Owner income$150k

Owner income$150kHow Much Does A Construction Company Owner Make On $113M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k  Net margin-199%

Net margin-199% Revenue for target pay$1.13M

Revenue for target pay$1.13M Business difficultyHard

Business difficultyHard

You’re trying to see what owner take-home looks like after jobs, crews, overhead, and cash needs This view separates $113M Year 3 revenue, 80% gross margin, $150k planned owner salary, profit, reserves, debt, and taxes it is not tax advice or a guaranteed earnings claim

Owner income$150kNet margin-199%Revenue for target pay$1.13MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It excludes taxes, legal structure effects, licensing costs, and guaranteed distributions.

Want to check owner income in the Construction Company model?

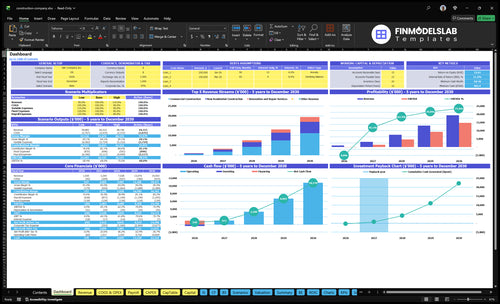

Screenshot: dashboard first; charts tie $113M revenue, 80% gross margin, $905k payroll, $85k marketing, and -$2.245M profit—open Construction Company Financial Model Template.

Owner-income model highlights

- Owner take-home scenarios

- Revenue and margin build

- Payroll, marketing, overhead

Why do construction companies have low profit margins?

Construction companies can post strong revenue and still have thin owner take-home because estimating errors, change-order leakage, material price swings, labor inefficiency, rework, warranty work, insurance, bonding, and slow collections all eat cash; if you're sizing a launch, see How Much Does It Cost To Open, Start, Launch Your Construction Company?. Even though direct listed costs fall from 24% in Year 1 to 20% in Year 3, payroll and overhead still drive a -$2,245k Year 3 operating loss. So margin quality matters more than bid volume.

Margin leaks

- Estimating errors miss real job cost.

- Change orders leak billed revenue.

- Material swings hit cash fast.

- Rework and warranty work add cost.

Cash drains

- Labor inefficiency raises payroll.

- Insurance and bonding stay fixed.

- Slow collections squeeze working cash.

- Payroll and overhead drive the loss.

How much can a construction company owner make?

A Construction Company owner can model $150,000 salary in the researched base case, but Year 3 distributions are not supported by the data. To see if that pay is durable, compare revenue pace and backlog with What Is The Current Growth Rate Of Your Construction Company?.

Owner pay range

- $150,000 planned base salary

- $0 supported Year 3 distribution

- Small owner-operated pay can start earlier

- Scale stays limited without systems

What drives upside

- Revenue above $113M, or lower overhead

- Managers, estimators, and site supervisors

- Backlog, cash flow, and gross margin

- BLS benchmark: $104,900 manager median pay

Does a construction company owner make more by scaling?

A Construction Company can pay the owner more when it scales, but not at first. An owner-operator keeps overhead low, yet that also caps project volume; a managed model adds project managers, estimators, site supervisors, admin, and business development, and that can mean $905k in Year 3 payroll plus $1.392m in fixed overhead. So the real test is simple: enough backlog and gross profit to absorb the extra layer.

Owner-operator

- Low overhead, but limited capacity

- Owner labor stays the main driver

- Fewer staff, fewer fixed costs

- Income stalls when projects stack up

Managed scale

- Adds payroll and fixed overhead fast

- $905k Year 3 payroll

- $1.392m fixed overhead

- Needs strong backlog to protect cash

Want the six main income drivers?

1

$113MProject Volume

More signed jobs and bigger contracts drive the biggest swing in owner income; at about $113M in Year 3 revenue, volume sets the ceiling.

2

80%Margin Control

Estimating accuracy protects the 80% gross margin, so small pricing misses or change-order gaps can erase owner profit fast.

3

$905KCrew Productivity

Payroll and field output decide how much job revenue turns into take-home, so $905K in payroll only works if crews keep rework and idle time low.

4

$116K/moOverhead Load

Overhead sets the burn rate, and $116K/mo means management bloat can eat profit even when jobs are moving.

5

$462KCash Buffer

Cash timing matters because the model bottoms at $462K in minimum cash and breakeven lands in Month 7, so slow pay or weak reserves can squeeze the owner.

6

45%Service Mix

Commercial share rises to 45% by Year 5, and that mix shift can lift contract size and change how much the owner earns per bid.

Construction Company Core Six Income Drivers

Project Volume And Contract Value

Project Volume and Value

Qualified projects, average contract size, and signed backlog drive owner income here. Using the stated marketing and customer acquisition cost (CAC) math, revenue rises from $1,716k in Year 1 to $113M in Year 3 and $284M in Year 5. That can raise profit fast, but only if crews, supervision, gross margin, and working capital keep up.

