Owner income$0-$10.2M

Owner income$0-$10.2MHow Much Does A Mixed-Use Development Owner Make Over 60 Months

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0-$10.2M  Net margin16%-31%

Net margin16%-31% Revenue for target pay$33.24M

Revenue for target pay$33.24M Business difficultyHard

Business difficultyHard

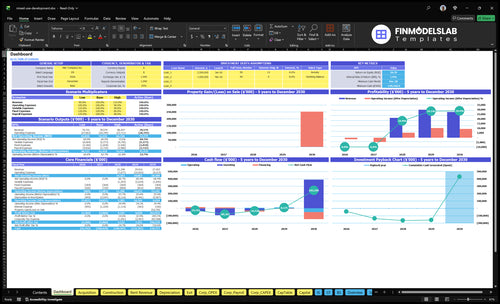

A mixed-use development owner can make nothing during early development and may only receive distributions after lease-up, debt service, reserves, and investor rules are covered In the researched assumptions, EBITDA is negative in Year 1 at -$1811M and Year 2 at -$4631M, then rises to $5282M in Year 3, $10192M in Year 4, and $9434M in Year 5 Full scheduled rental fees total $277M per month, but that is not owner income Owner income may come from development fees, stabilized cash flow, refinance proceeds, or sale gains

Owner income$0-$10.2MNet margin16%-31%Revenue for target pay$33.24MBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not a guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, debt, reserves, and timing.

Want to see the full Mixed-Use Development pro forma?

Open the Mixed-Use Development Financial Model Template to see the full pro forma as a planning tool: dashboard, rent roll assumptions, construction budget, acquisition schedule, operating expenses, wages, debt schedule, investor return outputs, and owner income outputs.

Key model outputs

- Owner income shown clearly

- EBITDA by year

- Test rent and vacancy

- Check cost and financing

Is mixed-use development profitable?

Mixed-Use Development can work in a long-run scenario: EBITDA is negative in Years 1 and 2, then turns positive at $5282M, $10192M, and $9434M in Years 3 to 5. The case also shows IRR 002%, ROE 3978%, payback at Month 60, and minimum cash of -$1406M in Month 36, so owner-operators can control costs better but passive investors still depend on sponsor execution.

What the case says

- Years 1 and 2 stay negative.

- Years 3 to 5 turn positive.

- Payback lands at Month 60.

- Cash bottoms at Month 36.

What to stress test

- Test lease-up delay risk.

- Model interest rate pressure.

- Check zoning issues.

- Review tenant mix and reserves.

What reduces mixed-use development profit margin?

Mixed-Use Development profit margin gets squeezed when you mix one-time build costs with ongoing operating leaks. The upfront stack already includes $115M construction, $45M owned acquisitions, and $405k initial capex, plus permitting, design, and tenant improvements; see What Is The Estimated Cost To Open, Start, Or Launch Your Mixed-Use Development Business? for the full cost lens. If lease-up slips past Month 26, fixed overhead of $30,300 per month can cut into returns fast.

Upfront cost drag

- $115M construction budget hits first.

- $45M in owned acquisitions adds more.

- $405k initial capex is still real cash.

- Permitting, design, and tenant improvements add pressure.

Operating margin leaks

- Variable expenses start at 90% of revenue in Year 1.

- They only fall to 60% by Year 5.

- $30,300 fixed overhead stays every month.

- Management, leasing, utilities, and insurance keep draining cash.

How do mixed-use development owners make money?

Mixed-Use Development owners make money from developer fees, rental cash flow, refinance proceeds, and sale gains, but rent is not the same as take-home income; see What Is The Current Growth Trajectory Of Your Mixed-Use Development Project? for the growth lens. At full run rate, the model shows $277M monthly scheduled rental fees, while EBITDA turns positive in Year 3 at $5,282M after early losses.

Income Sources

- Earn optional developer fees, if contracted

- Collect residential, retail, commercial, community-use rent

- Refinance after stabilized value increases

- Sell assets for realized gains

Cash Reality

- Subtract vacancy from scheduled rent

- Pay operating costs and reserves

- Cover debt service before distributions

- Split cash by ownership share

Want the six income drivers that matter most?

1

$2.77M/moLease Rates

Full scheduled rent is about $2.77M a month, so small pricing shifts move owner take-home fast.

2

Month 26Lease-Up Pace

Breakeven lands in Month 26, so faster filling gets cash positive sooner and raises take-home.

3

$50K-$800KTenant Mix

Monthly rent ranges from $50K to $800K across uses, so the blend of homes, offices, and retail changes average yield.

4

$115MBuild Cost

The build budget totals $115M, so any overrun cuts equity returns and pushes back payback.

5

Month 36Debt Timing

Cash bottoms out in Month 36, so funding timing and debt service decide how long owners carry the gap.

6

$67K/moOpex Burn

Year 1 fixed burn is about $67K a month, before variable costs, so lean overhead helps preserve cash.

