Time to Open8-12 weeksSetup window

Time to Open8-12 weeksSetup windowHow to Open a Merchant Services Company in 60 to 120 Days

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Time to Open8-12 weeksSetup window  Launch Sequence6 stagesEntity first

Launch Sequence6 stagesEntity first Key BottleneckApproval gateRisk review

Key BottleneckApproval gateRisk review First Revenue StepFirst residualsMerchants live

First Revenue StepFirst residualsMerchants live

You’re building the rails before you sell, so the real launch work is processor approval, compliance setup, underwriting flow, merchant boarding, and first-account activation This guide covers 60 to 120 days of payment processing business setup, with costs, funding, and residual income treated as planning checks inside the first-year and five-year model Your next step is to pick the launch path, then validate merchant acquisition against the Year 1 assumption of $150,000 in seller marketing at $500 CAC

Time to Open8-12 weeksSetup windowLaunch Sequence6 stagesEntity firstKey BottleneckApproval gateRisk reviewFirst Revenue StepFirst residualsMerchants liveMerchant services launch timeline

This is a short web summary of the launch plan, and the XLSX export carries the detailed Gantt Chart.

Launch scheduleWeek 1Week 2Week 3Week 4Week 5Week 6Week 7Week 8Week 9Week 10Week 11Week 12

Formation / compliance

- Entity setup

- Bank paperwork

- Licenses review

- Tax registrations

Partner / underwriting

- Processor shortlist

- ISO outreach

- Pricing model

- Approval package

Risk / boarding

- Risk rules

- Underwriting matrix

- Identity checks

- Boarding forms

Platform / tools

- CRM setup

- Merchant portal

- Gateway tests

- POS coordination

Sales / marketing

- Sales scripts

- Lead list

- Partner offers

- Demo calls

Support / finance

- Support desk

- Agent training

- Residual tracking

- Fee reconciliation

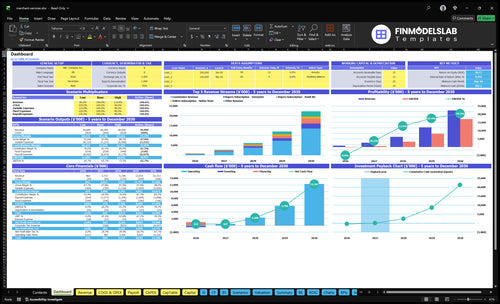

Why test the Merchant Services model before launch?

The Merchant Services Financial Model Template maps revenue, costs, cash needs, assumptions, and break-even logic—open the model.

Financial model highlights

- Dashboard and assumptions tabs

- Merchant ramp and volume

- $0.10 fixed commission

- 2.90% variable commission

- 1.80% network fees

- $29, $49, $39 plans

- Staffing, runway, break-even

- Charts and sensitivity checks

How do I get first merchant services clients?

Get your first Merchant Services clients by starting with local businesses and tight verticals that underwrite cleanly and can go live fast. Use referral partners like POS installers, accountants, and web agencies, plus your own network, then close with statement reviews, clear pricing, and onboarding checklists. The Year 1 model assumes $150,000 in seller marketing at $500 CAC for about 300 acquired sellers, with a mix of 40% small retail, 35% online stores, and 25% service providers; see What Is The Estimated Cost To Open And Launch Your Merchant Services Business? because first revenue starts when approved processing volume goes live, not when a lead says yes.

Best first clients

- Start with local businesses first

- Pick high-fit vertical niches

- Use referral partners

- Tap existing business networks

What closes deals

- Use statement reviews

- Keep pricing clear

- Run onboarding checklists

- Focus on approved volume

Should I start as an ISO or payment facilitator?

For Merchant Services, start as an agent, referral partner, reseller, or registered ISO before becoming a payment facilitator; What Is The Main Goal Of Merchant Services Business? is still the same: get approved merchants processing payments first. Payment facilitator gives more control, but it adds heavier underwriting, disputes, funding, technology, and compliance work.