Here’s the quick math: more signed work lifts billings, but it also raises payroll timing pressure and material cash needs. If backlog grows faster than labor capacity or collections, the business can look strong on paper while the owner’s take-home pay stays tight. Bigger contracts help only when job pacing and cash conversion stay under control.

Track Backlog Weekly

Measure qualified leads, win rate, average contract value, and signed backlog by start date. Then compare that work to crew hours, project manager load, progress billing, and material deposits. If backlog grows but labor or cash does not, owner distributions can slip even with strong revenue.

- Forecast backlog by start month

- Match crews to signed work

- Watch collections every week

- Protect margin on rushed jobs

Test whether bigger contracts still leave room for supervision and material cash needs. If payroll hits before customer cash comes in, the company may need outside funding to keep jobs moving.

1

Gross Margin And Estimating Accuracy

Gross Margin And Bid Accuracy

If bids miss direct cost by even a few points, owner pay gets squeezed fast. Here, direct costs improve from 24% in Year 1 to 20% in Year 3, so gross margin rises from 76% to 80%. That adds about $40k of gross profit for every $1M of revenue before overhead.

Winning a bad bid hurts twice: the job loses money, and fixed overhead still has to be covered. With fixed overhead at $116k per month or $1.392M a year, estimating accuracy and disciplined markup decide whether the owner takes home pay or just keeps the lights on.

Protect Margin Before You Bid

Track estimated vs. actual direct cost on every job, by labor, subcontractor, and materials. Build bids from clean scope, then price change orders before the extra work starts. The key inputs are billed hours, hourly rates, material cost, subcontractor quotes, markup, and signed change orders. One clean rule: if the scope changes, the price changes.

- Compare bid to actual weekly

- Review margin at closeout

- Require signed change orders

- Reject work that breaks markup

A 1-point margin miss on $1M of revenue cuts gross profit by $10k, and that usually comes straight out of owner draw after payroll and overhead. Margin quality beats chasing every contract; the best jobs protect gross profit and cash.

2

Labor And Subcontractor Productivity

Labor Productivity

Labor and subcontractor productivity is how much billable work the crews actually finish versus what was estimated. With $905k in Year 3 payroll, including the $150k owner salary, idle time, weak supervision, or rework can erase gross profit fast. The key inputs are labor hours against estimate, subcontractor pricing, change requests, and schedule slippage.

Here’s the quick math: Year 3 payroll averages about $75.4k per month. If crews miss production targets, the same revenue turns into less owner pay because payroll still runs while jobs drag. Less rework means more cash left for the owner.

Track Hours, Rework, and Delay Days

Measure hours used vs. hours estimated on every job, then separate crew time from subcontractor time. Also log subcontractor change requests, punch-list rework, and project manager load so you can see where margin slips. If a job needs extra supervision, price it before the work starts, not after the bill is sent.

Use a simple weekly review: estimated hours, actual hours, rework hours, and delay days. What this estimate hides: one late trade can stall the whole schedule, and that idle time still hits payroll. Better production protects gross profit and makes the owner’s salary easier to pay from operations.

3

Overhead And Management Structure

Overhead Must Match Gross Profit

Overhead is the cost of running the shop, not building the job. Here, that means office rent, insurance, admin software, vehicles, professional services, managers, estimators, and admin staff, plus $116k per month in fixed overhead, or $1.392M a year, before marketing and payroll. If job gross profit does not cover that load, the owner’s draw gets squeezed fast.

In Year 3, adding $85k marketing and $905k payroll lifts the yearly burden to $2.382M, before direct job costs. Here’s the quick math: overhead should rise slower than gross profit. If hiring runs ahead of backlog, cash gets trapped in payroll and admin, and owner distributions disappear.

Keep Fixed Cost Tied to Backlog

Track overhead in two buckets: direct job costs and company overhead. Separate field labor, materials, and subs from the office costs above so you can see the real job margin. One clean rule: don’t add managers, estimators, or admin staff until signed work and gross profit can pay them.

- Watch overhead per month.

- Compare payroll to backlog.

- Delay hires when revenue slips.

- Review admin cost by function.

If collections slow or contract wins soften, trim fixed spending first. That keeps gross profit available for owner pay instead of feeding a bigger cost base.

4

Cash Flow And Reserves

Cash Flow and Reserves

Accounting profit is not the same as cash the owner can take home. In construction, progress payments, retainage, accounts receivable, upfront material buys, payroll timing, and equipment loans can trap cash even on profitable jobs. With $905k of Year 3 payroll, including the $150k owner salary, a slow collection cycle can shut off distributions fast.

