Co-operative Bank Startup Costs For A $100M Year 1 Loan Plan

This guide separates co-operative bank startup cost breakdown items from bank startup capital requirements, so you don’t mix normal spend with balance-sheet funding It covers CAPEX, bank pre-opening expenses, working capital, and regulatory capital planning for a first-year model with $100M in loans, $105M in member deposits, savings, and certificates, and $46K/month in listed fixed operating costs

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a co-operative bank buildout.

Limits to keep in mind This calculator covers capitalized startup assets only. It excludes regulatory capital, legal chartering, deposit insurance application work, pre-opening payroll, working capital, debt service, deposits, inventory, and other operating cash needs. Monthly branch rent of $15,000 and recurring tech spend of $22,000 per month are operating costs, not CAPEX. Final pricing for branch fit-out, ATM install, and security gear should come from vendor quotes.

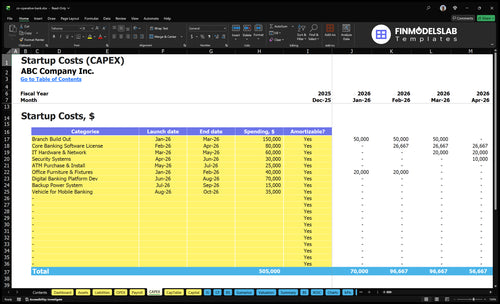

What does this screenshot show?

This Co-operative Bank Financial Model Template tab shows CAPEX and startup costs; review categories, timing, amounts, depreciation, and amortization. Open it and adjust assumptions.

Screenshot highlights

- Branch buildout CAPEX

- Pre-opening startup costs

- Depreciation and amortization

How much does it cost to start a co-operative bank in the United States?

A Co-operative Bank should be planned as a total funding need, not a simple startup-cost list: Year 1 anchors show $124M in interest-earning assets against $113M in member deposits, borrowed funds, and interbank deposits, leaving a $11M funding gap before startup expenses, CAPEX, and runway. Capital for loans and required reserves is balance-sheet funding, not money “spent”; How Is The Member Engagement Growing For Co-operative Bank? matters because member deposits drive that funding base.

Cost Layers

- $100M Year 1 loan book

- $24M other interest-earning assets

- $46K/month known fixed costs

- $22K/month recurring technology spend

Funding Checks

- $105M member deposit products

- $5M borrowed funds

- $3M interbank deposits

- $565K/year minimum known payroll

How to plan funding for a co-operative bank startup?

For a Co-operative Bank startup, plan funding around the balance sheet first: Year 1 assumes $100M in loans, $24M in other earning assets, $105M in member deposit products, $5M in borrowed funds, and $3M in interbank deposits. Using the provided Year 1 math, interest income is about $793M and interest expense is about $213M before operating costs, credit costs, taxes, and capital rules. After that, build the model around startup period costs, launch timing, staffing ramp, technology implementation, branch readiness, and a cash contingency so break-even can be tied to regulatory milestones.

Year 1 funding base

- $100M loans

- $24M earning assets

- $105M member deposits

- $8M outside funding

Launch cost drivers

- Startup period costs

- Staffing ramp timing

- Technology implementation

- Branch readiness and reserves

What hidden costs of starting a co-operative bank do organizers miss?

The main mistake is mixing required capital and liquidity with operating costs; they’re separate, and launch burn can get ugly fast. Hidden costs include pre-opening payroll, audit readiness, compliance testing, Bank Secrecy Act and anti-money-laundering policy work, vendor risk management, cybersecurity reviews, insurance, professional services, member outreach, website build, and launch comms; see How Much Does The Owner Of A Co-Operative Bank Typically Make? for the ownership side. If onboarding or approvals take longer, cash burn rises before fee income starts.