Start lighter

- Use 4 starter paths: agent, referral, reseller, ISO

- Launch faster with lower compliance burden

- Accept less control over pricing and underwriting

- Earn after approved merchants process payments

Scale later

- Choose payment facilitator for more control

- Prepare for 5 risk areas: compliance, disputes, funding, underwriting, tech

- Support 3 revenue streams: transactions, subscriptions, add-ons

- Match launch path to merchant support capacity

What delays starting a merchant services company?

Starting a Merchant Services company usually stalls at payment processor approval, not at selling. A realistic launch window is 60 to 120 days when due diligence, sponsor bank rules, compliance docs, pricing approval, underwriting, prohibited merchant categories, gateway setup, equipment coordination, and onboarding all move in parallel. If the underwriting policy or support flow is unclear, the first activation slips, and that can push back the Year 1 target of about 300 sellers.

Main delay points

- Due diligence slows partner approval.

- Sponsor bank rules add steps.

- Compliance docs must be complete.

- Pricing approval can hold launch.

Launch risks to watch

- Underwriting rules block weak merchants.

- Prohibited categories stop some deals.

- Gateway setup needs coordination.

- Incomplete onboarding delays first activation.

Check whether the merchant services startup checklist is launch-ready

Launch readiness checklist

Use this go-live approval checklist to confirm the business is ready to open before launch.

Entity

- Entity formation filedCritical

You need a legal entity before contracts, banking, and processor onboarding.

- Operating agreement signedHigh

This sets control, duties, and decision rights before launch.

- Tax IDs and accounts readyHigh

You need tax setup ready for payroll, filings, and vendor forms.

Compliance

- Underwriting rules approvedCritical

Use this to accept or reject merchants before boarding.

- Prohibited categories listedCritical

Blocked categories reduce chargeback and fraud losses.

- PCI awareness training doneHigh

Staff must know card data rules before handling payments.

Partners

- Processor agreement approvedCritical

No processing means no merchant boarding or live payments.

- Gateway and POS testedHigh

Test the payment stack before any merchant goes live.

- Merchant boarding flow passedCritical

The activation path must work from application to approval.

Onboarding

- Application pack completeHigh

Missing docs slow underwriting and delay first revenue.

- Document collection list setHigh

Collect tax and business records in one clean step.

- Support escalation path knownHigh

Staff need a fast path for failed activations and disputes.

Sales

- Pricing sheet signed offCritical

Rates, fees, and terms must match the model before selling.

- Sales scripts approvedHigh

Scripts keep claims consistent and lower compliance risk.

- First merchants identifiedCritical

You need real launch targets, not just a lead plan.

- Merchant fees mappedMedium

Fee mix drives seller revenue and merchant retention.

Finance

- Cash runway reviewedCritical

You need enough cash for Month 9 breakeven and early losses.

- Model assumptions lockedHigh

CAC, mix, and fees must match the launch plan.

- Go-live signoff completeCritical

Do not sell until compliance, tools, and support are ready.

- First revenue targets setMedium

Set the first merchants and volume target before opening.

Want to see the main merchant services launch drivers?

1Processor Ready

60-120dA signed processor or sponsor deal is the launch gate; without it, merchant boarding and residuals can't start.

2Compliance Controls

Boarding rulesWritten underwriting and chargeback rules cut rejected apps and keep first revenue cleaner.

3Onboarding Flow

1 test merchantA full test onboarding flow speeds activation and prevents missing-doc support loops.

4Pricing Model

2.9% + $0.10Clear pricing tied to residual math protects margin and makes partner approvals easier.

5Sales Channels

$150K / $500 CACChannel mix should produce boardable merchants, not just leads, and hit about 300 sellers in Year 1.

6Support Ops

Dispute ownerNamed owners for funding, equipment, and disputes help retain early merchants after activation.

