Owner income$180K+

Owner income$180K+How Much Eyewear Manufacturing Owners Make at $301M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180K+  Net margin55.5%–85.7%

Net margin55.5%–85.7% Revenue for target pay~$750K

Revenue for target pay~$750K Business difficultyHard

Business difficultyHard

Key Takeaways

- Product mix changes margin and cash timing.

- Gross margin depends on keeping COGS below sales.

- High utilization spreads fixed costs across more units.

- Cash reserves must fund inventory and receivables.

Owner income$180K+Net margin55.5%–85.7%Revenue for target pay~$750KBusiness difficultyHardWant to test your eyewear owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This output is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

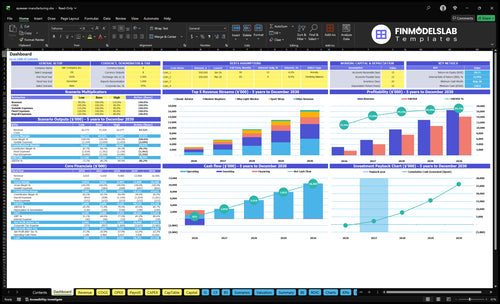

Want to see the eyewear income forecast?

The dashboard in the Eyewear Manufacturing Financial Model Template shows revenue, units, margin, costs, payroll, and owner take-home—open it.

Owner-income model highlights

- Owner pay is planned

- Revenue and margin trend

- Scenarios test capacity limits

What is the eyewear manufacturing profit margin?

For Eyewear Manufacturing, gross margin is not owner take-home. In Year 1, gross margin is 839% on $301M revenue and $4,851K product COGS; by Year 5, it rises to 850% on $165M revenue and $2,484M product COGS. For launch context, see How Much Does It Cost To Open And Launch Your Eyewear Manufacturing Business?

Gross margin math

- Year 1: 839% gross margin

- Year 5: 850% gross margin

- Based on product COGS only

- Not owner cash in hand

Cash reality

- Year 1: 764% contribution margin

- Year 5: about 800% contribution

- COGS includes frames and lenses

- Owner draws come after overhead

How much does an eyewear manufacturing business owner make?

An Eyewear Manufacturing owner makes a planned $180,000 founder salary in this model, plus possible distributions if cash remains after taxes, debt, inventory, staff, equipment, and reserves; see What Is The Current Growth Trajectory Of Your Eyewear Manufacturing Business? for the operating view behind those numbers. Year 1 shows 15,000 units, $3.01M revenue, about $2.525M gross profit, and roughly $1.73M pre-tax profit after fixed costs and visible payroll, including the founder salary.

Owner Pay

- $180,000 planned founder salary

- $1.73M Year 1 pre-tax profit

- 57.5% pre-tax margin on revenue

- Distributions depend on remaining cash

Scale Case

- 75,000 units by Year 5

- $16.5M Year 5 revenue

- $12.62M Year 5 pre-tax profit

- Taxes and reinvestment reduce take-home

How much revenue does an eyewear manufacturing business need to pay the owner?

Eyewear Manufacturing needs about $750K in revenue to pay the owner under the Year 1 model. At a $200.67 weighted ASP, that’s roughly 3,735 units; the real floor is higher once you add taxes, debt service, capex, inventory buffers, and extra production staff.

Core pay math

- 764% contribution margin

- $2.724M fixed expenses

- $120K Head of Design salary

- $180K founder salary

What the estimate leaves out

- No taxes or debt service

- No capex or inventory buffers

- No added production staff

- Revenue target stays model-based

Want the six main eyewear income drivers?

1

$3.01M-$16.5MMix & Channel

Premium styles and direct sales push revenue from $3.01M in year 1 to $16.5M in year 5, so owner take-home moves fastest here.

2

84%-85%Gross Margin

With gross margin near 84%-85%, every point of price or material control drops straight into owner income.

3

15K-75KCapacity Use

Running closer to full capacity spreads rent and payroll across more pairs, which improves cash and raises profit per unit.

4

15K-75KOrder Volume

Units grow from 15K to 75K, so higher order flow lifts earnings, but concentration in a few buyers can still swing take-home.

5

$1.00M-$1.24MOperating Costs

Fixed load rises from about $1.00M to $1.24M a year, and the $180K founder salary sits inside that pressure on profit.

6

$328KCash Reserve

Minimum cash of $328K in month 8 means weak reserves can force outside funding before payback arrives.

