Owner income$70k-$197k

Owner income$70k-$197kHow Much Candle Business Owners Make: $70k-$197k Year 1

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$70k-$197k  Net margin24%

Net margin24% Revenue for target pay$253k

Revenue for target pay$253k Business difficultyMedium

Business difficultyMedium

A candle making business owner can model about $70,000-$197,000 in Year 1 owner pay capacity before taxes and reserves if the business hits 16,500 units and $525,000 in revenue Here’s the quick math: average selling price is about $3182, gross margin after listed candle costs is about 706%, and contribution margin after packaging, shipping, and payment fees is about 576% The $197,000 figure includes the $70,000 founder salary plus about $127,000 of operating profit capacity Take-home depends on pricing, units sold, channel mix, costs, marketing, labor, and cash reserves

Owner income$70k-$197kNet margin24%Revenue for target pay$253kBusiness difficultyMediumWant to test your candle pay number?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

How do I check owner income in the Candle Making Business model?

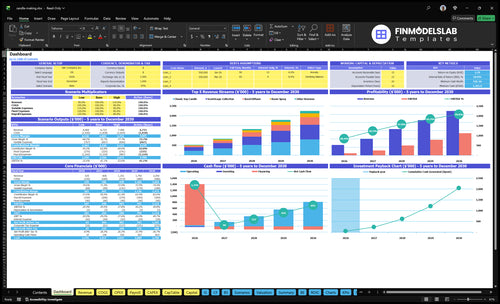

The dashboard shows revenue, assumptions, pricing, unit economics, product and channel mix, expenses, payroll, scenarios, and owner income. Open the Candle Making Business Financial Model Template.

Owner-income model highlights

- Owner salary and reserves

- Revenue and margin charts

- Scenario testing tables

What is a good profit margin for a candle business?

If you’re pricing a Candle Making Business, a good target is a healthy gross margin, not just a high sticker price; the cost math is the same idea you’d use in How Much Does It Cost To Open And Launch Your Candle Making Business?. In Year 1, the listed unit price is $3,182 against $913 in unit cost, so gross margin is about $2,269, or roughly 71%. After 10% for packaging and shipping and 3% for payment fees, contribution margin is about 58%, but wax, fragrance, vessels, wicks, labels, packaging, shipping, merchant fees, and labor still shrink owner take-home.

Margin math

- $3,182 listed selling price

- $913 listed unit cost

- 71% gross margin

- 58% contribution margin

Owner take-home

- Wax and fragrance cost money

- Vessels and wicks add up

- Labels and packaging reduce pay

- Labor cuts into net profit

How many candles do I need to sell to pay myself?

If you’re asking how many candles the Candle Making Business needs to sell to pay you, the Year 1 target is about 9,550 units at a $31.82 average selling price to cover $105k in non-owner fixed costs and payroll plus $70k in founder pay. That works out to about $304k in revenue, and the Year 1 plan of 16,500 units is above that line. If average order value rises, the unit count needed drops.

Year 1 math

- 576% margin after listed costs

- $304k revenue target

- 9,550 units needed

- 16,500 units planned

What moves the count

- Higher order value lowers units

- Fixed costs stay at $105k

- Founder pay adds $70k

- More sell-through makes pay possible

Is selling candles online or wholesale more profitable?

For the Candle Making Business, direct online sales usually keep more pricing power, but they also bring payment fees, packaging, shipping, software, and marketing work. Wholesale can move more units, yet it usually means lower selling prices and tighter production discipline, so higher revenue is not always higher take-home.

Direct online sales

- Keep pricing control.

- Pay card processing fees.

- Cover packing and shipping.

- Spend on ads and software.

Wholesale and local volume

- Move more units faster.

- Accept lower unit prices.

- Need tighter batch control.

- Use gifting or subscriptions for repeat orders.

Want the six drivers that move candle income most?

1

16.5KSales Volume

Year 1 sells 16,500 units and brings in $525,000, so every extra batch lifts owner income fast after fixed costs.

2

$31.82Pricing Mix

The Year 1 average price is $31.82 per unit, and a bigger mix of higher-priced items raises take-home without adding much overhead.

3

29%Material Costs

Direct product costs run about $150.6K in Year 1, or 29% of revenue, so small savings in wax, fragrance, vessels, and packaging move profit fast.

4

$130KOverhead Load

Year 1 payroll is $130K and fixed overhead is $3,750 a month, so the business has to cover taxes, reserves, and reinvestment before owner pay.

5

13%Channel Mix

Packaging and shipping take 10% and payment fees add 3% in Year 1, so the sales channel can swing take-home by 13% of revenue.

6

$28KMarketing Costs

Year 1 marketing payroll and software total about $28K, so spend has to turn into repeat orders quickly or it drags owner income.

