Owner income$1.1M to $105M

Owner income$1.1M to $105MHow Much Merchant Services Owners Make at $46M to $1017M Volume?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.1M to $105M  Net margin864%

Net margin864% Revenue for target pay$105M

Revenue for target pay$105M Business difficultyHard

Business difficultyHard

In the first-year planning case, the business processes about $46M, earns about $7727K of revenue, and has about $1112K available before CEO pay, taxes, reserves, other payroll, and reinvestment The modeled CEO salary is $180K, so the first year shows a $688K shortfall after that salary before excluded costs By the mature-year case, processing volume reaches about $1017M and revenue reaches about $167M, creating much more owner draw capacity if churn, risk, staffing, and reserves stay controlled

Owner income$1.1M to $105MNet margin864%Revenue for target pay$105MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, costs, reserves, and owner pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on volume, pricing, churn, payroll, taxes, reserves, and execution.

Need to see the whole forecast for Merchant Services?

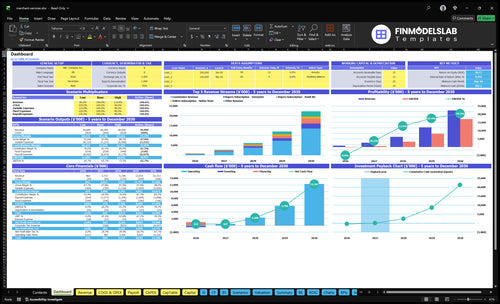

Yes — the Merchant Services Financial Model Template shows the full dashboard, revenue build, processing volume, subscriptions, commissions, COGS, variable costs, fixed overhead, CEO pay, cash reserves, and scenario output. Use it to test owner income, margin, and funding gaps before you plan the next step.

What the forecast shows

- CEO pay and take-home

- Gross margin and profit

- Scenario charts at $46M, $266M, $1017M

Can a merchant services business scale owner income?

Yes—Merchant Services can scale owner income, but only when growth is profitable, merchants stay retained, and the net spread stays healthy. Here’s the quick math: seller CAC falls from $500 to $300, buyer CAC from $20 to $10, and processing volume rises from $46M to $1,017M; still, this is not passive income because churn, chargebacks, and support can pull cash out fast.

What drives owner income

- Grow profitable account volume

- Keep merchants retained longer

- Lower seller CAC to $300

- Lower buyer CAC to $10

What limits the scale

- Coordinate underwriting and risk

- Control support load and fraud

- Manage partner relationships closely

- Keep cash reserves for reversals

What merchant services profit margin should owners watch?

Owners should watch operating margin and cash before distributions, not just gross margin. In Merchant Services, year-one revenue is about $7,727K, with about $1,052K of interchange and gateway cost, and you can sanity-check launch spend with What Is The Estimated Cost To Open And Launch Your Merchant Services Business?. A small drop in net basis-point spread or a rise in chargebacks can erase owner take-home fast.

Gross margin math

- Revenue starts at $7,727K.

- Interchange plus gateway costs hit $1,052K.

- Gross margin is about 86.4%.

- Support and fraud costs come next.

Cash to owner

- Contribution is about $5,668K.

- Marketing is about $350K.

- Fixed overhead is about $1,056K.

- Cash before CEO pay is about $1,112K.

How do merchant services owners make money?

Merchant Services owners make money by keeping the spread between what sellers pay and what processing, payouts, chargebacks, support, and overhead cost; see What Is The Main Goal Of Merchant Services Business? for the core model. Here’s the quick math: on a $100 order, a 2.70%–2.90% variable commission produces $2.70–$2.90, before adding fixed and subscription fees.

Main revenue

- Keep net processing spreads

- Charge $0.10–$0.15 per order

- Collect seller plans: $29–$59

- Add seller extras: $10–$15

Profit drivers

- Sell buyer plans: $0–$35

- Mark up equipment or software

- Earn residual split income

- Control chargebacks and support costs

Want the six biggest income drivers?

1

$46M-$1.0BProcessing Volume

More card volume lifts fee income and spreads fixed overhead across more swipes.

2

290bp-270bpNet Spread

A tighter take rate keeps more gross profit after interchange and gateway costs.

3

2.5x-9.0xMerchant Retention

Longer merchant life raises recurring fees and makes each acquisition dollar work harder.

4

$586K-$1.0MFixed Overhead

Payroll and fixed costs set the break-even line, so slower hiring boosts EBITDA.

5

$0.10+290bpResidual Split

Better split terms and commissions keep more of each transaction dollar for the owner.

6

70bp-50bpChargeback Risk

Fewer disputes and smaller reserves protect cash and stop revenue leakage.