Eyewear Manufacturing Core Six Income Drivers

Product And Channel Mix

Product and Channel Mix

The mix between private label, OEM, wholesale, and owned-brand sales changes both margin and cash timing. Year 1 prices run from $100 for Kids Durable to $250 for Modern Wayfarer, so sticker price alone does not tell you what the owner can actually pull out.

Here’s the quick math: Classic Aviator brings $110M of revenue and Modern Wayfarer $100M, while Sport Wrap, Blue Light Blocker, and Kids Durable add only $360K, $450K, and $100K. A higher retail price does not guarantee higher owner cash if fulfillment, commissions, returns, or inventory rise.

Track cash by channel

Model each channel with ASP (average selling price), fees, shipping, and payment timing. That is what drives cash available for owner draws, not the tag on the frame.

- Track ASP by product line.

- Separate fees and shipping.

- Watch returns and inventory.

- Map collection timing to cash.

If wholesale grows faster than direct sales, a late receivable can squeeze distributions even when revenue looks strong on paper.

1

Gross Margin And Unit Economics

Gross Margin And Unit Economics

When you sell eyewear, gross margin is the first real income gate. The model shows $4,851K of product COGS on $301M of revenue, which is 1.61% of sales; that math implies a 98.39% gross margin before overhead. That only works if unit costs stay tight across frame materials, lenses, labor, packaging, and freight.

Here’s the quick math: raw frames run $5 to $12, lenses $4 to $9, direct labor $3 to $550, packaging $1 to $2, and inbound freight $0.50 to $1. Add 40% of revenue for factory overhead, quality control, supervision, maintenance, and utilities, and defects or rework can eat owner cash fast, even if reported sales look strong.

Track Unit Cost Per Pair

Measure gross margin by product line, not just companywide. Track material cost per pair, labor per pair, scrap and rework rate, and the full overhead load per unit, then compare that to selling price and channel fees. If one style needs expensive labor or has high defect rates, it can look busy but still weaken owner pay.

Watch the inputs that move cash: order mix, yield, overtime, and inventory build. A small jump in defects means more labor, more freight, and more rework on the same pair, so the owner gets less free cash to draw. One bad batch can erase the margin from several good ones.

- Track cost per pair weekly

- Separate direct labor from overhead

- Measure defect and rework rates

- Review margin by style and channel

- Hold freight and packaging to plan

2

Capacity Utilization

Capacity Utilization

Capacity utilization is how much of the factory’s installed output you actually use. In this model, planned production rises from 15,000 units in Year 1 to 75,000 units in Year 5, while fixed expenses stay at $227K per month or $2,724K per year. That means fixed cost per unit falls from about $181.60 to $36.32 if quality stays steady.

Here’s the quick math: more units spread the same factory cost over more sales, so owner profit improves even if price stays flat. But idle machines, setup delays, small batches, overtime, and rework can wipe out that gain. If output per labor hour drops or late-order penalties rise, take-home pay shrinks even while revenue grows.

Track output, yield, and delay cost

Measure units per labor hour, batch yield, downtime, and late shipments every week. Those inputs tell you whether higher volume is turning into real margin or just busier machines. If you add overtime to cover weak scheduling, the fixed-cost benefit gets diluted fast, so compare planned units, actual units, and scrap before paying out profit.

Set a simple rule: raise production only when yield and on-time delivery hold. Track the gap between planned output and shipped output, then tie manager pay to utilization and late-order penalties. That keeps more of the $2.724M annual fixed base working for owner income instead of being lost to rework and delays.

3

Order Volume And Customer Concentration

Order Volume and Customer Concentration

When volume rises from 15,000 units in Year 1 to 45,000 in Year 3 and 75,000 in Year 5, planning gets easier and factory use gets steadier. Bigger repeat accounts can smooth frame runs, labor, and material buys, but they can also push for lower prices, longer terms, or custom packaging. So unit count helps income, but only if margin and terms hold.

The cash risk is simple: one large wholesale buyer that pays late can tie up receivables and block owner distributions, even when sales look strong. Here’s the quick rule: connect every big account to payment timing, not just booked revenue, and use minimum order quantities to protect setup time and material purchases.

Track Each Large Account’s Cash Impact

Model each major account with units, average selling price, payment terms, and any custom packaging or setup cost. If a buyer wants net 60 instead of net 30, cash stays out of the bank for an extra month. Protect margin with minimum order quantities and price floors when repeat volume rises.

- Track top-customer share monthly.

- Watch receivables by due date.

- Test minimum order quantities.

- Price custom packaging separately.

Keep large accounts below the level where one slow payer can strain payroll, material buys, or owner draws. If volume grows but collections slip, profit on paper won’t turn into cash in the bank.