Candle Making Business Core Six Income Drivers

Pricing and Product Mix

Pricing and Product Mix

This driver is the mix of price points and bundles that sets revenue per customer. Premium candles at $45 lift average order value faster than $18 wax melt sets, and gift boxes or limited drops can add revenue without many extra units. The disclosed Year 1 average selling price is about $3,182 across candles, diffusers, sprays, and wax melts.

The risk is clear: if a price increase slows conversion, profit can fall even when unit margin improves. To estimate the impact, the owner needs customer count, order count, conversion rate, average order value, and gross margin by product line. One clean rule: raise price only when perceived value and cost structure still support demand.

Test AOV, not just sticker price

Track average order value, conversion rate, discount rate, and gross margin after every price change. A bundle, gift box, or upsell should raise profit per order enough to cover packaging, shipping, and marketing time. If AOV rises but conversion drops hard, the owner may end up with less cash for overhead and salary.

- Compare AOV by product line.

- Test bundles before deeper discounting.

- Watch conversion after price changes.

- Track profit per order weekly.

Use premium candles at $45 to anchor the range, and use lower-priced wax melt sets to bring in first-time buyers. The key check is simple: keep the higher price only if total contribution still improves after fees and slower sell-through. That is what funds owner pay.

1

Sales Volume and Repeat Customers

Sales Volume and Repeat Customers

Volume turns margin into owner income. This driver includes units sold, repeat rate, seasonality, subscriptions, and corporate gifting. The plan grows from 16,500 units in Year 1 to 64,000 units in Year 5, or about 1,375 to 5,333 units a month.

Here’s the quick math: 64,000 ÷ 16,500 = 3.9x more units by Year 5. That helps only if gross margin holds and cash keeps up, because wax, fragrance, vessels, packaging, storage, and labor are paid before many customers pay you. If inventory grows faster than cash, owner draws get squeezed.

Track Repeat Demand and Cash

Measure monthly units sold, repeat purchase rate, subscription share, and corporate gifting orders. Then watch seasonality so you can buy raw materials in the right batch size and avoid stockouts or dead inventory.

- Set reorder points for key inputs.

- Match labor hours to forecasted units.

- Use a cash forecast before growth.

2

Channel Mix

Channel Mix

Channel mix is the split between direct-to-consumer, wholesale, craft fairs, local retail, and marketplace sales. It changes owner income because each channel carries different costs. Direct-to-consumer can protect price, but payment fees, packaging, shipping, ecommerce software, and marketing time cut take-home. The key test is contribution margin — revenue left after channel costs.

For a candle business, a channel with more sales can still pay less cash. Wholesale may raise unit volume but often compresses margin, while craft fairs and local retail add labor, booth fees, and inventory risk. If the channel does not help cover the business’s $3,750/month fixed overhead, it can grow revenue and still reduce owner pay.

Track Margin by Channel

Build a simple channel P&L for each route to market: units, average order value, payment fees, shipping, packaging, labor hours, booth costs, and marketplace fees. Then compare contribution margin per order and per hour. That shows which channel actually funds salary and draw, not just top-line sales.

Test the mix before scaling. If a channel needs heavy marketing time or slow-moving inventory, it ties up cash and can squeeze payroll. Keep the channels that cover fixed overhead fastest, and cap the ones that add volume but lower profit. That is usually where owner income improves first.

3

Material Costs and Batch Efficiency

Material Cost per Sellable Unit

Material cost covers wax, fragrance, vessels, labels, packaging, and any scrap from defects or failed pours. In Year 1, the listed unit materials average is about $913 per unit, but the mix matters a lot: soy candles are $780, premium candles $1,450, diffusers $950, room sprays $545, and wax melts $305. Higher input cost only helps if price and sell-through stay strong.

Here’s the quick math: when batch size is off, waste rises and cash gets tied up in unusable inventory. A failed batch, a leaky vessel, or extra packaging can erase the savings from buying cheaper materials. For the owner, that means lower gross margin, more working capital tied in stock, and less profit available for pay draws.

Track Yield, Scrap, and Unit Mix

Measure materials per good unit, not just supplier spend. Track batch yield, scrap rate, defect rate, and the share of sales from each product line so you can see whether premium candles, sprays, or wax melts are lifting or dragging margin. One useful check is: total materials cost divided by sellable units shipped.

Set simple controls around supplier pricing, batch size, and packaging choices. If a batch produces fewer sellable units than planned, stop and fix the process before scaling. Protect safety and quality first, because one return or failed batch can cost more than a full day of cheap-material savings. That discipline keeps gross margin and owner cash more stable.