Merchant Services Core Six Income Drivers

Monthly Processing Volume

Monthly Processing Volume

When monthly card volume rises, owner income usually rises too, but only the retained spread becomes company revenue. In this model, annual source volume scales from $46M in year 1 to $266M in the base case and $1.017B in a mature year, while revenue moves from about $7.7M to $45M to $167M.

What this hides is mix. Stable merchants with clean chargeback history drive stronger cash flow; low-margin or dispute-heavy merchants can add volume but cut owner take-home through reserves, support work, and payout friction.

Track Volume Quality, Not Just Volume

Watch monthly volume by merchant, plus chargeback rate, reserve holds, and retained spread. If a merchant adds volume but weakens margin, it is not good volume. Here’s the quick math: more volume only helps if the spread after pass-through costs still leaves cash for overhead and owner pay.

Set a clean-account target and test new merchants against it before scaling. Volume from stable accounts with low disputes protects recurring revenue and makes draws more predictable, while risky accounts can force extra compliance and delay cash.

1

Net Basis-Point Spread

Net Basis-Point Spread

Net basis-point spread is the slice left after pass-through payment costs. In this model, commission runs from 2.90% to 2.70% of order value, plus $0.10 to $0.15 per order, while interchange and gateway costs run from 2.30% combined in year one to 2.00% in the mature year. The first-year net processing spread proxy is about 0.67% after fixed order fees and processing COGS.

That spread is what funds owner pay after processor splits, support, and overhead. On high volume, even a small shift in spread moves cash fast, so the key inputs are order value, order count, fee mix, and pass-through rates. Small spread changes matter a lot at scale.

Track the spread, not just volume

Measure retained revenue per order and per dollar processed. Use order value, monthly processing volume, interchange, gateway fees, and fixed order fees to model the net spread each month. If volume rises but the spread slips, owner take-home can still stall.

- Track spread by merchant segment.

- Flag high-fee or dispute-heavy accounts.

- Test pricing against true pass-through cost.

- Separate fixed fees from percentage fees.

Here’s the quick check: if the spread is close to the 0.67% proxy, margins are thin and fee control matters more than sales growth. If onboarding or processing costs drift up, update the model right away so owner draws are based on current net cash, not gross volume.

2

Merchant Retention

Merchant Retention

Merchant retention means keeping sellers active so they keep paying monthly fees and keep processing volume. When merchants churn, recurring residual revenue drops, and the owner has to replace it with new sales. With fees at $29 to $59 per seller, even small churn hits cash flow fast.

Here’s the quick math: losing 100 sellers cuts $2,900 to $5,900 in monthly subscription revenue before processing and referral income. Replacing those sellers can cost $500 each, falling to $300, so churn is expensive on both the revenue and sales sides.

Track Active Sellers

Measure active seller count, monthly churn, fee tier mix, and processed volume per merchant. Retention only compounds if sellers stay active and process enough volume, so dormant accounts look busy but pay little. The owner’s take-home improves when support load falls and referrals keep coming from long-tenured merchants.

- Track monthly active sellers.

- Watch churn by fee tier.

- Compare retention to acquisition cost.

- Test save offers before cancellation.

If churn rises, new sales just keep revenue flat. Protecting retention is cheaper than replacing merchants at $300 to $500 per acquisition and keeps residual income compounding instead of resetting.

3

Residual Split And Commissions

Residual Split And Commissions

Residual split is the cash left after you pay processor splits, sales rep commissions, referral partner payouts, and agent overrides. It starts with gross commission revenue, not owner take-home. The key inputs are processed volume, commission rate, and each payout layer. A small shift matters fast: a 10-point higher payout on $1M of volume cuts distributable cash by $100k.

The model gives commission revenue rates, but it does not fix the residual split, so this line must stay editable. Direct-sold accounts should keep more margin than partner-sourced accounts. If the payout stack gets too rich, reported revenue can look fine while owner cash stays thin and harder to draw.

Track the payout stack by source

Measure gross commission first, then subtract each payout layer one by one so you can see true owner margin. Here’s the quick math: owner cash = gross residuals - processor split - rep commission - referral payout - agent override. That tells you which channel is worth scaling.

- Separate direct-sold and partner-sourced accounts.

- Set a target net residual per $1 of volume.

- Review payout changes every month.

4

Operating Costs And Owner Role

Operating Costs And Owner Role

Operating costs decide how much gross profit reaches the owner. Here, fixed overhead is $88K per month, or about $1.056M per year, before any owner draw. The modeled CEO salary is $180K per year, so the owner pay line must be separated from business overhead.

Marketing rises from $350K in year 1 to $25M in a mature year, so cash burn can jump fast. Owner-run teams may save cash early, but support, compliance, fraud, and onboarding still need coverage. One clean rule: if those jobs are underfunded, owner income gets squeezed even when sales grow.

