Owner incomeUp to $13.5M

Owner incomeUp to $13.5MHow Much Indoor Rowing Studio Owners Make: $0 To $335K Modeled

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeUp to $13.5M  Net margin-417% to 390%

Net margin-417% to 390% Revenue for target pay$71.7k/mo

Revenue for target pay$71.7k/mo Business difficultyHard

Business difficultyHard

An indoor rowing studio owner can make very little in the first year if payroll and rent outrun the membership base, but a mature studio can produce meaningful owner take-home Using the researched assumptions, revenue grows from $268,200/year in Year 1 to $860,400/year in Year 5 Modeled operating profit is about -$111,900 in Year 1, $149,300 in Year 3, and $335,200 in Year 5 before taxes, debt service, reserves, and owner distributions The biggest swing factors are active members, class utilization, pricing, instructor payroll, rent, and debt or lease obligations

Owner incomeUp to $13.5MNet margin-417% to 390%Revenue for target pay$71.7k/moBusiness difficultyHardWhat could your rowing studio pay you?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not a guaranteed salary, tax advice, or owner distribution advice. Actual owner income will move with sales, staffing, taxes, debt, and reinvestment needs.

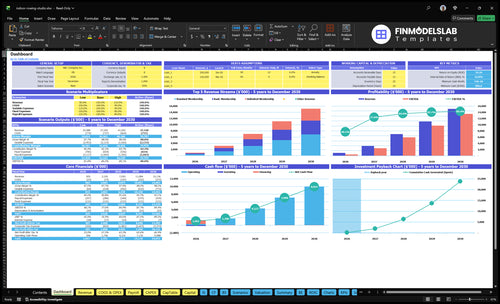

Want to test the Indoor Rowing Studio financial model?

Open the dashboard tab in the Indoor Rowing Studio Financial Model Template to check monthly revenue, EBITDA, cash, payback, and owner income.

Owner-income model highlights

- Payback: 9 months

- Listed capex: $228,000

- ROE: 342%

How does the owner’s role change rowing studio income?

An owner-operated Indoor Rowing Studio can save cash if the founder handles management or teaches classes, but that money does not disappear — it turns into unpaid founder work. Here’s the quick math: the model already includes a $60,000 studio manager and a $50,000 lead instructor, so that is $110,000 before part-time instructors, front desk staff, and cleaning staff. Manager-run studios need payroll coverage before owner distributions, and absentee ownership is not passive because retention, instructor quality, utilization, and local marketing still need daily oversight.

Owner-run cash effect

- Owner labor can cut payroll spend.

- Founder time replaces paid management.

- Teaching classes adds unpaid workload.

- Cash improves, but effort rises fast.

What still needs oversight

- Protect class retention every week.

- Keep instructor quality tight.

- Watch spot utilization closely.

- Run local marketing in person.

What indoor rowing studio operating costs reduce owner income most?

Payroll is the biggest drag on owner income in an Indoor Rowing Studio, with Year 1 wages of $222,500 rising to $335,000 by Year 5. If you're sizing startup costs, see How Much Does It Cost To Open An Indoor Rowing Studio? — rent at $8,000/month and fixed overhead of $10,900/month hit before wages, while variable costs start at 100% of revenue because of 50% digital marketing and 25% card processing.

Biggest cost pressure

- Payroll hits income hardest.

- Year 1 wages: $222,500.

- Year 5 wages: $335,000.

- Rent: $8,000/month.

Cash flow strain

- Fixed overhead: $10,900/month.

- Variable costs start at 100% of revenue.

- Digital marketing: 50%; card fees: 25%.

- Capex: $228,000 reduces distributions.

How much revenue does an indoor rowing studio need to pay the owner?

An Indoor Rowing Studio should work backward from owner pay, not hope. To net $100,000 of before-tax owner pay, it needs about $408,000 in annual revenue at the Year 3 modeled operating margin of 245%, or about $256,000 at the Year 5 modeled margin of 390%.

Revenue needed

- $100,000 owner pay target

- $408,000 revenue at 245%

- $256,000 revenue at 390%

- Higher margin means less revenue needed

What pay depends on

- Payroll comes off revenue first

- Then rent and marketing

- Then maintenance and reserves

- Then financing obligations

Want to see the main income drivers?

1

150-420Active Members

Going from 150 to 420 active members is the biggest revenue jump, because recurring dues flow in with little extra floor space.

2

45%-82%Class Utilization

Higher occupancy fills more rowing slots, so fixed labor and rent get spread across more paid classes.

3

$99-$220Pricing Mix

Shifting the mix toward Standard and Unlimited lifts monthly revenue per member without adding more machines.

4

$223K-$335KInstructor Payroll

Staff pay is the largest cost swing, so extra FTEs can erase margin fast if demand softens.

5

$10.9K/moFacility Costs

This fixed monthly base hits cash every month, so tight rent and overhead control protect take-home profit.

