Owner income$150k-$233k

Owner income$150k-$233kHow Much Mediation Consulting Owners Make: $150k Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k-$233k  Net margin72%

Net margin72% Revenue for target pay$424.7k

Revenue for target pay$424.7k Business difficultyHard

Business difficultyHard

A mediation consulting owner can plan on $150,000 in founder salary in this model, plus any distributions the business can safely afford after reserves and reinvestment EBITDA is $83,000 in Year 1, then rises to $604,000 in Year 2 and $4697 million by Year 5 under the researched assumptions Year 1 gross margin after delivery costs is 85%, based on 5% online dispute resolution software and 10% external mediator fees These are planning assumptions, not guaranteed earnings or tax advice

Owner income$150k-$233kNet margin72%Revenue for target pay$424.7kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the gap to target pay from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will move with cases, fees, contractor mix, overhead, and reserves.

Want to pressure-test the Mediation and Negotiation Consulting model?

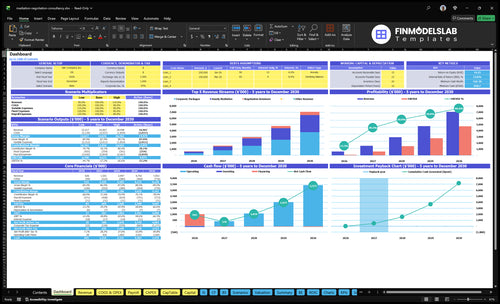

Yes—this dashboard shows revenue, gross margin, EBITDA, cash, breakeven, and owner income; open the Mediation and Negotiation Consulting Financial Model Template next.

Model highlights

- Month 6 breakeven

- $839,000 minimum cash

- 14-month payback

- EBITDA: $83k to $4.697M

- Scenario tabs cover pricing

- Also tests staffing and reserves

What affects mediation consulting profit margin?

Mediation and Negotiation Consulting margin comes down to mediator fees, online dispute resolution software, marketing, and the case mix; Year 1 delivery costs are 15% and variable costs are 13%, so contribution is 72% before fixed overhead and payroll. For startup spend, see How Much Does It Cost To Open And Launch Your Mediation And Negotiation Consulting Business? Fixed overhead is $5,900 per month, and the marketing budget rises from $25,000 in Year 1 to $100,000 in Year 5 while CAC improves from $500 to $350.

Main margin levers

- External mediator fees hit margin first

- ODR software lowers delivery cost

- Case mix changes hourly yield

- Travel and admin support add drag

Cost pressure points

- Insurance and office costs are fixed

- Marketing must keep lead flow strong

- Lower overhead only helps with quality

- $5,900 monthly fixed overhead still matters

How much does a mediation consulting business owner make?

A Mediation and Negotiation Consulting owner can model $150,000 in salary, plus profit distributions if cash remains after taxes, reserves, and reinvestment; What Is The Most Critical Indicator For The Success Of Your Mediation And Negotiation Consulting Business? explains the KPI behind that upside. EBITDA, or profit before interest, taxes, depreciation, and amortization, is $83,000 in Year 1, $604,000 in Year 2, and $4.697 million in Year 5.

Owner Pay

- Start with $150,000 founder salary

- Add distributions only after reserves

- Use profit, not employee wage data

- Solo model caps at billable capacity

Profit Levers

- Senior mediators expand capacity

- Junior mediators support delivery

- Contractors raise volume faster

- External fees cut margin 10% Year 1

How much revenue does a mediation consulting business need to pay the owner?

Mediation and Negotiation Consulting needs about $424,700 in Year 1 revenue to pay a $150,000 owner salary, $85,000 of other payroll, and $70,800 of fixed overhead. That math assumes a 72% contribution margin after 15% delivery costs and 13% variable costs, so every $1 of revenue leaves $0.72 before fixed costs. Owner distributions are separate from salary, and they are not the same as tax treatment.

Year 1 math

- $150,000 founder salary

- $85,000 other payroll

- $70,800 fixed overhead

- $424,700 revenue target

Cost drivers

- 15% delivery costs

- 13% variable costs

- 72% contribution margin

- Distributions are separate from salary

Want the six owner-income levers?

1

$1.8K/caseBillable Volume

Each extra case adds about $1.8K gross profit at a $2,085 fee and 85% gross margin, so volume is the main income lift.

2

$2.1KAverage Fee

A higher average fee pushes revenue per matter up, and the Year 1 blend already lands near $2,085 per engagement.

3

70/20/10Service Mix

The current mix of hourly work, packages, and retainers shapes cash flow, and more packaged work usually improves income quality.

4

20hDelivery Capacity

More billable hours per mediator lifts revenue without much extra fixed cost, but only if scheduling stays tight.

5

50/yrReferral Pipeline

At a $500 CAC, a $25K marketing budget buys about 50 clients, so referrals can cut acquisition drag fast.

6

$220.8KCost Discipline

Fixed overhead is $70.8K and founder salary is $150K, so cost control has a direct hit on take-home.