Hidden launch costs

- Capital and liquidity are not opex

- Pre-opening payroll hits before revenue

- Compliance and audit work add cost

- Cybersecurity and vendor checks slow launch

Base model lines

- $3K/month insurance

- $2K/month professional services

- 80% of Year 1 marketing and community development

- 30% of Year 1 card processing fees

Calculate Fuding Needs

Startup cost summary

Shows the main launch assets and the separate opening cash reserve needed before breakeven.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Branch Build Out | $150,000 | Branch shell work, fit-out, and opening readiness | Yes |

| Core Banking Software License | $80,000 | Core banking system setup and licensing | Yes |

| IT Hardware & Network | $60,000 | Workstations, servers, and network infrastructure | Yes |

| Digital Banking Platform Development | $70,000 | Online and mobile banking buildout | Yes |

| Security Systems | $30,000 | Alarm, surveillance, and access control installation | Yes |

| Opening Cash Reserve | $39,501,000 | Non-CAPEX runway for deposits, payroll, and loan funding timing | No |

Co-operative Bank Core Five Startup Costs

Regulatory Formation And Chartering Startup Expense

Charter spend

For a co-operative bank, the one-time startup spend is the legal and filing work around the charter, organizer documents, feasibility studies, business plan support, governance, and regulator communications. If deposit insurance is needed, add Federal Deposit Insurance Corporation application work. The cost shifts with the charter path, state, ownership structure, team depth, community need analysis, and how many feedback cycles the regulator requests.

What it covers

This bucket pays for legal counsel, regulatory consultants, application preparation, organizer documentation, feasibility work, governance materials, and back-and-forth with examiners. Here’s the quick split: one-time professional fees on one side, then regulatory capital and required liquidity on the other. The second bucket is not a fee; it is cash you must have ready to meet approval standards and early operating needs.

- Use counsel for charter filings.

- Budget for regulator revisions.

- Keep capital separate from fees.

How to control it

Trim this cost by picking a clean charter path, keeping the ownership structure simple, and showing a complete management team early. A tighter community need analysis and a realistic capital plan can reduce regulator questions. What this estimate hides is delay risk: every extra feedback cycle adds adviser time, filing edits, and more board work.

- Start with a complete data room.

- Avoid late plan changes.

- Answer regulator comments fast.

Approval timing

Approval work moves faster when the business plan, governance package, and community support proof are consistent from day one. If the management team is thin or the capital story is weak, regulators usually ask for more detail, which pushes up outside help and timeline risk. The practical guardrail is simple: budget for extra review rounds, not just the first filing.

Technology Infrastructure Startup Expense

Core Tech Stack

The launch stack covers the core banking platform, online and mobile banking, data hosting, compliance reporting, payment rails integration, cybersecurity, implementation support, and vendor due diligence. The recurring base model is $22K/month: $10K for core licensing, $5K for cybersecurity, and $7K for digital maintenance.

What Drives Cost

Estimate this with one-time implementation plus monthly run costs. Ask vendors for quotes on setup, conversion, training, and support, then add hosting and software by month. The budget changes with launch channels, account volume, card program scope, reporting depth, and security needs.

- Count setup and conversion separately

- Price monthly software by module

- Match reporting to regulator needs

How To Keep It Lean

Keep scope tight at launch. Start with the channels you need on day one, and avoid paying for extra modules before volume justifies them. Push vendors on bundled pricing for licensing, hosting, and support. Don’t underbuy cybersecurity; that’s where cheap plans get expensive fast.

- Launch fewer channels first

- Bundle vendor services

- Keep security requirements current

Budget Check

Here’s the quick math: recurring tech alone starts at $22K/month, so annual run rate is $264K before one-time setup. That means the launch budget should protect both implementation cash and enough runway for vendor support, testing, and regulator-driven changes without squeezing working capital.

Branch Facilities And Physical Infrastructure Startup Expense

Branch setup costs

A co-operative bank branch needs leasehold improvements, teller stations, furniture, signage, surveillance, access control, ATMs, vault or cash equipment, and member meeting space. Use this as CAPEX planning, then add rent deposits and ongoing occupancy costs separately. The biggest swing factors are branch size and cash-handling scope.

