Owner income$0 → $2.3M

Owner income$0 → $2.3MHow Much Does A Fitness Center Owner Make? Year 5 EBITDA $23M

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0 → $2.3M  Net margin-21% → 42%

Net margin-21% → 42% Revenue for target pay$98K/mo

Revenue for target pay$98K/mo Business difficultyHard

Business difficultyHard

Key Takeaways

- 1,047 active members cover fixed costs.

- Average revenue per member rises from $124 to $185.

- Payroll is the biggest controllable cost after revenue.

- Weak retention delays break-even and raises acquisition spend.

Owner income$0 → $2.3MNet margin-21% → 42%Revenue for target pay$98K/moBusiness difficultyHardWant to test your own gym owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This output is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

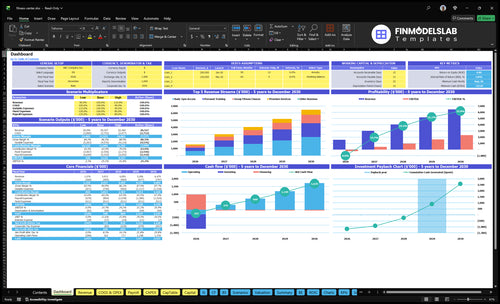

Want to see the forecast flow in the Fitness Center model?

This screenshot ties assumptions to owner-income outputs. Open the Fitness Center Financial Model Template for the forecast flow.

Owner-income model highlights

- Revenue, mix, payroll, capex

- Fixed costs, cash flow

- Scenarios and valuation dashboard

- EBITDA: -$246K, $443K, $978K

- EBITDA peaks: $1,620M, $2,329M

- Month 8 cash: -$314K

- Month 9 breakeven; 41-month payback

What is a typical fitness center profit margin?

If you’re pricing out a How Much Does It Cost To Open A Fitness Center?, the margin answer depends on which layer you mean: gross margin is high, but operating profit can be negative early on. In this model, Year 1 EBITDA margin is about -21%, then it improves to 18% in Year 2 and 42% in Year 5.

Core margins

- 16.5% direct COGS in Year 1

- 83.5% gross margin before overhead

- 65% Year 1 contribution margin

- 72.6% Year 5 contribution margin

Profit after costs

- -21% EBITDA margin in Year 1

- 18% EBITDA margin in Year 2

- 42% EBITDA margin in Year 5

- Owner payouts come after reserves, debt, and taxes

How much do fitness center owners make per year?

Fitness Center owners may make $0 in Year 1 under this model because EBITDA, profit before debt and taxes, is -$246K; see What Is The Key To Success For Your Fitness Center? for the KPIs that drive that swing. By Year 2, EBITDA reaches $443K, then $978K in Year 3, $1.620M in Year 4, and $2.329M in Year 5 before debt, taxes, reserves, and owner distributions.

Owner Take-Home

- Year 1: likely $0 take-home

- Year 2: $443K EBITDA pool

- Year 3: $978K EBITDA pool

- Revenue is not owner income

Key Assumptions

- $85K general manager from Month 1

- Owner-operated saves payroll

- Owner time replaces paid labor

- Distributions come after reserves

How many members does a fitness center need to be profitable?

A Fitness Center needs about 1,047 active paying members to break even, using $124 in first-year monthly revenue per member, a 65% contribution margin, and about $84,350 in monthly payroll plus fixed costs. Here’s the quick math: $84,350 ÷ 65% ÷ $124 ≈ 1,047, so profit depends on filling the membership base fast enough; the model says break-even lands in Month 9.

Break-even math

- $124 monthly revenue per member

- 65% contribution margin

- $84,350 monthly fixed load

- 1,047 members to break even

What to watch

- Break-even lands in Month 9

- Owner pay should wait for growth

- Member count must keep rising

- Slower signup means cash burn risk

Want the six drivers that move owner income?

1

HighActive Members

More paying members lift every revenue stream, so this is the biggest lever on owner income.

2

68%Retention

Group class participation rises to 68% by Year 5, and that kind of engagement helps keep members longer.

3

$124Revenue Per Member

Year 1 revenue per active member is $124, so better mix in classes, training, and premium services raises take-home fast.

4

$501KPayroll Load

Year 1 payroll totals $501K, so staffing levels and the owner's direct role move EBITDA fast.

5

$43K/moFixed Overhead

Facility rent, utilities, and support costs run about $43K a month, so the break-even floor stays high.

6

$85 CACCAC Control

With $85 CAC and a $180K Year 1 marketing budget, acquisition only pays if members stay long enough.

