content, speaking, and targeted outbound. Better niche positioning lowers wasted spend, shortens the sales cycle, and keeps booked calls more qualified. One weak channel can drain cash fast. What this estimate hides is payback timing: if leads take too long to close, cash flow tightens even when revenue later looks fine.

Tighten the lead path

Track booked calls, close rate, conversion rate, sales cycle, and payback period by source. Split referrals, content, speaking, partnerships, and outbound so you can see which channel brings the best-fit clients at the lowest CAC. Measure the channel, not just the total lead count.

Test tighter messaging around one niche, one problem, and one outcome. If broad outreach raises CAC above $1,000, cut waste before scaling spend. Lower-friction sources should produce steadier revenue and faster owner pay because fewer dollars are lost to unqualified calls, long follow-up, and weak close rates. Keep the best channels, then scale them first.

5

Operating Cost Discipline

Operating Cost Discipline

When fixed overhead sits at $51k/month, the business needs steady billings just to protect owner pay. That’s $612k/year before the owner takes a draw, and payroll can rise from $230k to $610k as the team scales. One clean line: every extra fixed cost has to earn its keep fast.

Here’s the risk: office space, tools, and hires added before revenue is consistent can squeeze cash and delay distributions. Technology and travel can also swing hard, from 7% to 55% of revenue, so the owner needs tight spend control and a clear link between each cost and booked client work.

Cut Fixed Costs First

Track monthly overhead by line item: rent, utilities, insurance, legal, accounting, office tools, website upkeep, payroll, tech, and travel. Keep support hires tied to signed revenue, not forecasted growth. If a cost does not improve close rate, retention, or delivery capacity, it should stay small.

- Compare spend to booked revenue.

- Review payroll before each hire.

- Use trained support for scale.

- Delay office upgrades until stable.

Useful growth spend goes to client success and trained support, because that can protect retention and reduce founder overload. What this estimate hides is timing: if revenue is lumpy, even “good” overhead can strain cash and cut into owner pay fast.

6

Compare low, base, and high business coaching income scenarios

Owner income scenarios

Founder pay here depends on revenue, payroll, and marketing burn. Negative EBITDA years keep take-home closer to salary; stronger years can add distributions after reserves are covered.

| Scenario | Low CaseDownside case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower-income path, where the practice stays small and the founder mostly relies on salary. | This is the modeled middle path, where the business approaches break-even but still leaves little room for owner distributions. | This is the stronger earnings path, where scale and margin support founder pay plus possible distributions. |

| Typical setup | About $78k revenue, 82% gross margin, $20k marketing, $1,000 CAC, and $230k payroll keep EBITDA near -$253k. | About $730k revenue, 84% gross margin, $80k marketing, $900 CAC, and $440k payroll leave EBITDA near -$13k. | A scaled team, about 86% gross margin, $180k marketing, $800 CAC, and $610k payroll support EBITDA of $925k. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $150k salarySalary only | $150k salaryNear breakeven | $150k salary + distributionsSalary plus upside |

| Best fit | Use this to stress test a thin launch year and tight cash control. | Use this as the main planning case for one founder salary and little extra owner draw. | Use this to test what owner take-home can look like once cash, reserves, and reinvestment needs are covered. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Business Coaching Porter's Five Forces Analysis

- Business Coaching BCG Matrix

- Business Coaching Business Model Canvas

- 7 Essential KPIs to Track for Business Coaching Success

- Business Coaching Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Business Coaching Profitability

- How Much Does It Cost To Run Business Coaching Monthly?

- Business Coaching Startup Costs: $51k CAPEX to $289k Cash Need

- Business Coaching Financial Model Template in Excel

- How To Start A Business Coaching Practice In 30 To 90 Days

- How to Write a Business Coaching Business Plan: 7 Actionable Steps

- Business Coaching Marketing Mix

- Business Coaching Marketing Plan

- Business Coaching Business Proposal

- Business Coaching PESTEL Analysis

- Business Coaching Pitch Deck Example Editable PPTX

- Business Coaching Business SWOT Analysis

- Business Coaching Value Proposition Canvas

Frequently Asked Questions

In this model, the owner salary is $150,000 per year, but distributions depend on profit EBITDA is -$253,000 in Year 1, -$13,000 in Year 3, and $925,000 in Year 5 So early take-home may be salary only, while later upside depends on taxes, reserves, and reinvestment