Mixed-Use Development Core Six Income Drivers

Rent And Lease Rates

Rent and Lease Rates

Rent and lease rates drive owner income directly because every rent dollar flows into the waterfall before profit draw. In this model, gross potential rent comes from average residential rent, retail rent per square foot, and commercial rent, with $277M in monthly scheduled rental fees, or $3,324M a year at full run rate.

Once fixed overhead and payroll are covered, even a small rent lift can move EBITDA materially. Apartments usually stabilize faster, while retail and office leases can take longer to negotiate, so weak lease pricing can delay NOI and future distributions.

Track the rent stack

Measure average residential rent, retail rent per square foot, commercial rent, and gross potential rent by asset and lease term. The quick test is simple: if rent rises but concessions, downtime, or tenant improvements rise faster, owner cash does not improve.

- Track signed rent versus asking rent.

- Watch renewal spreads by property type.

- Model rent after concessions and free rent.

- Stress test EBITDA at small rent drops.

Use a monthly rent roll and update the forecast when a lease is signed, renewed, or reset. That keeps the distribution model honest and shows when a 1% to 2% rent change is enough to lift take-home cash after overhead.

1

Occupancy And Lease-Up Timing

Lease-Up Timing

Occupancy decides when owner income starts. A project can show strong gross rent on paper, but if space is still empty, vacancy loss and commercial downtime keep distributions at $0. In mixed-use assets, apartments often fill faster, while ground-floor retail can slow cash flow until the last bays lease.

Watch stabilized occupancy, absorption period, and rent concessions by use type. The disclosed milestones matter: Month 26 breakeven, Month 36 minimum cash of -$1,406M, and Month 60 payback. Faster lease-up pulls owner draws forward; delayed signing pushes them back even if gross rent potential is unchanged.

Track Absorption Weekly

Measure occupancy as leased space ÷ total leasable space, then split it by residential, office, and retail. That tells you where cash is really coming from and where delays are hitting owner income. One empty retail suite can drag the whole project, even when the apartments are close to full.

Use a simple lease-up sheet with leased units, asking rent, concessions, and days vacant. If retail is lagging, tighten pricing, shorten downtime, and track deal pace against the breakeven month. The goal is simple: get to cash flow fast enough that owner distributions can start and stay on.

- Track occupancy by asset type

- Record vacancy days by suite

- Log rent concessions monthly

- Compare absorption to breakeven

2

Tenant Mix And Use Mix

Tenant Mix And Use Mix

Tenant mix is the split across residential, retail, commercial, and community-use space. In this model, the income base comes from owned residential and commercial assets plus rented retail and community spaces, with $40k in monthly site rental cost sensitivity. More residential usually means steadier rent cadence, while retail and office can lift upside but also bring longer vacancy and concession risk.

What this changes for the owner is NOI and cash swings. A better mix can raise stable cash flow and make distributions easier to pay, but a weak mix can leave the project dependent on a few tenants. Here’s the quick math: if retail or office sit empty longer, the fixed $40k monthly site cost still runs, so take-home income falls fast.

How To Manage Tenant Mix

Track revenue share by use type, lease expiry dates, vacancy days, and concession levels. The key input set is simple: residential rent cadence, retail and office lease terms, community-space occupancy, and the monthly site rental cost. If one use type drives too much income, cash flow gets less stable.

- Test more residential for steadier rent.

- Use service tenants to support foot traffic.

- Watch office concessions and downtime.

- Forecast vacancy against the $40k site cost.

What this estimate hides is timing risk. If lease-up slips, the mix can look strong on paper but still produce weak cash flow, so the owner should favor tenant types that fill faster and hold through slower market cycles.

3

Development Budget And Construction Control

Construction Cost Control

Construction cost control decides whether the project ever gets to owner cash flow. On a $115M construction budget, plus $45M owned acquisition cost and $405k initial capex, even a small slip matters: a 5% overrun adds $5.75M before rent starts.

That budget includes hard costs, soft costs, tenant improvements, contingency, permits, and overruns. Design changes, delayed permits, and tenant improvement allowances can hit cash early, force more equity or debt, and push distributions later. Tight control protects ROE and reduces the Month 36 funding gap.

Track Budget Drift Weekly

Measure committed cost versus budget by line item, not just total spend. Here’s the quick math: a 1% swing on $115M is $1.15M, so change orders, permit delays, and tenant improvement requests need sign-off before they hit the draw schedule.

- Track hard costs by trade.

- Lock soft-cost assumptions early.

- Cap tenant improvement allowances.

- Update contingency after each draw.

- Escalate permit delays weekly.

Use a simple control rule: if approved changes eat contingency faster than planned, freeze new scope until the budget is reset. That keeps cash from leaking before occupancy and helps preserve the owner’s take-home once rent starts.