4

Operating Costs

Operating Overhead

Owner pay is only dependable after the business clears $227K per month in fixed costs, or $2.724M per year. That stack includes $15K rent, $25K utilities, $1K insurance, $800 software, $12K professional services, $15K marketing platform fees, and $700 security, plus visible payroll of $180K for the founder and $120K for the Head of Design.

As unit volume rises, quality assurance, regulatory work, production management, and sales administration need to be watched closely. If those jobs grow faster than volume, overhead eats cash and owner draws get pushed out. One clean rule: fixed overhead must be covered before profit can turn into reliable pay.

Track Overhead Every Month

Build the monthly model from unit volume, selling price, payroll, rent, utilities, software, professional fees, marketing tools, and security. Then compare total overhead to gross profit dollars, not just revenue. If overhead stays at $227K while sales slip, the business can look busy and still leave nothing for the owner.

Set a review on the four rising cost centers: QA, regulatory, production management, and sales admin. Tie each role to shipped units, defect rate, and order flow, so headcount grows with workload, not with hope. T hat keeps the monthly burn flat enough for owner pay to start showing up.

5

Working Capital Reserves

Working Capital Reserves

Profit is not cash. In eyewear manufacturing, cash gets tied up in frame materials, lenses, packaging, finished goods, receivables, tooling, and maintenance parts. Even with strong first-year pre-tax profit after visible payroll of about $173M, owner distributions should wait until those operating needs are funded.

As revenue reaches $165M in Year 5, cash pressure rises because more units mean more inventory and slower cash conversion. The key inputs are units produced, collection timing, supplier terms, and growth inventory. If cash is short, the business can look profitable and still miss owner pay, purchases, or payroll.

Hold Cash Before Paying the Owner

Track inventory on hand, receivables aging, and supplier credit every month. Put a reserve rule between accounting profit and owner draws so cash stays inside the business until the next round of materials, packaging, and overhead is covered.

Use a 13-week cash forecast and test slow collections against growth buys. If finished goods build up or customers pay late, cut distributions first. That protects factory cash and keeps owner income tied to real cash, not paper profit.

6

Compare lean, base, and high-scale owner income scenarios

Owner income scenarios

Owner income moves with unit volume, product mix, and pricing, while payroll and factory overhead set the floor. These scenarios show how the model scales from launch year to mature year.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path built on launch-year output and the founder still covering the core payroll load. | This is the modeled middle path where Year 3 scale supports stronger earnings and steadier plant use. | This is the stronger earnings path tied to Year 5 scale and the best spread of fixed costs. |

| Typical setup | Year 1 volume is 15,000 units across five styles, about $3.01M revenue, roughly 84% gross margin, and a $180K founder salary. | Year 3 volume reaches 45,000 units, revenue is about $9.47M, gross margin stays near 84%, and payroll is more fully spread. | Year 5 volume reaches 75,000 units, revenue is about $16.5M, gross margin is near 85%, and payroll is used at full capacity. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.67M - $1.73MLow Case | $6.85M - $7.53MBase Case | $12.62M - $14.14MHigh Case |

| Best fit | Use this to stress-test launch year cash and overhead. | Use this as the main operating plan for a scaled but still manageable business. | Use this to test upside if demand holds and production runs near full load. |

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Eyewear Manufacturing Porter's Five Forces Analysis

- Eyewear Manufacturing BCG Matrix

- Eyewear Manufacturing Business Model Canvas

- 7 Critical KPIs to Track for Eyewear Manufacturing

- Eyewear Manufacturing Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Eyewear Manufacturing Profitability

- How to Run an Eyewear Manufacturing Business Monthly Costs

- Eyewear Manufacturing Startup Costs for a 15,000-Unit Year 1 Launch

- Eyewear Manufacturing Financial Model Template in Excel

- How to Open an Eyewear Manufacturing Business in 6–12 Months

- How to Write an Eyewear Manufacturing Business Plan in 7 Steps

- Eyewear Manufacturing Marketing Mix

- Eyewear Manufacturing Marketing Plan

- Eyewear Manufacturing Business Proposal

- Eyewear Manufacturing PESTEL Analysis

- Eyewear Manufacturing Pitch Deck Example Editable PPTX

- Eyewear Manufacturing Business SWOT Analysis

- Eyewear Manufacturing Value Proposition Canvas

Frequently Asked Questions

The model includes a $180,000 annual founder salary from launch month through the full model period In Year 1, revenue is $301M on 15,000 units, with about $173M pre-tax profit after visible payroll Actual take-home depends on taxes, debt, reserves, inventory, and whether the company approves distributions