The key metric is working capital, not book profit. The source data gives no tax, debt, or reserve percentage, so do not assume a draw is safe until cash has cleared and near-term obligations are covered. One late-paying client can force outside funding even when the job margin looks fine.

Protect Owner Cash

Build a weekly cash forecast that tracks billed work, expected collections, retainage release dates, payroll, materials, and loan payments. Here’s the quick math: owner cash only exists after collections pay direct costs, fixed overhead, and a reserve buffer. If the forecast goes negative, delay owner draws before the bank balance does.

- Track billed versus collected cash.

- Age retainage by job. < li>Map payroll dates to receipts.

- Watch material prepayments closely.

- Hold cash before owner distributions.

If collections slow while payroll runs, use the forecast to cap new work, renegotiate progress billing, or secure outside funding early. That keeps profitable projects from turning into a cash squeeze that blocks owner pay.

5

Service Mix And Market Positioning

Service Mix And Market Positioning

Service mix is the split of work across new residential, commercial, and renovation jobs. In Year 3, the mix is 36% new residential, 40% commercial, and 24% repair; by Year 5 it shifts to 45% commercial, 35% residential, and 20% repair. That mix changes price power, job risk, and how fast cash comes in, so it directly affects gross profit and owner pay.

Commercial work can bring larger contracts, but it often comes with tighter terms, more supervision, and slower collections. Repair work can be faster to start and finish, but it can be lumpier and harder to schedule. No niche is automatically best; the better mix is the one that matches local demand, licensing, repeat clients, contract terms, margin, capacity, and risk control.

Track Mix By Margin, Not Just Revenue

Measure each segment by gross margin, days to collect, change orders, and rework, not just sales. A mix that looks busy can still squeeze cash if commercial jobs tie up labor and receivables while repair jobs fill gaps with lower ticket size. The key question is simple: which mix leaves the most cash after labor, materials, and supervision?

Build the forecast by segment: expected win rate, average contract value, billing terms, and crew load. Then test whether a higher commercial share, like the move from 40% to 45%, improves profit without overloading project managers or slowing collections. Keep the mix flexible, and drop work types that hurt margin or stretch cash too long.

- Track margin by job type.

- Watch collections by contract type.

- Limit low-margin, slow-pay work.

- Match crews to job complexity.

6

Compare owner income across lean, base, and mature cases

Owner income scenarios

Early owner cash can cover salary, but true upside depends on margin, staffing, and cash kept for reserves. Later EBITDA is strong, yet distributions still need debt and tax inputs.

| Scenario | Low CaseSalary only | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | This case assumes the owner mainly takes salary, with little or no extra draw. | This case assumes the model runs through Year 3 with no clear owner draw beyond pay. | This case assumes the business reaches the mature Year 5 path and can start to pay the owner beyond salary. |

| Typical setup | Year 1 keeps the leanest setup: $1,716k revenue, 76% gross margin, $25k marketing, $1,392k fixed overhead, and a $150k planned salary. | Year 3 shows $11.3M revenue, 80% gross margin, $905k payroll, and a reported -$2,245k operating profit, so owner income stays constrained. | Year 5 reaches $284M revenue and 84% gross margin, but final distributions still depend on complete staffing, reserves, debt, and taxes. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $150k salary onlyLow draw | No supported drawDraw constrained | Salary plus distributionsUpside only |

| Best fit | Use this when the business is still proving demand and cash is tight. | Use this as the most realistic operating case before reserves and debt service are set. | Use this to test strong growth, but don't book owner cash until the full capital stack is set. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Construction Company Porter's Five Forces Analysis

- Construction Company BCG Matrix

- Construction Company Business Model Canvas

- 7 Critical KPIs to Measure for Construction Company Success

- Construction Company Business Plan Template in Pre-Written Word

- Increase Construction Company Profitability: 7 Strategies for Higher Margins

- How to Calculate Monthly Running Costs for a Construction Company

- How Much It Costs To Start A Construction Company: $345K CAPEX

- Construction Company Financial Model Template in Excel

- How to Start a Construction Company: Month 1 Readiness Roadmap

- How to Write a Construction Company Business Plan in 7 Steps

- Construction Company Marketing Mix

- Construction Company Marketing Plan

- Construction Company Business Proposal

- Construction Company PESTEL Analysis

- Construction Company Pitch Deck Example Editable PPTX

- Construction Company Business SWOT Analysis

- Construction Company Value Proposition Canvas

Frequently Asked Questions

The researched plan includes a $150,000 CEO/founder salary In Year 3, the company reaches about $113M revenue and 80% gross margin, but payroll, marketing, and fixed overhead create about a -$2245k operating loss So the salary may need funding unless revenue, margin, or staffing efficiency improves