Monthly occupancy

The base model uses $15K/month branch rent, $25K/month utilities, and $15K/month office maintenance, with occupancy modeled at $19K/month. That sits outside buildout CAPEX and should be budgeted as ongoing runway burn, not startup construction spend. The one-line test: if occupancy is high, opening the branch early can strain cash fast.

- Separate deposits from buildout.

- Budget occupancy by month.

- Track cash before opening.

What moves the number

Cost swings with branch size, number of teller stations, cash volume, security scope, landlord work letter, and whether the model is branchless, single-branch, or full-service. More teller lanes and stronger security mean more wiring, more equipment, and more buildout time. Here’s the quick math: more cash flow needs more physical control.

- Small branch: lower buildout.

- More cash: stronger vaulting.

- Work letter: less landlord spend.

Keep it lean

Push for a strong landlord work letter, standardize teller stations, and right-size security to cash volume. If the first location is a low-cash service branch, skip oversized vault gear and extra meeting space. The cleanest savings come from staying single-branch or using a branchless model until traffic justifies the space.

Staffing Readiness And Pre-Opening Payroll Startup Expense

Year 1 salary floor

For a co-operative bank, the named Year 1 salaries already total at least $565K: $180K for 1 CEO or president, $90K for 1 branch manager, $160K for 2 loan officers, and $135K for 3 tellers. One line matters most: payroll starts before loan income does.

What this covers

This startup cost covers recruiting, background checks, training, and pre-opening payroll for the CEO or president, CFO, compliance or BSA officer, lending staff, operations, and member service. Estimate it from headcount × salary, plus the months of pay needed before revenue stabilizes. The operations manager amount is incomplete, so keep it separate.

- Use signed offer letters

- Count pre-open months

- Track training time

How to trim burn

Hire in stages, not all at once. Start with roles tied to launch readiness, then add lending and service staff as opening dates firm up. Keep background checks and training scheduled close to start dates, and don’t roll this into rent, tech, or insurance. Pre-opening payroll is a separate cash bucket, not part of monthly operating expenses.

- Stage hires by launch milestone

- Avoid early idle payroll

- Keep payroll and runway separate

Runway check

Use the $565K Year 1 floor as the base staffing cash need, then add the unpaid gap for the incomplete operations manager role and any extra pre-opening months. That total should sit on top of your working capital runway so payroll doesn’t collide with compliance, rent, or loan-book ramp.

Compliance, Insurance, Audit, And Member Launch Startup Expense

Launch controls

This bucket pays for compliance setup, insurance, audit readiness, accounting setup, BSA/AML policies, vendor risk reviews, the website, and member launch outreach. Keep regulatory capital and required liquidity separate. The base model starts at $3K/month for insurance and $2K/month for professional services.

Budget inputs

Here’s the quick math: $3K + $2K

Related Products

- Co-operative Bank Porter's Five Forces Analysis

- Co-operative Bank BCG Matrix

- Co-operative Bank Business Model Canvas

- 7 Critical KPIs to Measure Co-operative Bank Performance

- Co-operative Bank Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Co-operative Bank Profitability

- How to Calculate Running Costs for a Co-operative Bank Monthly?

- Co-operative Bank Financial Model Template in Excel

- Co-Operative Bank Owner Income Using $58M-$198M NII

- Start a Cooperative Bank: 18-36+ Month US Launch Path

- How to Write a Co-operative Bank Business Plan (7 Steps)

- Co-operative Bank Marketing Mix

- Co-operative Bank Marketing Plan

- Co-operative Bank Business Proposal

- Co-operative Bank PESTEL Analysis

- Co-operative Bank Pitch Deck Example Editable PPTX

- Co-operative Bank Business SWOT Analysis

- Co-operative Bank Value Proposition Canvas

Frequently Asked Questions

No, regulatory capital is not a normal startup expense It is money the institution must hold to support risk, growth, and regulator expectations In this plan, Year 1 includes $100M in loans, $24M in other interest-earning assets, and $105M in deposit products, so capital planning sits beside the expense budget