Owner incomeUp to $215k

Owner incomeUp to $215kHow Much Can A Craft Cidery Owner Make By Year 2?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeUp to $215k  Net margin12% Y2

Net margin12% Y2 Revenue for target pay$785k

Revenue for target pay$785k Business difficultyHard

Business difficultyHard

A craft cidery owner may take home little or nothing in Year 1 if the business opens with a full production and taproom team Under these researched assumptions, Year 1 revenue is about $395,000, but listed payroll, fixed overhead, COGS, and variable costs leave roughly negative $47,000 before owner pay, taxes, debt principal, and reserves By Year 2, revenue rises to about $785,000 and cash available before those items is about $215,000 Treat that as planning capacity, not a guaranteed cidery owner salary

Owner incomeUp to $215kNet margin12% Y2Revenue for target pay$785kBusiness difficultyHardWant to test your cidery owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

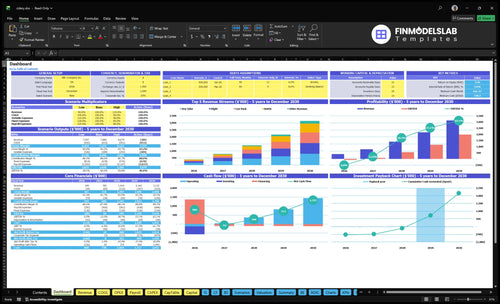

Want to check owner income in the Craft Cidery model?

This dashboard shows revenue, gross margin, payroll, fixed overhead, reserves, and owner take-home in the Craft Cidery Financial Model Template. Open it.

Owner-income model highlights

- Owner cash-out: cash available

- Revenue path: Year 1 $395,000; Year 2 $784,700; Year 5 $3,131,500

- Scenarios: units, prices, debt

How much does a cidery owner make per year?

A Craft Cidery owner likely makes $0 in Year 1 under these assumptions; revenue of $395,000 is already pressured by 48% variable costs, $135,600 fixed overhead, and $253,000 listed payroll before full admin detail. For startup planning, see How To Launch A Craft Cidery?; Year 2 shows about $215,000 before owner pay, taxes, debt principal, reserves, and distributions.

Year 1 Pay

- $395,000 annual revenue

- 48% variable cost load

- $135,600 fixed overhead

- $253,000 listed payroll

Owner Economics

- $215,000 Year 2 pre-owner pool

- Salary means paid labor

- Distribution means after-profit payout

- Owner labor can mask true cost

Can a small cidery support an owner?

Yes, Craft Cidery can support an owner, but not safely in year 1 under this staffed model. Year 1 revenue of $395,000 does not cover the listed operating structure plus owner pay. Year 2 revenue of $784,700 creates about $215,000 before taxes, debt principal, reserves, and owner distributions.

Year 1 gap

- $395,000 revenue is too thin

- Owner pay is not covered safely

- Seasonality can weaken taproom traffic

- Compliance work adds labor load

Year 2 upside

- $784,700 revenue changes the picture

- About $215,000 stays before key claims

- Inventory cash gets tied up in fermentation

- Maintenance and payroll still need reserves

How much revenue does a cidery need to pay the owner?

Craft Cidery needs about $449,000 in annual revenue before owner pay, taxes, debt principal, or reserves. Here’s the quick math: $135,600 in fixed overhead plus $253,000 in payroll equals $388,600, and at a blended contribution margin near 86.6% that means roughly $449,000 in sales. Year 1 revenue is $395,000, so it falls short by about $54,000; adding a $75,000 owner target pushes the need to about $535,000.

Cost load

- Payroll: $253,000

- Overhead: $135,600

- Blended margin drives the floor

- Taproom share helps margin

Revenue target

- Break-even: about $449,000

- Year 1: $395,000

- Gap: about $54,000

- With $75,000 owner pay: about $535,000

What drives cidery owner income most?

1

$258KTaproom Traffic

Flights and dry cider bring in about $258K in Year 1, so higher tasting traffic and check size lift owner cash fast.

2

$137KSales Mix

Can packs, bottles, and merch add about $137K in Year 1, and the taproom-to-retail split sets margin and cash timing.

3

95KProduction Volume

Dry cider scales from 20K units in Year 1 to 95K by Year 5, so output and yield are the core growth lever.

4

$0.60-$1.00Packaging Cost

Per-unit cider and packaging cost runs about $0.60 to $1.00, so bottle-heavy mix can squeeze take-home.

5

$253KLabor Load

Listed payroll is about $253K in Year 1, so staffing and how much the owner does directly hit EBITDA.

6

$135.6KOverhead Floor

Fixed overhead is about $135.6K a year, and breakeven does not arrive until month 14.