Fitness Center Core Six Income Drivers

Active Paying Members And Retention

Active Paying Members

Owner pay starts only after fixed costs are covered, so the real metric is active paying members, not leads or followers. Using $124 average revenue per member and a 65% contribution margin, the first-year break-even is about 1,047 active paying members. One clean rule: more paid members mean more cash, but only if retention holds.

Churn rate must be user-entered because no churn rate is provided. If retention weakens, the club needs more paid acquisition to replace lost members, which delays Month 9 breakeven and cuts the cash left for owner draw. Here’s the quick math: membership growth helps income only when recurring revenue stays ahead of churn and fixed overhead.

Track Retention, Not Vanity Metrics

Measure active paying members, monthly churn, and net adds each month. Keep the forecast tied to paid members only, since a big follower count does not pay rent or payroll. If churn rises, the same revenue target needs more new sales, more ad spend, and longer payback on each member.

- Track paid members by cohort.

- Enter churn as a model input.

- Watch Month 9 breakeven closely.

Retention work should focus on onboarding, class attendance, and trainer touchpoints, because each kept member protects recurring margin. If a member stays one more month, the business keeps the $124 monthly revenue and the 65% contribution that helps fund owner pay after fixed costs clear.

1

Average Revenue Per Member

Average Revenue Per Member

Average revenue per member is the monthly revenue mix from basic access, group classes, personal training, and premium services. In this model, it is about $124 per member per month in Year 1 and rises to about $185 by Year 5, mainly from price and mix changes. That lifts revenue faster than facility costs, so owner pay can improve if retention stays strong.

Here’s the quick math: if members buy more personal training, priced at $149 in Year 1 and $175 in Year 5, revenue per head rises without adding the same rent or equipment cost. The catch is simple: higher pricing only works if the value is clear and the local market will pay for it.

Track Mix, Price, and Upgrade Rate

Measure monthly revenue per member by service line, not just total dues. Track how many members buy basic access only, how many add classes, and how many use personal training or premium services. A small shift in mix can move cash flow fast, because add-ons raise revenue without the same facility cost increase.

Test price changes against retention and local demand. If personal training moves from $149 to $175 but upgrades stall, take-home income can fall from weaker renewal. The right test is simple: higher ARPM, stable churn, and better monthly profit after payroll and fixed costs.

2

Payroll And Owner Role

Payroll And Owner Role

Payroll is the biggest controllable cost after revenue, so it hits owner pay fast. Modeled payroll is $501K in Year 1, $722K in Year 2, and $1.172M in Year 5 across the general manager, trainers, group instructors, front desk, maintenance, marketing, nutrition, and assistant manager roles.

If the owner covers the $85K general manager salary, cash payroll drops, but workload rises and short-term take-home can still fall if sales, retention, or hiring slip. This is a trade between saving salary now and buying back time for growth later.

Track Hours, Not Just Headcount

Measure payroll as a share of revenue and by role, not as one lump sum. Use member count, class volume, trainer hours, front desk coverage, and marketing output to set staffing. The goal is enough labor to keep members active without paying for empty hours.

- Track payroll by role each month.

- Test owner GM coverage vs. hiring.

- Watch churn if service slips.

- Link labor to active member demand.

Test the owner-versus-GM choice against three numbers: $85K salary saved, hours the owner gives up, and any change in retention or add-on sales. If the owner’s time is best used on sales or retention, payroll can support higher profit; if not, lean staffing protects take-home.

3

Facility And Equipment Fixed Costs

Facility and Equipment Fixed Costs

$426K per month in fixed operating costs sets the floor before owner pay shows up. That includes $28K rent, $45K utilities, $32K insurance, and $22K cleaning, so the lease and building choice hit profit every month, even when member sales soften.

The equipment side also matters to cash flow. Startup capex is $935K, with $180K for cardio, $220K for strength, and $120K for the recovery zone. If equipment maintenance runs at 85% of revenue in Year 1, there is very little left to cover fixed costs, debt service, or owner draw.

Trim the Cost Floor

Measure facility cost per member, per square foot, and per month. Here’s the quick math: if rent, utilities, insurance, and cleaning stay fixed, the only fast way to improve owner income is to raise revenue density or shrink the space and service load. Location and facility size are not just startup choices; they change the monthly break-even line.

Track rent, utility load, insurance, cleaning, and equipment maintenance as a % of revenue every month. If maintenance stays anywhere near 85% of revenue, pause new purchases, review service contracts, and match equipment mix to actual use so cash stays available for profit and owner pay.

4

Capacity Utilization And Scheduling

Capacity Utilization

Better use of space lifts revenue without matching cost growth. Here, the key inputs are active members, billable hours, class fill, and personal training attach rate. In this model, average billable hours per active customer rise from 12 per month in Year 1 to 18 in Year 5, while group fitness participation grows from 45% to 68% and personal training from 25% to 38%.