Processor And Sponsor Relationship Readiness

Processor and Sponsor Readiness

Merchant boarding is the launch gate. Until the processor, ISO, or acquiring sponsor signs the partner deal and approves the boarding path, you cannot reliably open, set pricing, or activate merchants. Any delay here pushes sales from planning into limbo and can stall first revenue even when demand is ready.

This driver also controls who can be boarded, what risk rules apply, and how residual payments are reported. If the partner has not approved escalation contacts and underwriting steps, day one service can break fast: applications sit pending, merchants wait longer, and cash timing gets messy.

Confirm the Boarding Path Before You Sell

Get the partner diligence, pricing terms, residual reporting, risk rules, and escalation contacts in writing before launch. The readiness check is simple: a signed reseller or partner agreement plus an approved boarding workflow that a teammate can follow without founder help.

- Verify merchant categories the partner will accept.

- Test the boarding steps end to end.

- Assign one owner for approvals.

- Document who handles rejects and escalations.

If approval slips, do not book activation dates you cannot hit. That is the fastest way to miss day-one capacity and damage trust with early merchants.

1

Compliance And Risk Controls

Compliance And Risk Controls

If you board the wrong merchants, launch slows fast. Underwriting standards, know-your-customer checks, prohibited categories, and chargeback rules decide who can go live, so this work has to be set before sales starts pushing applications.

The key dependency is processor or sponsor policy. If your rules do not match their rules, they can reject accounts after you spend time selling them, which delays opening and creates messy first revenue. Payment Card Industry Data Security Standard (PCI DSS) awareness also has to be built in from day one.

Launch-Ready Risk Screen

Build a written process a salesperson can follow before opening. It should tell the team how to screen merchant type, check identity details, flag prohibited categories, and route higher-risk cases for review before any promise is made to the customer.

- Match policy to the processor.

- Screen before application submission.

- Document chargeback review steps.

- Train on PCI DSS basics.

- Assign a merchant risk reviewer.

The goal is simple: fewer rejected applications, less rework, and a cleaner first month of revenue. Accepting merchants the partner will reject is the launch bottleneck, because it burns sales time, delays activation, and can leave day-one support scrambling.

2

Merchant Onboarding Infrastructure

Merchant Onboarding Flow

Merchant onboarding has to work before opening day. If the application, document collection, pricing approval, gateway setup, and terminal or POS coordination are not sequenced cleanly, the business cannot move a merchant from sale to activation without delay. The readiness test is simple: 1 test merchant should move through the full workflow with no missing handoffs.

The key dependency is processor boarding portal and gateway access. If that access is late, sales may start but first revenue will not. Missing documents, unclear ownership, or a slow post-approval handoff can turn into support issues on day one, which means slower first activation and more founder time spent fixing basics instead of serving merchants.

One Test Merchant Run

Map each step in order: application, document intake, pricing approval, gateway setup, terminal or POS coordination, CRM tracking, activation, and handoff. Assign one owner per step and require a timestamped checkpoint so nothing sits in a queue.

Use the pilot merchant to check the weak spots: missing paperwork, pricing changes, portal access, and escalation contacts. If the workflow breaks once, fix it before launch. Fast first activation depends on clean docs and a clear owner for every handoff.

- Verify processor portal access first

- Collect documents before approval

- Track every step in CRM

- Confirm activation handoff owner

3

Pricing And Residual Economics

Pricing and Residual Economics

If your merchant pricing is off, you can’t open cleanly. The launch gate is a pricing sheet that matches partner terms: $0.10 fixed commission per order, 2.90% variable commission, and the 1.80% interchange and network fees that sit underneath it. If those numbers don’t line up with the processor buy rate and residual split, sales can promise margin you can’t actually keep.