6

5%-3%Retention & Ads

Keeping members longer cuts paid acquisition needs, and marketing spend drops from 5% to 3% of revenue.

Indoor Rowing Studio Core Six Income Drivers

Active Paying Members

Active Paying Members

Active paying members set the studio’s base cash flow. In this model, members grow from 150 in Year 1 to 420 in Year 5, and membership revenue rises from $21,350/month to $68,200/month. That is the income line that pays rent, payroll, and owner draws before retail or extras.

Here’s the quick math: Year 1 revenue is about $142 per active member per month ($21,350 ÷ 150), and Year 5 is about $162 per member per month ($68,200 ÷ 420). The risk is simple: every lost recurring member cuts predictable cash, so owner income gets less stable fast if cancellations outrun new paid sign-ups.

Track Paid Retention, Not Interest

Measure active paid members, monthly churn, and reactivation, not followers, inquiries, or free trials. A waitlist helps, but only paid members cover fixed costs. If one member is worth roughly $142 to $162 per month, even a small drop in retention can erase a large share of owner take-home before you see it in the bank.

Track three inputs: new paid joins, cancellations, and average revenue per member. Use a simple rule in forecasting: if active members fall by 10, monthly recurring revenue drops by about $1,400 to $1,600. That makes staffing, marketing, and owner pay harder to protect, so retention should sit at the center of the plan.

Count only paid active members.

Watch monthly churn and reactivations.

Forecast owner pay from recurring revenue.

Use waitlists to replace lost members.

1

Class Utilization And Capacity

Class Utilization

Utilization is how much of your class capacity you sell. In this model, it rises from 450% in Year 1 to 820% in Year 5, so each instructor hour and facility hour earns more without the same jump in fixed cost. Fuller classes pay the fixed bill. Empty seats still leave you with instructor pay, rent, utilities, software, and cleaning.

Watch spots offered, spots filled, and fill rate by morning, lunch, and evening. Waitlists matter because they show where demand is real, but they only help if you turn them into added sessions or tighter schedules.

Fill peak slots first

Track revenue per instructor hour and revenue per facility hour for each class time. If a session stays light, move it, shrink it, or cut it fast. Add more classes only where the waitlist stays full and the peak slots keep selling.

- Booked spots vs capacity

- Waitlist by time slot

- Instructor hours per class

- Facility cost per hour

Weak classes still burn cash, so better scheduling can raise owner take-home even if total memberships stay flat.

2

Pricing And Package Mix

Pricing And Package Mix

When your tiers are priced right, each member brings in more cash without adding more class load. In Year 5, the mix of 125 basic at $110, 190 standard at $165, and 105 unlimited at $220 produces about $68,200/month, or roughly $162 per member. That recurring revenue is what pays payroll, rent, and the owner draw.

Here’s the quick math: 125 x 110 + 190 x 165 + 105 x 220 = $68,200. Private sessions and retail can add upside, but the recurring tiers still carry the plan. If pricing is above local demand, sign-ups slow and retention slips; if it’s too low, you fill classes but leave margin on the table.

Track Mix Before You Raise Rates

Watch member mix, not just headcount. Track how many members sit in each tier, how often they attend, and whether higher-priced members stay longer. Price changes should match schedule depth and local demand, because unlimited tiers only work when members can use them without crowding out the core class base.

- Track revenue per active member monthly.

- Test price by tier, not across all plans.

- Check retention after each price move.

- Use waitlists to spot upgrade demand.

One clean rule: if the schedule is thin, don’t push unlimited too hard. Weak access can hurt retention, while over-discounting basic plans can cap owner income even when classes look full.

3

Instructor Payroll And Staffing

Instructor Payroll

Instructor payroll is the labor line that can eat owner income before rent does. Year 1 payroll is $222,500, or about $18,542/month, split across a $60,000 manager, $50,000 lead instructor, $70,000 part-time instructors, $30,000 front desk, and $12,500 cleaning. By Year 5, payroll reaches $335,000 a year, so cash pressure rises fast even if sales hold steady.

Owner-taught classes can save cash, but that saving only helps if the hours are sustainable. If the owner replaces paid staff with too many classes, the studio may protect margin for a while but lose quality, energy, and retention. What this estimate hides is payroll taxes, benefits, and overtime, which would make the real load even heavier.

Track payroll by class hour

Measure payroll against classes taught, attendance per class, and paid hours by role. The key inputs are instructor hours, manager coverage, front desk shifts, and cleaning load. If a slot runs light, cut the shift before adding more staff. If the owner is teaching more to save cash, cap those hours so fatigue does not turn into weaker coaching and churn.

- Track weekly payroll by role.

- Compare pay to filled class hours.

- Use owner hours as a cap.

- Staff peak slots first.

Here’s the quick math: every $10,000 of payroll saved is $10,000 more room for owner pay or reserves, but only if class quality stays high. If the studio needs repeated owner coverage to hold margins, that is a warning sign, not a long-term fix.