Track Overhead Before Owner Pay

Measure monthly overhead, owner salary, and marketing spend separately. Here’s the quick math: with $88K fixed overhead and $180K CEO pay, the business already carries $103K a month before variable work starts. That means owner distributions should come only after service, compliance, and fraud costs are covered.

- Track support hours and ticket volume.

- Track onboarding time by merchant.

- Track fraud losses and chargebacks.

- Track compliance and legal work monthly.

- Track salary, draw, and distributions separately.

Test whether a leaner owner role still protects service quality. If onboarding slows or fraud review piles up, the cash saved on headcount can disappear fast. The goal is simple: keep overhead tight enough to fund growth, but not so thin that the owner has to cover operating gaps out of personal cash.

5

Chargeback Risk And Reserves

Chargeback Risk And Reserves

If your processing volume looks strong but owner draws stay tight, chargebacks and reserves are usually the reason. This driver includes fraud losses, dispute handli ng, and processor holdbacks. In year one, a 0.70% cost on $45.75M of volume is about $320K; at 0.50% on $1.017B, it is about $5.085M.

Reserves are cash planning, not income. A high-risk merchant mix can trigger processor holds, more support work, and slower owner draws. So even when revenue rises, cash available for payroll, taxes, and distributions can lag the P&L. Here’s the quick math: more disputes and bigger holds cut the money you can safely pay out.

Manage Holds Before They Cut Draws

Model this driver from three inputs: monthly processing volume, chargeback rate, and reserve hold. Separate low-risk and high-risk merchants, then forecast cash by payout timing, not just sales booked. If a merchant group keeps pushing disputes up, price for the extra risk or tighten onboarding before it drains owner pay.

- Track disputes by merchant.

- Forecast holds before owner draws.

- Watch support time tied to disputes.

- Keep reserve cash outside income.

Test reserve levels against worst-month volume, then keep distributions below the cash left after holds and dispute costs. If chargebacks rise, the fix is usually mix, rules, and underwriting, not more sales. Otherwise the business can look profitable while the owner waits weeks or months to get paid.

6

Compare low, base, and mature owner-income scenarios

Owner income scenarios

Seller mix, buyer count, and processing volume swing revenue hard, while payroll, support, and compliance costs rise as the team scales.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower owner-income case, where first-year volume and a lean seller base leave little cushion after pay. | This is the modeled mid-case, where year-three scale starts to cover the operating team and owner pay. | This is the stronger earnings path, where year-five scale leaves much more room for the owner. |

| Typical setup | The model uses first-year assumptions with 300 sellers, 10,000 buyers, $4,575M of processing volume, $7,727K of revenue, and a thin margin after COGS and variable costs. | The model uses year-three assumptions with 1,250 sellers, 46,667 buyers, about $266M of processing volume, and about $45M of revenue before excluded items mature. | The model uses year-five assumptions with 3,333 sellers, 150,000 buyers, about $1,017M of processing volume, and about $167M of revenue before excluded items mature. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$688KLow Case | $194MBase Case | $1.036BHigh Case |

| Best fit | Use this to stress-test early traction and pay pressure. | Use this for a working plan with a scaled sales and support team. | Use this to test upside if buyer and seller volume both mature. |

Planning note: These ranges use researched planning assumptions and are not guaranteed earnings, salary promises, tax advice, or distributions; they also exclude other payroll, reserves, taxes, debt service, and guaranteed distributions.

Related Products

- Merchant Services Porter's Five Forces Analysis

- Merchant Services BCG Matrix

- Merchant Services Business Model Canvas

- 7 Critical KPIs for Merchant Services Success

- Merchant Services Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Merchant Services Profitability and Scale

- How Much Does It Cost To Run A Merchant Services Company Monthly?

- Merchant Services Startup Costs: $500 CAC and $88k Monthly Fixed Costs

- Merchant Services Financial Model Template in Excel

- How to Open a Merchant Services Company in 60 to 120 Days

- How to Write a Merchant Services Business Plan in 7 Steps

- Merchant Services Marketing Mix

- Merchant Services Marketing Plan

- Merchant Services Business Proposal

- Merchant Services PESTEL Analysis

- Merchant Services Pitch Deck Example Editable PPTX

- Merchant Services Business SWOT Analysis

- Merchant Services Value Proposition Canvas

Frequently Asked Questions

In the first-year model, the business generates about $7727K of revenue on $4575M of processing volume Cash before CEO pay is about $1112K, while the modeled CEO salary is $180K In the mature-year case, revenue reaches about $167M on $1017M of processing volume before excluded payroll, taxes, reserves, and reinvestment