Mediation and Negotiation Consulting Core Six Income Drivers

Billable Case Volume

Billable Case Volume

Income rises when more owner time turns into paid mediation, negotiation, prep, and follow-up. Year 1 assumes 5 billable hours per hourly mediation, 15 hours per corporate package, and 8 hours per retainer. Intake, scheduling, referral work, and documentation still take time, so the gap between calendar time and billed time drives take-home pay.

The key inputs are case count, billable hours per case, and utilization, which is the share of working time that gets billed. Higher utilization lifts revenue and cash flow only if quality and close rates stay intact. Push volume too hard and you can lose referrals, slow closes, and cut profit instead of raising it.

Track Billable Hours per Case

Measure billed hours by case type, plus nonbillable time for intake, follow-up, and admin. Compare that split to the 5 / 15 / 8 hour planning assumptions, and watch which referral sources turn into paid work. If conversion slips, higher utilization just creates more unpaid prep.

- Billable hours by case type

- Nonbillable admin hours

- Close rate by source

Use a weekly check on active cases, booked billable hours, and cash collected. With fixed overhead at $5,900 per month, weak billable volume hits margin fast, so the owner’s pay depends on keeping the calendar full of paid sessions, not just busy work.

1

Average Engagement Fee

Average Engagement Fee

Average engagement fee is the cash you collect per closed matter, before overhead. With Year 1 planning values of $1,250 for hourly mediation, $5,250 for corporate packages, and $1,600 for negotiation retainers, pricing can lift owner income faster than adding more cases when calendar time is tight. Higher-fee matters also cover fixed costs sooner, which supports owner draw.

Here’s the quick math: the fee depends on case mix, billed hours, scope, and discounting. Compare hourly, half-day, full-day, retainer, and project pricing as planning variables. What this hides: state, dispute type, and prep time can change realized margin, so do not treat any rate as a universal market price.

Raise Fee per Matter

Track realized fee per matter, effective hourly rate, and write-offs on every closed case. If utilization is tight, the fastest income move is usually a better package mix, not more low-dollar sessions. The goal is simple: raise cash per booking without adding unpaid admin time.

- Closed matters by type

- Billed hours per matter

- Discounts and write-offs

- Prep and follow-up time

Use a price sheet by dispute type and expected hours, then compare booked revenue against hours delivered. If a 15-hour package needs extra unpaid work, take-home drops fast. Control scope early so the average fee stays real, not just quoted.

2

Case And Service Mix

Case and Service Mix

Your income shifts when the work mix shifts. In Year 1, the model assumes 70% hourly mediation, 20% corporate packages, and 10% retainers; by Year 5, it moves toward 60% hourly mediation, 40% corporate packages, and 25% retainers. That mix changes revenue per hour, staffing load, and how much owner pay is left after delivery costs.

Here’s the quick math: a Year 5 corporate package uses 20 hours at $400, or an $8,000 package value. More package work can lift cash collected per engagement, but it also ties up capacity longer. The real risk is overload: if higher-value work blocks billable hours or adds contractor time, gross margin can slip even when topline revenue rises.

Track Mix by Hour, Not Just by Case

Measure the share of billed hours, not just the number of cases. Track hourly mediation, package hours, and retainer hours separately, then compare revenue per hour and direct labor cost by service type. If packages consume more prep and follow-up than planned, the owner’s draw falls even when booked revenue looks strong.

Set a monthly mix target and test it against capacity. Watch utilization (billable hours divided by available hours), close rate, and contractor use. If the mix shifts toward corporate packages, make sure pricing covers the extra time and admin load. One bad mix can crowd out better-paying work fast.

- Track revenue per billable hour.

- Split prep time from paid time.

- Flag low-margin package work.

- Watch contractor hours by service.

3

Delivery Capacity And Staffing

Staffing Capacity

Delivery capacity is the number of mediations, prep hours, and follow-up hours the team can sell and complete. Here, associate mediators and contractors can lift revenue, but they also cut gross margin: external mediator fees run at 10% of revenue in Year 1 and 8% by Year 5, while payroll climbs from $235,000 to $595,000. If booked hours do not keep pace, staffing becomes owner wage replacement, not profit growth.

The key inputs are billable hours, utilization, case mix, contractor fees, and supervision time. One clean rule: unused associate capacity hurts take-home fast. If the owner hires ahead of demand, payroll and oversight rise before revenue does, so cash flow tightens even when top-line sales look better.

Track Utilization, Not Headcount

Measure billable hours per mediator, percent of time spent on intake and prep, and revenue per staffed hour. Separate owner delivery hours from true profit expansion so you do not count your own labor shift as new growth. Also track fee mix by case type, because higher-fee work can cover staffing overhead faster than low-complexity matters.

Use this simple check: if added staff do not raise revenue enough to absorb the 10% to 8% fee load plus a payroll base that grows to $595,000, margin weakens. The fix is tighter scheduling, faster case assignment, and hiring only when booked capacity is already near full.

- Billable hours per associate

- Utilization by week

- Contractor fee % of revenue

- Owner hours versus paid staff hours

- Revenue per staffed hour

4

Referral Pipeline

Referral Pipeline

Referral pipeline is the flow of cases from attorneys, HR teams, business owners, courts, professional networks, and online search into paid wor k. With a $25,000 Year 1 marketing budget and $500 CAC, the model buys about 50 cases or qualified leads; at $100,000 and $350 CAC, that rises to about 286. More low-cost referrals lift billable volume and owner draw.