Craft Cidery Core Six Income Drivers

Taproom Traffic And Ticket Size

Taproom Traffic

Direct taproom sales turn visitors into cash fast. At $18 per flight and 6,000 units in Year 1, flights generate $108,000. By Year 5, 38,000 units at $20 reach $760,000. That matters because direct sales keep more gross profit inside the business, so owner pay rises faster when labor and pour costs stay controlled.

This driver includes flights, dry pours, bottles to-go, can packs, merchandise, private events, and repeat guests. The key inputs are guest count, ticket size, and traffic mix by day. Slow weekday traffic or weak local demand can leave fixed labor and rent undercovered, so cash for the owner improves only when sales grow faster than staffing.

Track Spend Per Guest

Measure visits, average ticket, and sales by daypart. Here’s the quick math: revenue = visits × ticket size, so lifting spend with add-ons can matter as much as adding seats. Watch whether each tasting, event, or promo adds profitable dollars, not just foot traffic.

- Track weekday and weekend visits.

- Track ticket size by product mix.

- Compare labor hours to sales.

If weekday demand is thin, push bundles, private events, and to-go packs before adding labor. What this estimate hides is mix: higher direct sales help owner income only if card fees, pour cost, and payroll stay in line.

1

Sales Channel Mix

Sales Channel Mix

Sales channel mix is the split between taproom sales and wholesale. Direct sales keep more gross profit because you keep the retail margin on flights, dry cider, cans, bottles, and merchandise, while wholesale adds distributor margin and more packaging, delivery, and sales labor. The model does not give a wholesale split calculator, so owner income will swing with how much volume stays direct.

The key test is channel contribution after packaging, delivery, sales labor, card fees, and reserves. More direct-to-consumer volume usually improves blended margin, but slow taproom traffic or thin wholesale pricing can leave the owner with low cash even when top-line revenue grows.

Protect Direct Margin

Track revenue and cost by channel, not as one blended line. Use wholesale share, distributor margin, average order value, and channel labor to forecast owner pay. If channel contribution can cover $11,300 per month of fixed overhead, the draw gets safer; if not, growth just adds work.

- Split taproom and wholesale revenue.

- Test wholesale-share scenarios.

- Set distributor margin by channel.

- Track packaging and delivery per case.

- Staff to protect peak-margin hours.

2

Production Volume And Yield

Production Volume And Yield

Production volume only raises income when every gallon turns into sellable cider that moves fast enough. In this model, dry cider units rise from 20,000 in Year 1 to 95,000 in Year 5, can packs from 3,000 to 30,000, and bottles from 2,000 to 20,000. If tanks are full but product sits, cash gets tied up and owner pay gets squeezed.

The key inputs are tank utilization, fermentation loss, spoilage, and sell-through speed. Here’s the quick math: more output helps only when the channel price covers packaging and labor. If packaging is prepaid or pricing is thin, extra gallons can lift revenue on paper but still lower free cash for the owner.

Track Yield Before You Chase Volume

Measure batch yield from apples in to cases out, then compare it with the planned unit mix. Watch the gap between produced and sold units each month, not just the brew schedule. If inventory days rise, reduce production or push faster-moving packs first.

Also track tank turns, spoilage rate, and sell-through by channel. A simple rule: more volume should improve cash only when finished goods leave the building faster than packaging and ingredient cash go in. If not, the owner is financing stock instead of taking profit.

3

Cider COGS And Packaging

Cider COGS

COGS is the cost of the cider you sell: apples or juice, yeast, utilities, glassware, cans, bottles, corks, labels, carriers, sample glasses, flight boards, garnishes, merchandise packaging, freight, fermentation loss, and excise tax. In Year 1, modeled COGS is about $33,944 on $395,000 of revenue, or about 8.6%. Keep this low and owner take-home improves fast; let it creep up, and gross margin shrinks before fixed costs even hit.

Here’s the quick math: every extra 1 point of COGS on $313 million of Year 5 revenue is about $3.13 million less gross profit. That is why apple cost, packaging orders, and freight matter so much. One bad supplier deal or higher spoilage can wipe out a lot of cash, even if sales keep rising.

Track cost per finished unit

Measure COGS per gallon and per packaged unit, then separate taproom pours from cans, bottles, and merchandise packaging. Watch apple or juice cost, packaging orders, freight, and fermentation loss every month. If any one moves, your gross margin moves too, and that changes how much cash is left for owner pay.

Set reorder points before peak season, and price for the full unit cost, not just ingredients. Also track excise tax by channel, because direct sales can still look strong while net profit falls if packaging and loss rates rise. One clean rule: if the unit cost goes up, the owner only keeps the gap if price follows.

