Owner income$327k-$787k

Owner income$327k-$787kHow Much Indoor Playground Owners Make: $327k Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$327k-$787k  Net margin33%-45%

Net margin33%-45% Revenue for target pay$987k-$1.74M

Revenue for target pay$987k-$1.74M Business difficultyHard

Business difficultyHard

You’re sizing owner income before you sign a lease, hire staff, and buy play equipment In this five-year US toddler indoor playground model, Year 1 revenue is $987k and EBITDA is $327k, before personal taxes, debt service, reserves, and owner distributions

Owner income$327k-$787kNet margin33%-45%Revenue for target pay$987k-$1.74MBusiness difficultyHardWant to test your indoor playground income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on real traffic, pricing, payroll, taxes, debt, and reinvestment needs.

Want to see the Indoor Playground forecast?

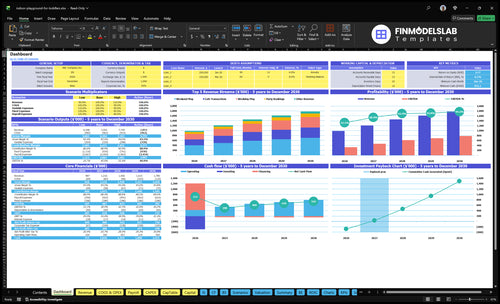

Open the Indoor Playground Financial Model Template for the dashboard, revenue forecast, expense assumptions, payroll schedule, startup costs, cash flow, EBITDA, and owner income scenarios. It shows a five-year model, $651k minimum cash need in Month 6, a 24-month payback, and EBITDA growth from $327k to $787k.

Owner-income model highlights

- Owner income scenarios

- Revenue and EBITDA

- Five-year assumptions

How many kids does an indoor playground need to make money?

Indoor Playground doesn’t need a universal kid count to make money; it needs enough paid visits, parties, and cafe sales to cover fixed costs. In the Year 1 base case, that means 35,000 paid play visits, or about 673 visits a week, plus 150 party bookings, 30,000 cafe transactions, and $22,000 in extra income. At $15 weekday tickets and $20 weekend tickets, the real break-even point comes down to capacity, staffing, and rent.

Year 1 math

- 35,000 paid visits

- About 673 visits weekly

- 150 party bookings

- 30,000 cafe transactions

What drives break-even

- $15 weekday ticket

- $20 weekend ticket

- $22,000 extra income

- Year 5: 57,000 visits and 250 parties

Can an indoor playground run without the owner?

An Indoor Playground can run without the owner if you hire management, but it is not passive unless payroll and controls are funded from day one. The model includes a General Manager at $70,000 and an Assistant Manager at $55,000 starting in Month 1, and total payroll is $308,000 in Year 1, or about $25,667 per month. If the owner runs it, take-home can improve by replacing some management labor, but owner hours go up fast.

Hired management

- $70,000 GM starts Month 1

- $55,000 Assistant Manager starts Month 1

- Payroll totals $308,000 in Year 1

- Needs reporting, cash, and safety controls

Owner-operated

- Can raise take-home by cutting labor

- Owner hours rise, so it is not passive

- Cash checks must stay tight

- Service standards need daily review

Can an indoor playground owner pay themselves in the first year?

Yes, an Indoor Playground owner can pay themselves in Year 1 if cash flow allows it, but owner pay should stay behind startup cash, reserves, debt service, taxes, and reinvestment. In the model, Year 1 EBITDA is $327k on $987k revenue, with $495k startup capex, a $651k minimum cash need in Month 6, Month 1 breakeven, and 24-month payback; track the operating driver here: What Is The Most Important Metric To Measure The Success Of Indoor Playground?

Owner Pay Signal

- $327k Year 1 EBITDA

- $987k Year 1 revenue

- Month 1 model breakeven

- 24-month payback period

Cash Guardrails

- $495k startup capex

- $651k Month 6 cash need

- Pay after reserves are funded

- Debt and taxes reduce distributions

Want to see what drives indoor playground profit?

1

$625KAdmissions

Year 1 has 35K visits, so small gains in weekday or weekend traffic flow straight into revenue.

2

$308KStaffing

Payroll starts at $308K a year, so tighter scheduling and FTE control can protect take-home cash.

3

$120KRent

Commercial rent is $10K a month, so this fixed cost sets the floor for monthly profit.

4

$75KParties

150 bookings at $500 each add high-margin sales and use the same space already staffed for play.

5

$265KAncillary Sales

Cafe revenue of $240K plus merch at $25K lifts ticket size without needing much more traffic.

6

UpsideMemberships

Memberships are not in base revenue, but repeat passes can smooth visits and add recurring cash.