That mix pushes more dollars through the same floor space, so revenue per square foot improves faster than rent or utilities. The risk is crowding: if peak hours feel packed or classes run over capacity, member experience slips and retention can drop, which cuts the very income this driver is supposed to create.

Track Utilization, Not Just Headcount

Measure the room, not just the roster. Track billable hours per active customer, class fill rate, personal training attach rate, and revenue per square foot. Use a simp le check: monthly revenue ÷ usable square feet. If that number rises while service quality holds, owner take-home has room to grow without a big jump in fixed cost.

- Watch peak-hour occupancy.

- Stagger classes and equipment use.

- Cap class size before crowding.

- Shift trainers to busy windows.

- Test equipment mix by demand.

Small schedule changes matter most when they move demand away from the same busy hour. If the floor stays smooth at peak times, add-on sales from classes and training can rise faster than payroll and occupancy cost.

5

Acquisition Cost And Churn Economics

Acquisition Cost And Churn Economics

Customer acquisition cost (CAC) and churn decide how much of each member dollar reaches owner pay after growth spend. With a $180K marketing budget and $85 CAC, the plan buys about 2,118 customers in Year 1. By Year 5, $340K at $65 CAC buys about 5,231 customers, before churn cuts the real gain.

Here’s the quick math: lower CAC and lower churn improve payback, so more revenue turns into cash instead of ad waste. Marketing expense falling from 125% to 85% of revenue helps, but only if referrals, trials, partnerships, and retention hold members long enough to recover the first-month spend. If churn spikes, owner income drops fast.

Track CAC, churn, and payback together

Measure CAC by channel, not as one blended number. Split ads, referrals, partnerships, and trials, then compare each to first 90-day revenue and retention. A cheap lead that cancels quickly is still expensive, because it delays break-even and trims the owner’s draw.

Watch the ratio of marketing spend to revenue every month. If spend rises faster than active-member growth, tighten the offer, improve onboarding, and push referral loops. One clean target: keep payback tight enough that new members start covering their acquisition cost before churn eats the cash.

- Track CAC by channel monthly

- Measure 90-day retention by cohort

- Test referrals and trial offers

- Cut spend on slow payback channels

6

Compare lean, base, and strong fitness center income scenarios

Owner income scenarios

Owner income swings with ramp speed, payroll, and how much cash the business keeps in reserve. Early losses can leave take-home near zero even after sales improve.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | Year 1 is a loss case, so owner take-home is likely $0 while the business funds growth. | Year 2 turns profitable, but owner pay is still a cautious draw after reserve and debt needs. | Year 5 supports a stronger owner draw, but tax and reserve planning still cap what comes out. |

| Typical setup | Year 1 runs about -$246K EBITDA on roughly $98K monthly revenue and a -21% margin, with about $501K payroll, $511K fixed costs, and a $180K marketing budget. | Year 2 reaches about $443K EBITDA on roughly $207K monthly revenue and an 18% margin, with payroll near $722K and marketing at $220K. | Year 5 reaches about $2.329M EBITDA on roughly $461K monthly revenue and a 42% margin, with payroll near $1.172M and marketing at $340K. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No owner take-homeNo draw | Modest owner take-homeCareful draw | Strong owner take-homeUpside draw |

| Best fit | Use this to stress-test the launch year if occupancy grows slowly or spend runs ahead of sales. | Use this for a steady Year 2 path with positive EBITDA but cash still protected for reserves. | Use this to test a mature year with strong member mix and room for a larger owner draw. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Fitness Center Porter's Five Forces Analysis

- Fitness Center BCG Matrix

- Fitness Center Business Model Canvas

- 7 Critical KPIs to Scale Your Fitness Center

- Fitness Center Business Plan Template in Pre-Written Word

- How to Increase Fitness Center Profitability in 7 Practical Strategies

- Analyzing Monthly Running Costs for a Sustainable Fitness Center

- How Much Does It Cost To Open A Fitness Center? $935K CAPEX Guide

- Fitness Center Financial Model Template in Excel

- How To Open A Fitness Center In 4 To 9 Months: Launch Roadmap

- How to Write a Fitness Center Business Plan: 7 Steps

- Fitness Center Marketing Mix

- Fitness Center Marketing Plan

- Fitness Center Business Proposal

- Fitness Center PESTEL Analysis

- Fitness Center Pitch Deck Example Editable PPTX

- Fitness Center Business SWOT Analysis

- Fitness Center Value Proposition Canvas

Frequently Asked Questions

A fitness center owner may take $0 in the first year if the site follows this ramp, because Year 1 EBITDA is -$246K The same model shows $443K of EBITDA in Year 2 and $2329M in Year 5 That is profit capacity before debt service, taxes, reserves, and owner distributions