This driver also affects day-one cash. You need the inputs for processor buy rates, residual splits, equipment fees, statement analysis, and margin assumptions before the first merchant boards. If the model is wrong, approvals slow down and residual tracking gets messy, which makes it hard to tell what each account really earns. Simple rule: if sales can’t explain the pricing in one minute, the launch is not ready.

Verify the margin math first

Before opening, build one pricing sheet and have sales, finance, and the partner review it together. Tie every offer to the actual residual math, not a target price. Here’s the quick check: commission collected minus interchange, network fees, buy rate, residual split, and equipment costs. If the sheet does not show the margin by account type, do not start selling that package.

Test it on one sample merchant and one statement review before launch. Confirm the pricing can support boarding, approval, and residual reporting without manual fixes. Keep the assumptions in writing so the team knows what to quote, what to avoid, and what terms need partner sign-off. That keeps first revenue cleaner and cuts the risk of selling unsupported margin.

- Match quotes to buy rates

- Document residual splits clearly

- Price equipment and statement fees

- Test one merchant before launch

4

Sales Channel Development

Boardable Seller Pipeline

Sales has to create boardable merchants, not just leads. For year 1, the plan assumes $150,000 in seller marketing, $500 seller CAC, and about 300 acquired sellers; that only works if prospects are already qualified and their documents are ready, so applications can move straight into boarding.

The mix matters too: 40% small retail, 35% online store, and 25% service provider, or about 120, 105, and 75 sellers. If channels generate weak-fit leads, approval slows, first revenue slips, and the business opens with a sales queue instead of live merchants.

Preboard Before Spend

Build channels around local businesses, vertical niches, referral partners, POS installers, web agencies, accountants, and statement review campaigns, but only count prospects that can board. The readiness signal is a qualified pipeline with documents ready, because that is what drives faster first approved accounts and protects the launch date.

- Screen for boardable fit first.

- Track doc-ready status in CRM.

- Match channel mix to target segments.

- Review seller CAC against $500.

5

Support And Chargeback Operations

Support and Chargeback Coverage

Early merchants will ask for funding, equipment, gateway access, and dispute setup on day one. If those questions bounce around, activation slows and first merchants can leave before they see value. The key dependency is partner support access for processor communication and chargeback handling.

A launch-ready setup has support coverage, clear escalation paths, and troubleshooting scripts. The readiness signal is a named owner for each issue type. That keeps urgent calls off the founder, reduces merchant confusion, and lowers the risk of losing the first accounts after activation.

Assign Issue Ownership Before Launch

Assign one owner for funding, equipment, gateway access, and chargebacks before opening. Test the processor handoff, document who replies first, and keep the dispute script ready. One clean path matters more than a big team.

- Verify processor escalation contacts.

- Document chargeback steps.

- Test gateway troubleshooting.

- Track issues by merchant.

6

Related Products

- Merchant Services Porter's Five Forces Analysis

- Merchant Services BCG Matrix

- Merchant Services Business Model Canvas

- 7 Critical KPIs for Merchant Services Success

- Merchant Services Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Merchant Services Profitability and Scale

- How Much Does It Cost To Run A Merchant Services Company Monthly?

- Merchant Services Startup Costs: $500 CAC and $88k Monthly Fixed Costs

- Merchant Services Financial Model Template in Excel

- How Much Merchant Services Owners Make at $46M to $1017M Volume?

- How to Write a Merchant Services Business Plan in 7 Steps

- Merchant Services Marketing Mix

- Merchant Services Marketing Plan

- Merchant Services Business Proposal

- Merchant Services PESTEL Analysis

- Merchant Services Pitch Deck Example Editable PPTX

- Merchant Services Business SWOT Analysis

- Merchant Services Value Proposition Canvas

Frequently Asked Questions

Start by choosing a launch path, usually referral partner, agent, reseller, or ISO before a heavier processor model Then form the entity, secure a processor relationship, document underwriting rules, build the merchant application workflow, and sell to boardable merchants Use 60 to 120 days as the planning range