Owner income$180K

Owner income$180KHow Much Disaster Recovery Service Owners Make at 705% Margin

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180K  Net margin-43%

Net margin-43% Revenue for target pay$256K

Revenue for target pay$256K Business difficultyHard

Business difficultyHard

On these researched assumptions, a disaster recovery service owner can plan around $0 to $180K before tax in the early ramp-up, but the full $180K founder payroll is not fully funded by first-year EBITDA Here’s the quick math: about 100 acquired clients produce roughly $132M in revenue, 705% direct margin, and about -$79K EBITDA after payroll, marketing, and fixed overhead At 200 active clients, revenue rises to about $324M, direct margin improves to 728%, and EBITDA after founder payroll is about $872K before reserves, taxes, debt service, and reinvestment Actual take-home depends on pricing, utilization, emergency demand, retention, and the owner’s compensation choices

Owner income$180KNet margin-43%Revenue for target pay$256KBusiness difficultyHardWant to estimate your disaster recovery owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, reserves, debt, churn, and operating discipline.

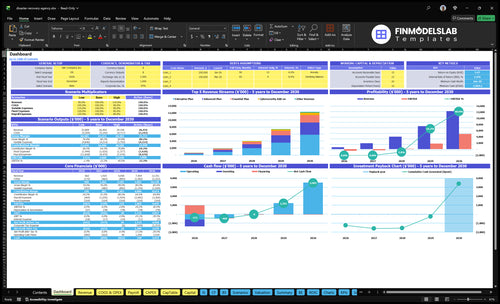

How do you check owner income in the Disaster Recovery Service forecast?

This dashboard in the Disaster Recovery Service Financial Model Template shows revenue, margin, costs, reserves, and owner pay assumptions—open the model.

Owner-income model highlights

- Owner pay capacity

- 100-client and 200-client cases

- MRR, EBITDA, margin charts

How many disaster recovery clients do I need to make $100K?

You need about 100 active clients for a Disaster Recovery Service to support roughly $100K owner pay before tax, based on Year 1 economics; the main number to watch is explained here: What Is The Most Critical Indicator Of Disaster Recovery Service Performance?. Here’s the quick math: $1,102.75 monthly revenue per client × 70.5% direct margin × 12 = about $9,329 annual contribution per client.

Client Target

- 100 clients supports about $100K owner pay

- $9,329 contribution per client per year

- $831.5K covers payroll, fixed costs, marketing

- $931.5K total need with owner pay

Pay Sensitivity

- $180K founder payroll needs about 109 clients

- Reserve funding is not included

- Downtime can cost businesses millions per hour

- Subscription revenue must stay recurring

What costs reduce disaster recovery business owner income?

In Disaster Recovery Service, owner income gets squeezed first by technical payroll, cloud infrastructure, software licensing, support labor, marketing, insurance, and 24/7 readiness; if you’re sizing startup spend, see How Much Does It Cost To Open And Launch A Disaster Recovery Service Business?. The model shows Year 1 direct costs at 295% of revenue — 180% cloud, 80% software, and 35% support — so EBITDA gets hit before any owner distribution.

Direct cost pressure

- Cloud runs at 180% of revenue.

- Software runs at 80% of revenue.

- Support labor runs at 35% of revenue.

- Payroll is $4475K in Year 1.

Fixed cost drag

- Fixed overhead is $27K per month.

- Insurance is $35K.

- Legal and professional services are $4K.

- Marketing is $240K.

Can a disaster recovery owner-operator make more than a team-based agency?

Yes — a technical owner-operator can keep more cash early, but only by replacing paid labor with their own time. In Disaster Recovery Service, that means carrying a $140K Lead Technical Engineer in Year 1 and $180K CEO/founder payroll; cutting staff can improve short-term cash, but it also reduces capacity, response coverage, and documentation quality.

Early cash edge

- Own labor can replace hires early

- $140K engineer payroll sits in Year 1

- $180K founder payroll also stays in play

- Short-term cash improves, not capacity

Scaling tradeoff

- More revenue needs more payroll

- More scale raises management load

- Insurance and reserves also rise

- Higher revenue does not mean higher take-home

Want to see the six biggest income drivers?

1

$110K MRRRecurring Base

100 Year 1 clients create the monthly base, so renewals matter more than one-off wins.

2

$4.5MPayroll Load

The technical and support team is the biggest cash drag, so each hire has to pay for itself fast.

3

70.5%Service Mix

A better split toward higher-rate plans and add-ons pushes gross margin up, and that drops straight to take-home.