4

Rent, Facility, And Equipment Burden

Fixed Facility Burden

When rent is $8,000 and utilities are $1,200 a month, the studio starts with $10,900/month of fixed overhead before wages. That means owner pay only starts after the class schedule covers rent, utilities, and the rest of the fixed base. If membership revenue is around $21,350/month, facility overhead alone consumes about 51% of sales.

The setup bill also ties up cash: $205,000 for rowing machines, buildout, locker rooms, and sound/AV. That does not improve monthly margin, but it raises the member level needed before owner distributions make sense. One clean rule: high fixed costs make the break-e ven floor hard to miss.

Track Break-Even Before Draws

Build the forecast from paid members, monthly rent, utilities, and other fixed overhead. Track those costs separately from class revenue so you can see when the studio covers its base before any owner draw. The real question is simple: does recurring revenue stay above the fixed monthly burn?

- Watch rent and utilities monthly.

- Separate fixed and variable costs.

- Delay draws until cash stays positive.

If membership growth stalls, the same $10,900 base hits fewer members and squeezes profit fast. Use that pressure to tighten class fill and keep enough recurring members to cover fixed costs before paying yourself.

5

Retention And Marketing Efficiency

Retention And Marketing Efficiency

Retention protects owner take-home better than launch promotions. In this model, digital marketing starts at 50% of revenue and falls to 30% by Year 5, so every retained member cuts the cost of replacing lost revenue. Since churn is not provided, the model should test member loss, trial conversion, and referral growth against monthly membership income.

Here’s the quick math: if card fees ease from 25% to 21%, margin improves a bit, but paid ads still matter more. Strong retention keeps recurring cash steadier, lowers pressure on ad spend, and gives the owner a better shot at a reliable draw.

Track churn, trials, and referrals

Measure active members, churn by tier, trial-to-paid conversion, referral share, and paid marketing as a % of revenue. If retention slips, replacement cost rises fast, and the studio ends up buying growth instead of collecting it from repeat members.

- Test churn by membership tier.

- Track trial conversion by source.

- Watch ad spend as revenue share.

- Push referrals from retained members.

If onboarding takes 14+ days or early class use drops, churn risk rises and marketing efficiency weakens. That shows up first in higher ad spend, then in tighter cash flow, then in a smaller owner draw.

6

Compare lean, base, and high-performing rowing studio income scenarios

Owner income scenarios

Owner income swings with class fill, member count, and staffing load. Higher occupancy spreads payroll and rent across more revenue, while weak fill leaves the studio in the red.

| Scenario | Low CaseLean case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | This model assumes Year 1 traffic, 150 members, 45% occupancy, and about $22,350 a month in revenue. | This model assumes Year 3 scale with steadier classes and a middle-of-the-road profit path. | This model assumes Year 5 scale with fuller classes and a stronger profit path. |

| Typical setup | The studio runs with early-stage staffing, 100% variable costs, and $222,500 of payroll, so owner income stays negative. | The studio reaches 315 members, 70% occupancy, and about $50,730 a month in revenue with roughly 84% variable costs. | The studio reaches 420 members, 82% occupancy, and about $71,700 a month in revenue with roughly 69% variable costs. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | ($111,900)Downside range | $149,300Base range | $335,200Upside range |

| Best fit | Use this to stress-test early cash flow if demand starts slow. | Use this as the planning case for budgeting and lender talks. | Use this to test upside if membership growth and fill rates hold. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; they are before taxes, reserves, debt service, and owner payouts.

Related Products

- Indoor Rowing Studio Porter's Five Forces Analysis

- Indoor Rowing Studio BCG Matrix

- Indoor Rowing Studio Business Model Canvas

- 7 Critical KPIs to Scale Your Indoor Rowing Studio

- Indoor Rowing Studio Business Plan Template in Pre-Written Word

- How to Increase Indoor Rowing Studio Profitability by 7 Focused Strategies

- How Much Does It Cost To Run An Indoor Rowing Studio Monthly?

- Indoor Rowing Studio Startup Costs: $228K Buildout and Gear

- Indoor Rowing Studio Financial Model Template in Excel

- How to Open an Indoor Rowing Studio: 7-Month Launch Roadmap

- Writing an Indoor Rowing Studio Business Plan: 7 Actionable Steps

- Indoor Rowing Studio Marketing Mix

- Indoor Rowing Studio Marketing Plan

- Indoor Rowing Studio Business Proposal

- Indoor Rowing Studio PESTEL Analysis

- Indoor Rowing Studio Pitch Deck Example Editable PPTX

- Indoor Rowing Studio Business SWOT Analysis

- Indoor Rowing Studio Value Proposition Canvas

Frequently Asked Questions

In this model, first-year owner take-home is likely $0 because operating profit is negative Revenue is $268,200 in Year 1 against $222,500 payroll and $130,800 fixed overhead By Year 5, modeled operating profit reaches about $335,200 before taxes, debt service, reserves, and owner distributions