- Track cost per sellable unit

- Watch scrap after every batch

- Test packaging before scaling

- Price premium items for margin

4

Marketing and Customer Acquisition Cost

Customer Acquisition Cost

Revenue growth only helps when each new customer creates more gross profit than it costs to win them. The model includes a 0.5 FTE marketing and ecommerce role in Year 1 and $100/month in marketing software, so paid ads, content, email, referrals, wholesale outreach, and events must be judged on order profit, not clicks or followers.

Here’s the quick math: if acquisition cost rises faster than repeat orders, the owner’s income gets squeezed even when sales look better. Track customers, orders, AOV (average order value), repeat purchase rate, and gross profit per order; if a channel can’t pay back fast, it adds volume but not take-home pay.

Track Order Profit

Measure CAC by channel and compare it to gross profit per order. A channel that brings steady repeat buyers can support owner pay; a channel that only buys one-time orders cannot. Keep spend, conversion rate, and repeat rate in one view so you can see which source actually pays back.

If acquisition costs rise faster than repeat orders, tighten owner distributions and slow the channels that lose money after the first sale. The goal is not just more revenue; it’s more cash after ads, software, and the marketing role are paid.

- Track CAC by channel.

- Compare spend to gross profit.

- Watch repeat order rate closely.

- Cut weak channels fast.

5

Overhead, Capacity, and Owner Role

Fixed Overhead and Founder Pay

$3,750/month of fixed overhead covers rent, utilities, insurance, ecommerce fees, marketing software, accounting and legal, plus U.S. Consumer Product Safety Commission compliance and testing. That is $45,000/year before one extra candle sells. Add $130k in Year 1 payroll, including the $70k founder salary, and the business has to clear a lot of fixed cost before owner pay turns into real cash.

Owner-operated profit is not the same as unpaid owner labor. If the founder works more hours without charging payroll, reported profit can overstate the real take-home. Hiring help can raise batch capacity and order throughput, but short-term income usually drops unless shipped volume rises fast enough to absorb the extra labor.

Track Capacity Before You Hire

Measure monthly orders, units per batch, founder hours, and labor cost per unit. Here’s the quick math: $45,000 in annual fixed overhead plus $130,000 payroll means every staffing choice has to protect contribution margin, not just sales. If compliance testing or fulfillment delays slow turns, cash gets tied up fast.

- Track hours per batch

- Test hire timing against volume

- Watch payback from added output

- Separate founder pay from profit

If a helper adds capacity but orders do not rise, the owner funds more payroll with no offset. The safer move is to hire only when weekly volume is already near the founder’s ceiling and the added labor can be tied to shipped orders, not just busier days.

6

Compare lean, base, and high candle owner income scenarios

Owner income scenarios

Owner pay moves with unit volume, mix, and fee drag. The low case tests thin demand against fixed overhead and payroll; the high case shows later-scale profit room.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Owner income stays tight because lower volume leaves less room after fixed costs and payroll. | Owner income follows the modeled Year 1 plan, where scale supports a founder salary and profit on top. | Owner income rises when the business reaches Year 5 scale and lower fee rates lift profit capacity. |

| Typical setup | The shop runs below Year 1 volume, keeps the same workshop overhead, and gives the founder a smaller draw. | The model uses 16,500 units, $525k revenue, 70.6% gross margin, 57.6% contribution margin, and a $70k founder salary. | The model reaches 64,000 units and about $2.25M revenue, with shipping at 6.0% and payment fees at 2.4%. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $30k - $70kLow band | $70k - $197kBase band | $250k - $1.1MUpside band |

| Best fit | Use this to stress-test early months if demand lags and the founder takes a smaller draw. | Use this for core budgeting, hiring, and owner pay planning. | Use this to test upside if the line reaches Year 5 scale and fees keep falling. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Candle Making Business Porter's Five Forces Analysis

- Candle Making Business BCG Matrix

- Candle Making Business Business Model Canvas

- 7 Key Financial Metrics to Scale Your Candle Making Business

- Candle Making Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Candle Making Business Profitability

- Estimating Monthly Running Costs for a Candle Making Business

- Candle Making Business Startup Costs: $268K CAPEX Guide

- Candle Making Financial Model Template in Excel

- How To Start A Candle Business In 6–12 Weeks With Tested Products

- How to Write a Business Plan for a Candle Making Business

- Candle Making Business Marketing Mix

- Candle Making Business Marketing Plan

- Candle Making Business Business Proposal

- Candle Making Business PESTEL Analysis

- Candle Making Business Pitch Deck Example Editable PPTX

- Candle Making Business Business SWOT Analysis

- Candle Making Business Value Proposition Canvas

Frequently Asked Questions

In this model, Year 1 owner pay capacity is about $70,000-$197,000 before taxes and reserves That includes a $70,000 founder salary plus about $127,000 of operating profit capacity if the business reaches $525,000 revenue and 16,500 units sold Actual take-home depends on cash reserves, tax planning, debt, and reinvestment