4

2.5-10hTechnician Load

Enterprise work carries more billable hours per client, so utilization lifts revenue without the same jump in overhead.

5

26%-18%Cloud Costs

Cloud and software costs fall from 26% to 18% of revenue, so cost control widens EBITDA as volume grows.

6

$2.4KCAC

At $2,400 CAC, the $240K launch budget buys about 100 clients, so cheaper acquisition shortens payback.

Disaster Recovery Service Core Six Income Drivers

Recurring contract base

Recurring contract base

A retained client base turns disaster recovery from one-off work into monthly recurring revenue (MRR). With 100 clients at about $1,102.75 per client, Year 1 MRR is about $110,275; that cash is what stabilizes owner pay. The catch is acquisition cost: at $2,400 CAC, churn has to stay low enough for each client to repay that spend.

Scope drives margin. Monitoring, recovery testing, planning, and service-level coverage all cost time, and not every client uses the same support level. If pricing does not match workload, the recurring base still looks big, but profit and take-home pay get thinner fast.

Price the work inside the contract

Track retained clients, MRR per client, churn, and payback on $2,400 CAC. Then split revenue by service tier so you can see which accounts cover monitoring, testing, planning, and response time. One clean rule: if a client needs more coverage, the price should move before the margin does.

- Watch monthly retained clients.

- Test add-on attach rate.

- Price higher for strict SLAs.

- Review margin by account.

Use the contract base to fund owner pay only after delivery costs are covered. If high-touch clients pile up, cash flow can look steady while labor drag rises, so the fix is tighter scope, better renewal terms, and fewer underpriced accounts.

1

Emergency recovery project pricing

Emergency Recovery Pricing

Urgent outage, cyberattack, and data restoration work can push revenue up fast, but only when you price for after-hours labor, senior engineer time, subcontractors, and liability risk. This line is usually lumpy, so treat it as an upside revenue bucket, not base payroll support. If response pricing is too low, the job adds stress without lifting owner pay.

The model does not give emergency project counts, so the key question is whether each incident clears the cost of standby capacity and recovery labor. A useful floor is the model’s premium hourly service range of $350/hour to $450/hour, which should cover higher-pressure work better than standard support pricing.

Price the risk, not just the hours

Build each quote from billable hours, data complexity, subcontractor pass-throughs, and a risk load for liability exposure. Here’s the quick math: if a job needs senior staff, overnight coverage, and outside help, the rate has to cover all three before it helps gross profit or owner draw.

- Track incident count by month.

- Separate labor, tools, and pass-throughs.

- Set a standby reserve.

- Use a higher after-hours floor.

What this estimate hides: demand is uneven, so cash flow can swing hard month to month. If emergency work starts to crowd out recurring clients or forces too much overtime, margin falls even when revenue rises.

2

Service mix and gross margin

Service Mix and Gross Margin

Here’s the quick math: at 70.5% blended direct margin in Year 1, every $100 of revenue leaves $70.50 before overhead. By Year 2, margin improves to 72.8%, so the same $100 leaves $72.80. That extra 2.3 points flows straight into owner pay if cloud and software costs stay in line.

The mix includes managed retainers, testing, consulting, backup storage, cybersecurity add-ons, and compliance reporting. Inputs that matter are client count, add-on attach rates, cloud and software spend, and labor hours on incidents. Labor-heavy recovery work can push margin down fast, even when revenue looks strong.

Measure Margin by Service Line

Track gross profit by service type, not just at the company level. Watch the margin on retainers, add-ons, and incident work separately, since cybersecurity adoption rises from 150% to 400% in the model and compliance reporting rises from 80% to 300%. If those add-ons bring more support labor, reprice them.

Use a short quote checklist before work starts: engineer hours, subcontractors, after-hours pay, re-test time, and reporting time. If a recovery job needs extra labor, the price should move too. That keeps cash flow cleaner and makes the owner’s draw depend on true gross profit, not busy hours.

- Track margin by service line.

- Reprice labor-heavy incidents fast.

- Test add-on attach rates monthly.

- Watch cloud and software spend.

3

Technician utilization

Technician Utilization

When technicians are underused, payroll sets the ceiling on owner take-home. This model starts with one $140K Lead Technical Engineer in Year 1 and scales to five by Year 5, so scheduling, documentation, automation, and escalation design decide how much revenue each engineer supports. Owner time matters too: if the owner is handling escalations, that is still an economic cost, even when it is not booked as payroll.