Indoor Playground Core Six Income Drivers

Paid Admissions

Paid Admissions

Admissions are the main traffic lever, so small shifts in visits or ticket price move owner income fast. The model shows 15k weekday visits at $15 and 20k weekend visits at $20, or about $625k in Year 1 admissions revenue. A $1 change across 35k annual visits changes revenue by $35k.

That upside only helps if the floor can handle it. Peak-hour crowding can force more cleaning and play supervision, which cuts margin. Year 1 fixed costs are $186k and payroll is $308k, so admission volume has to stay strong without pushing labor higher than the extra cash it brings in.

Track Visits by Time Slot

Track weekday vs. weekend visits, hour by hour, and tie it to capacity, cleaning, and staff coverage. Here’s the quick math: 35k visits at the disclosed prices equal $625k in Year 1, and the model scales to 57k visits by Year 5, so traffic growth is the biggest revenue driver.

Test price moves in small steps and watch conversion, wait times, and reviews. If more visitors slow check-in or crowd the play area, the extra revenue can get eaten by overtime and service issues. The goal is simple: keep admissions high enough to cover fixed costs and still leave room for owner draw.

1

Birthday Parties And Private Events

Birthday Party Revenue

Birthday parties are a high-ticket add-on, but they only work if weekend room, staff, and cleanup slots are open. Year 1 revenue is $75k from 150 bookings at $500; by Year 5 it reaches $140k from 250 bookings at $560. That revenue lifts cash and owner pay above admission-only sales, but extra bookings can also raise labor and turnover costs.

Here’s the quick math: more parties mean more dollars per family, yet margin depends on supplies, labor, deposits, add-ons, and turnover time. If a party blocks a room too long or needs extra cleanup, the added booking can crowd out another sale. The real limit is not demand alone; it’s how many profitable time slots the venue can actually serve.

Protect Party Margin

Track bookings, average price, add-on spend, cleanup minutes, and staff hours per event. Those are the inputs that show whether party revenue is growing profit or just filling the calendar. A simple test: if more bookings push overtime or delay the next event, revenue rises but take-home income can stall.

Use tighter slot rules, clear deposit terms, and separate pricing for extras so each event covers its own labor and cleanup. The goal is not just more parties; it’s more profitable parties. One clean number to watch: party revenue per weekend hour.

- Count bookings per weekend.

- Measure event labor hours.

- Track cleanup and reset time.

- Separate base price from add-ons.

2

Memberships And Repeat Visits

Memberships And Repeat Visits

Memberships are a cash-flow tool, not just a discount. In this model, they should support the paid visits line, not replace it. The win is better weekday traffic and more repeat visits, which helps cover fixed costs like rent, payroll, and cleaning without waiting on party bookings.

The risk is simple: unlimited passes can crowd peak times and lower revenue per visit. If member use cuts into full-price weekend demand, owner income drops even when foot traffic looks strong. The key inputs are member visits, churn, acquisition cost, and weekend capacity.

Control Member Use

Price memberships against capacity, not against hope. Here’s the quick math: if a pass fills slow weekdays but protects weekend seats, it can smooth cash flow and improve take-home pay. If it pulls heavy use into busy hours, it can crowd out higher-value visits and raise staff pressure.

Track these numbers every month:

- Member visits by daypart

- Weekend capacity used

- Churn and renewals

- Acquisition cost per member

What this hides: members only help if overuse stays controlled. If onboarding is easy and weekday visits rise, cash gets steadier. If peak-time use rises faster than staffing or space, profit per visit falls and owner pay gets tighter.

3

Staffing And Owner Labor

Labor and Owner Pay

Payroll is a major take-home lever because it is the biggest controllable cost tied to daily service. Year 1 payroll is $308k, including $70k for the General Manager and $55k for the Assistant Manager, plus play supervisors, cafe staff, front desk, and cleaners. If owner coverage replaces paid hours, margin improves; if staffing slips, safety, cleanliness, and party quality can drop fast.

At Year 1 revenue of $987k across admissions, parties, cafe, merch, and extras, payroll is about 31% of sales ($308k / $987k). The key inputs are open hours, visit volume, party blocks, cafe rushes, and cleaning turns. Year 5 staffing should rise with volume; under-staffing can hurt reviews and repeat visits.

Staff to the Rush

Track labor by daypart, not just by month. Watch labor dollars per visit, overtime, owner hours, and coverage for peak admissions, parties, and cleanups. That lets you cut idle time without starving the floor.

Set staffing rules for busy days so the owner is not the default backup every weekend. If the room looks tired, cleaning lags, or party turns run late, the payroll savings can get wiped out by weak reviews and slower repeat visits.

4

Rent And Facility Costs

Fixed Lease Burden

This is the cash drag that hits before traffic proves out. The model shows $10k/month rent, plus $15k/month utilities, $850 insurance, $12k marketing, $750 maintenance, and permits, accounting, and software, for $186k in Year 1 fixed costs. One soft weekday does not lower rent, so weak traffic cuts owner pay fast.