4

Financing And Debt Service

Debt Service Structure

Financing changes owner income even when operations look healthy. After NOI (net operating income), the cash left for the owner is reduced by principal, interest, and lender reserves, so a strong property can still throw off weak take-home cash if the loan is heavy.

Here’s the quick math: you need the construction loan, permanent loan, interest rate, loan-to-cost, DSCR (debt service coverage ratio), equity requirement, and any refinance proceeds. The model does not provide loan terms, so debt service must be entered as an assumption. Higher leverage can lift equity returns, but it can also eat Year 3 to Year 5 EBITDA.

Control the Debt Load

Measure cash after debt service, not just NOI. A simple rule: if the loan payment and reserves l eave too little free cash, owner pay stays thin even when rent and occupancy improve. That is the real risk with mixed-use projects.

Track these inputs on every deal:

- Interest rate and reset date

- DSCR at stabilization

- Loan-to-cost and equity need

- Reserve funding and timing

- Refinance proceeds at takeout

If rates rise or reserves are heavy, distributable cash drops fast. That can delay owner draws even when the property is otherwise performing well.

5

Operating Expenses And Reserves

Operating Expenses And Reserves

Operating expenses decide how much rent turns into cash the owner can actually keep. In this model, variable expenses step down from 90% in Year 1 to 60% in Year 5, but fixed overhead stays at $30,300 per month and wages reach $660k per year from Year 3 onward, so the cash burden stays real even as the project matures.

Here’s the quick math: $30,300 x 12 = $363,600 in fixed overhead before wages. Add Year 3 wages and fixed cash costs rise to $1.024M a year, before utilities, maintenance, insurance, common area maintenance, leasing commissions, and capital reserves. Lean control lifts distributions; thin reserves can make near-term payouts look better while raising repair risk later.

Track Cash Burn And Reserve Coverage

Measure the full operating stack: property management fees, leasing commissions, utilities, maintenance, insurance, common area maintenance, payroll, and capital reserves. The key inputs are rent collected, expense ratio, fixed overhead, headcount, and reserve funding. If expenses fall faster than rent grows, owner draw improves; if reserves are light, a repair or tenant turnover can hit cash flow hard.

- Track monthly expense ratio by property

- Separate fixed and variable costs

- Fund reserves before distributions

- Watch payroll after Year 3

- Stress test vacancy and repairs

6

Compare low, base, and high owner-income cases

Owner income scenarios

Lease-up speed, vacancy, debt service, and reserves change owner income here. Early months are cash heavy, while stabilized years can turn positive after Month 26 breakeven.

| Scenario | Low CaseDownside case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | Slow lease-up and higher debt service keep owner draws near zero. | Modeled leasing and financing reach breakeven by Month 26, then owner income improves after stabilization. | Stronger rents, faster occupancy, and lighter financing costs lift owner income sooner. |

| Typical setup | Revenue lags plan, vacancy stays high, costs run over budget, reserves get used, and owner income stays near zero. | Revenue reaches breakeven by Month 26, cash trough hits around Month 36, EBITDA reaches $5.282M in Year 3, $10.192M in Year 4, and $9.434M in Year 5, but debt service and reserves still delay distributions. | Revenue runs above the base case, occupancy fills faster, margins widen, debt service is lighter, and reserves rebuild sooner. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Near-zero owner drawNear-zero draw | Delayed but positive distributionsModeled draw path | Larger stabilized distributionsFaster cash-out |

| Best fit | Use this to stress-test weak leasing, tougher lender terms, and a sponsor who can fund a longer burn. | Use this as the core plan for an operator who can carry the Month 36 cash trough and wait for Year 3 EBITDA. | Use this to test a stronger market, tighter cost control, and an operator who can keep the project full and financed well. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Mixed-Use Development Porter's Five Forces Analysis

- Mixed-Use Development BCG Matrix

- Mixed-Use Development Business Model Canvas

- Tracking Key Financial KPIs for Mixed-Use Development Projects

- Mixed-Use Development Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Profitability in Mixed-Use Development Projects

- How Much Does It Cost To Run A Mixed-Use Development Monthly?

- Mixed-Use Development Startup Costs: $160M+ Planning Budget

- Mixed-Use Financial Model Template in Excel

- How To Open A Mixed-Use Development In 24–48+ Months

- How to Write a Mixed-Use Development Business Plan

- Mixed-Use Development Marketing Mix

- Mixed-Use Development Marketing Plan

- Mixed-Use Development Business Proposal

- Mixed-Use Development PESTEL Analysis

- Mixed-Use Development Pitch Deck Example Editable PPTX

- Mixed-Use Development Business SWOT Analysis

- Mixed-Use Development Value Proposition Canvas

Frequently Asked Questions

The owner may make $0 during early development and receive distributions only after the project has cash available In this researched case, EBITDA is -$1811M in Year 1, -$4631M in Year 2, then positive at $5282M in Year 3 Actual take-home depends on debt service, reserves, taxes, and ownership share