Keep Engineers Busy on Paid Work

Track billable hours, recovery tests, and support tickets per technician, then compare them to recurring revenue and service coverage. A $140K engineer is about $11.7K per month before payroll taxes and benefits, so weak utilization turns growth into labor drag fast. Use runbooks, automation, and clear escalation rules to push repeat work down the stack and free senior time for high-value tasks.

- Measure billable load by engineer.

- Document repeat recovery steps.

- Automate backup checks and alerts.

- Route simple issues away fast.

4

Cloud and software cost control

Cloud and software cost control

If cloud and software licensing run ahead of revenue, owner pay gets squeezed fast. In the model, cloud costs start at 180% of revenue and ease to 120% by Year 5; software runs from 80% to 60%. That means infrastructure can absorb more than the full top line, so price increases only help if usage and license counts stay tight.

Control the bill before it controls pay

Track storage volume, retention periods, replication frequency, test environments, and platform licensing every month. Here’s the quick math: longer retention, more copies, and idle test systems raise cost before cash comes in. Price those settings into each tier, then review whether each client still leaves enough cash for owner draw.

- Match retention to service tier.

- Delete idle test environments.

- Cut unused licenses monthly.

- Set replication by SLA.

5

Client segment and SLA complexity

Enterprise SLA Pricing

Clients with strict uptime, compliance, audit, and recovery-time targets can pay more, so this segment lifts revenue per hour. In this model, Enterprise Plan pricing starts at $350/hour for 800 billable hours and reaches $450/hour at 1,000 hours by Year 5. The upside is real, but each tighter service-level agreement adds delivery risk.

What this driver includes is simple: uptime promises, recovery-time objective (RTO), compliance reporting, audit trails, and response speed. If the fee does not cover documentation, insurance, staffing depth, and liability exposure, owner pay gets squeezed even when sales rise.

Price the Risk, Not Just the Hours

Track revenue per client by SLA tier, plus the extra labor tied to reporting and testing. The big check is whether higher-touch accounts still cover senior engineer time, standby coverage, and insurance. If not, the contract is underpriced.

Use compliance reporting adoption as a pricing trigger: it rises from 80% to 300% in the model, and that work should be billed into the rate before renewal. One clean rule helps here: if the SLA is tighter, the margin must be wider.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income changes fast here because client volume, plan mix, CAC, payroll, and fixed overhead do not move together. The three cases show how founder take-home shifts as the service scales.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower-earnings path with modest client count and a thin cash cushion. | This is the modeled path with steady client growth and a workable owner payout. | This is the stronger earnings path with faster scaling and better CAC efficiency. |

| Typical setup | The model holds near 100 clients and about $132M revenue, with 705% direct margin, $4,475K payroll, $240K marketing, and about $324K fixed overhead. | The model reaches about 200 clients and about $324M revenue, with 728% direct margin, $740K payroll, and $420K marketing before reserves. | The model reaches 358 clients from Year 3 CAC math, about $733M revenue, and 750% direct margin as the team scales capacity. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$79KLow Case Range | $872KBase Case Range | $342MHigh Case Range |

| Best fit | Use this to stress-test founder pay when growth is slow and reserves stay tight. | Use this as the main planning case for staffing, pricing, and owner draw. | Use this to test upside when sales efficiency holds and delivery capacity keeps up. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Disaster Recovery Service Porter's Five Forces Analysis

- Disaster Recovery Service BCG Matrix

- Disaster Recovery Service Business Model Canvas

- 7 Critical KPIs to Track for Disaster Recovery Service

- Disaster Recovery Service Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Disaster Recovery Service Profitability

- Monthly Running Costs for a Disaster Recovery Service Startup

- How Much Does It Cost To Start A Disaster Recovery Service? $420K+ CAPEX

- Disaster Recovery Financial Model Template in Excel

- How To Open A Disaster Recovery Service In 60–120 Days

- How to Write a Disaster Recovery Service Business Plan

- Disaster Recovery Service Marketing Mix

- Disaster Recovery Service Marketing Plan

- Disaster Recovery Service Business Proposal

- Disaster Recovery Service PESTEL Analysis

- Disaster Recovery Service Pitch Deck Example Editable PPTX

- Disaster Recovery Service Business SWOT Analysis

- Disaster Recovery Service Value Proposition Canvas

Frequently Asked Questions

In the researched model, Year 1 includes $180K founder payroll, but EBITDA is about -$79K after payroll, marketing, and overhead That means extra distributions are not funded early At 200 clients, EBITDA after founder payroll is about $872K before reserves, taxes, debt service, and reinvestment