The key input is total fixed overhead versus conservative visits. If admissions, parties, and cafe spend do not cover this base, profit drops before the owner can take a draw. Lease discipline matters here: a too-big space or long lease can keep the business busy but still starve the owner’s take-home income.

Track Break-Even Lease Load

Measure monthly fixed cost against weekday traffic, not just weekend peaks. Here’s the quick math: the business must cover $186k a year before owner pay starts to feel safe, so every extra dollar of rent or fac ility cost has to be funded by more paid visits, parties, or cafe sales.

- Rent and lease term

- Utilities by month

- Insurance and permits

- Marketing spend pace

- Maintenance and software

If weekday traffic stays soft, renegotiate space, shorten the lease, or delay any fixed-cost add-ons. That keeps more cash in the month and protects the owner’s income when demand is uneven.

5

Ancillary Sales

Ancillary Sales

Ancillary sales include the cafe, merchandise, vending, arcade, and sponsorships. In Year 1, they total $287k: $240k cafe sales from 30k transactions at $8, plus $25k merchandise and $22k extra income. That raises spend per visit, but the owner only keeps what is left after direct costs and staffing.

The margin mix matters. Cafe inventory runs at 50% in Year 1, while merchandise inventory is 20%, so waste and slow stock can erase cash fast. By Year 5, cafe revenue reaches $4,224k and extra income reaches $40k, but take-home income still depends on how much of each dollar survives product, licensing, and operating complexity.

Protect basket size and waste

Track ancillary sales by line: cafe ticket, merchandise sales, and other income. The main inputs are visits, average order value, merch attach rate, and sponsorship or arcade yield. If transactions stay at 30k but basket size rises from $8, owner cash improves without needing more foot traffic or more play capacity.

Control the cost side hard. Watch food waste, shrink, and labor tied to cafe service, since a 50% inventory ratio leaves little room for mistakes. Keep separate margin reports for each stream, and drop any add-on that needs more staff, licensing, or cleanup than it earns.

- Track revenue per visit weekly.

- Separate cafe and merch margins.

- Test add-ons before scaling.

6

Compare low, base, and high indoor playground income scenarios

Owner income scenarios

Traffic and party volume drive owner income here because rent and core staffing stay fixed. Lower visits cut earnings fast, while stronger weekends and cafe sales lift EBITDA.

| Scenario | Low CaseTraffic risk | Base CaseModelled base | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the downside case, where weaker traffic and party demand push owner income below the base plan. | This is the modeled operating case, where steady traffic and party demand support solid owner income. | This is the stronger earnings path, where higher traffic and more bookings push owner income toward the Year 5 model. |

| Typical setup | Weekday visits, weekend visits, parties, and cafe transactions all run lighter, but rent and core staffing stay mostly fixed, so margin gets squeezed. | Year 1 revenue is about $987k, EBITDA is $327k, about a 33% margin, with 35k visits, 150 parties, $308k payroll, and $186k fixed costs. | Year 5 revenue is about $1.78m, EBITDA is $787k, about a 44% margin, with 57k visits, 250 parties, stronger cafe sales, and more extra income. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Below base EBITDAReserve pressure | $327k EBITDAPlanning anchor | $787k EBITDAGrowth upside |

| Best fit | Use this to stress-test cash reserve needs if traffic or bookings come in below plan. | Use this as the core budget case for staffing, pricing, and cash planning. | Use this to test upside if traffic holds, bookings scale, and extra income streams stay strong. |

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions.

Related Products

- Indoor Playground Porter's Five Forces Analysis

- Indoor Playground BCG Matrix

- Indoor Playground Business Model Canvas

- Tracking 7 Core KPIs for Your Indoor Playground Business

- Indoor Playground Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Indoor Playground Profitability Now

- How Much Does It Cost To Run An Indoor Playground Monthly?

- Indoor Playground Startup Costs: $651k Funding Plan

- Indoor Playground Financial Model Template in Excel

- Start An Indoor Playground: 4-9 Month US Launch Roadmap

- How to Write a Business Plan in 7 Simple Steps

- Indoor Playground Marketing Mix

- Indoor Playground Marketing Plan

- Indoor Playground Business Proposal

- Indoor Playground PESTEL Analysis

- Indoor Playground Pitch Deck Example Editable PPTX

- Indoor Playground Business SWOT Analysis

- Indoor Playground Value Proposition Canvas

Frequently Asked Questions

In the researched base case, the business produces $327k EBITDA in Year 1 and $787k by Year 5 That is operating profit before personal taxes, debt service, reserves, and owner distributions Revenue grows from $987k to $178m over the same period, so owner income depends on how much cash the business can safely distribute