4

Labor And Owner Role

Labor and Owner Role

Labor is the biggest early cash pressure here. Listed Year 1 payroll is $253,000 across the head cidermaker, taproom manager, production assistant, bartenders, and sales marketing, before incomplete admin detail. If staffing is not matched to sales, that spend cuts straight into the owner’s cash draw.

By Year 2, payroll rises to $335,000, up $82,000 or about 32%. Unpaid owner hours can make profit look better on paper, but they are not a sustainable salary. The real test is whether taproom coverage, production shifts, and event labor stay tight enough to protect cash flow.

Track Coverage Before Pay

Measure taproom coverage, production shifts, event labor, payroll taxes, and management backup every week. Here’s the quick math: if labor rises faster than sales volume, owner take-home falls even when the business looks busy. That is the risk hidden inside the payroll line.

Set a simple rule: compare labor hours to open hours and event count, then check whether each added role earns its keep. Keep one person assigned as backup for the taproom and one for production so the owner is not the default fix when demand spikes or staff miss shifts.

- Track labor by shift

- Separate owner hours from salary

- Budget payroll taxes separately

5

Overhead, Debt, And Reserves

Fixed Overhead, Debt, And Reserves

$11,300 a month in fixed overhead, or $135,600 a year, sets the floor the cidery must clear before owner pay. The biggest line is the $5,000 lease, then $2,000 marketing, $1,500 utilities, $1,200 insurance, $700 maintenance, $500 compliance, and $400 POS fees. One weak month can eat cash fast if traffic slows.

Debt principal and reserves sit outside operating profit, so they must be funded after the business covers overhead. The key inputs are monthly sales, debt service, equipment replacement timing, working capital needs, and compliance cash. If owner draw is set from profit without those buckets, take-home is overstated and the business c an look healthier than it is.

Track Cash, Not Just Profit

Build the forecast from taproom revenue, debt payments, and a separate reserve target. Track rent, utilities, insurance, maintenance, compliance, and POS fees each month, then compare them with sales so fixed overhead stays in line. If sales soften, cut variable spend first and keep reserve cash intact for equipment swaps and timing gaps.

- Separate debt principal from profit.

- Fund replacement cash monthly.

- Track working capital weekly.

- Review lease load before renewals.

6

Compare low, base, and high cidery owner-income cases

Owner income scenarios

Owner pay stays tight in year 1, improves in year 2, and only scales in later years if taproom demand, margin quality, and payroll discipline hold up.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Year 1 is a lean run at about $395,000 of revenue, so there is no room for owner pay after the operating load. | Year 2 lifts revenue to about $784,700 and creates roughly $215,000 before owner pay, taxes, debt principal, and reserves. | Later-year scale reaches about $3.132 million of revenue and $1.976 million of EBITDA, with stronger owner pay only if costs stay controlled. |

| Typical setup | Taproom demand is still light, and full staffing plus fixed overhead leave the business focused on covering production and cash burn. | Taproom demand is steadier, but payroll still runs heavy and cash only starts to cover the owner's draw after operating needs are funded. | Dry cider reaches 95,000 units, the mix broadens across flights, cans, bottles, and shirts, and cash holds up if labor and reserves stay tight. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0Low Case | $215,000Base Case | $1.976M pre-taxHigh Case |

| Best fit | Use this to stress-test the first year if traffic is thin and the taproom only covers core overhead. | Use this as the main planning case for staffing, pricing, and debt checks. | Use this to test upside if volume scales fast and the cost base does not outrun sales. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Craft Cidery Porter's Five Forces Analysis

- Craft Cidery BCG Matrix

- Craft Cidery Business Model Canvas

- What Are The 5 Core KPIs For Craft Cidery?

- Craft Cidery Business Plan Template in Pre-Written Word

- How Increase Craft Cidery Profits?

- What Does It Cost To Run A Craft Cidery?

- Craft Cidery Startup Costs: $265k CAPEX Plus Runway

- Craft Cidery Financial Model Template in Excel

- How to Open a Craft Cidery: 9- to 18-Month Launch Roadmap

- How To Write A Business Plan For Craft Cidery?

- Craft Cidery Marketing Mix

- Craft Cidery Marketing Plan

- Craft Cidery Business Proposal

- Craft Cidery PESTEL Analysis

- Craft Cidery Pitch Deck Example Editable PPTX

- Craft Cidery Business SWOT Analysis

- Craft Cidery Value Proposition Canvas

Frequently Asked Questions

A cidery owner may take home $0 in the first year under a full-staffed launch model Here, Year 1 revenue is $395,000, but COGS, 48% variable costs, $135,600 fixed overhead, and listed payroll of $253,000 leave no clean owner-pay room before taxes, debt principal, and reserves