What this hides is intake quality. If follow-up is slow, paid leads go cold, utilization drops, and fixed overhead absorbs more of each case. One clean rule: faster response and stronger repeat referrals matter more than more ad spend when you already have a trusted referral base.

Track intake conversion

Measure lead source, response time, consult-to-case close rate, and CAC by channel. Split attorney and HR referrals from search because they behave differently. The goal is simple: turn the same budget into more billable hours, not just more inquiries.

- Call within one business hour.

- Log repeat referral sources.

- Compare CAC by channel.

- Track no-show and loss reasons.

If conversion rises and repeat referrals grow, CAC falls and more revenue drops to profit instead of being spent on re-acquisition.

5

Overhead And Reserves

Fixed Overhead and Cash Reserve

Fixed overhead is the monthly cost base that sits under every case: office rent, insurance, admin software, supplies, legal and accounting, hosting, internet, and professional development. Here that runs $5,900 per month, or $70,800 a year, before any variable delivery costs. One clean rule: if revenue is flat, every $1 cut from fixed overhead adds $1 to profit only after the work still runs smoothly.

The reserve matters just as much. Startup capital items total $68,000, and minimum cash is $839,000 in Month 2, so the owner cannot treat low overhead as free money. If cash gets too tight, compliance slips, service quality drops, and lead generation weakens, which hurts billable case volume and owner pay faster than the savings help.

Keep the Cost Base Funded

Track fixed overhead as a percent of monthly revenue and keep a line item view of the big drivers: rent, software, legal and accounting, and internet. That tells you whether the business is lean or just under-resourced. Overhead should stay funded before owner draws grow.

Use the reserve to protect three things: compliance, service quality, and lead flow. If you trim spend, test it one line at a time and confirm the savings do not slow intake, scheduling, or case handling. The goal is lower overhead without breaking the pipeline that fills billable hours.

- $5,900 monthly fixed overhead

- $70,800 annual fixed overhead

- $839,000 Month 2 minimum cash

- $68,000 startup capital items

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with client mix, CAC, staffing, and how fast the firm reaches breakeven. Founder-led delivery looks lean early, while contractor scale and lower CAC lift pay later.

| Scenario | Low CaseLean case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lean launch path, where the founder carries most delivery and pay stays at the modeled $150,000 salary level. | This is the modeled operating case, where Year 2 scale supports steadier owner pay and profit. | This is the stronger upside path, where the practice scales into a multi-mediator model with much higher profit capacity. |

| Typical setup | Year 1 stays mostly hourly mediation, with 70% of clients in that line, $25,000 marketing, $500 CAC, 85% gross margin, and Month 6 breakeven. | The mix shifts toward corporate packages and retainers, marketing rises to $40,000, CAC eases to $450, and EBITDA reaches $604,000 with 86% gross margin. | By Year 5, corporate packages and retainers carry more of the mix, marketing reaches $100,000, CAC falls to $350, and EBITDA reaches $4,697,000 with 89% gross margin. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $150k salary pathLean income | $604k EBITDA pathCore income | $4.697M EBITDA pathUpside income |

| Best fit | Best for a solo founder stress-testing early cash use and slower client build. | Best for planning staffing, cash needs, and the owner draw in a balanced growth case. | Best for an experienced operator who can use contractors, protect margin, and hold a cash reserve. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Mediation and Negotiation Consulting Porter's Five Forces Analysis

- Mediation and Negotiation Consulting BCG Matrix

- Mediation and Negotiation Consulting Business Model Canvas

- Tracking Key Financial Metrics for Mediation and Negotiation Consulting

- Mediation and Negotiation Consulting Business Plan Template in Pre-Written Word

- How to Increase Mediation and Negotiation Consulting Profitability in 7 Practical Strategies

- How Much Does It Cost To Run Mediation and Negotiation Consulting Monthly?

- Mediation Consulting Startup Costs: $33K-$68K Before Runway

- Mediation and Negotiation Consulting Financial Model Template in Excel

- How To Open A Mediation And Negotiation Consulting Business In 8 Weeks

- How to Write a Business Plan for Mediation and Negotiation Consulting

- Mediation and Negotiation Consulting Marketing Mix

- Mediation and Negotiation Consulting Marketing Plan

- Mediation and Negotiation Consulting Business Proposal

- Mediation and Negotiation Consulting PESTEL Analysis

- Mediation And Negotiation Consulting Pitch Deck Example Editable PPTX

- Mediation and Negotiation Consulting Business SWOT Analysis

- Mediation and Negotiation Consulting Value Proposition Canvas

Frequently Asked Questions

This model plans $150,000 in founder salary, plus possible distributions from business profit EBITDA is $83,000 in Year 1 and $604,000 in Year 2 By Year 5, EBITDA reaches $4697 million under the assumptions Distributions still depend on cash reserves, reinvestment, debt, and tax planning