Owner income$317k

Owner income$317kMobile Burger Stand Owner Income: $459k Year 1 Profit Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$317k  Net margin22.8%

Net margin22.8% Revenue for target pay$737k

Revenue for target pay$737k Business difficultyHard

Business difficultyHard

A mobile burger stand owner can make strong money on paper, but only if sales volume holds and cash isn’t drained by payroll, fixed costs, startup spend, or reserves Using the researched assumptions, Year 1 revenue is about $1083k per month, with 85% gross margin after food and packaging and $4585k annual operating profit before owner taxes and reserves The model also shows $377k in startup capex and a $630k minimum cash need by Month 4, so early owner take-home should be planned carefully

Owner income$317kNet margin22.8%Revenue for target pay$737kBusiness difficultyHardWhat could your burger stand pay you?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Mobile Burger Stand model?

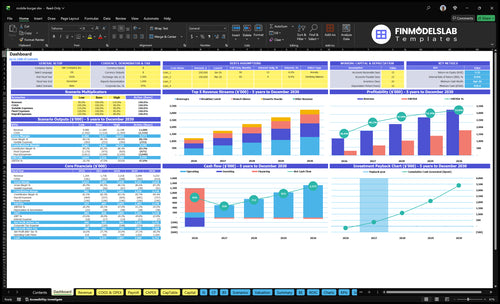

The Mobile Burger Stand Financial Model Template dashboard shows assumptions, revenue, margin, payroll, fixed costs, cash reserve planning, owner income, and break-even; it maps $1,083k Year 1 sales, 85% gross margin, $406k payroll, $1,625k fixed costs, $377k capex, and $630k minimum cash need. It’s a planning tool, not a payout promise.

Owner-income model highlights

- Owner income estimates

- Revenue and margin

- Scenarios and assumptions

What is the difference between mobile burger stand revenue vs profit?

Revenue is the total burger sales coming in; profit is what stays after food, packaging, marketing, payment fees, payroll, and fixed costs. For Mobile Burger Stand, the figures provided show $130M in Year 1 revenue, 15% for food and packaging, and 35% more for marketing and payment fees, which leaves $105.95M contribution. After $195k fixed expenses and $406k payroll, operating profit is $4.585M, and owner take-home can be lower once reserves, debt service, startup capex, and cash needs are covered.

Revenue

- Revenue = total sales.

- $130M is top line.

- Food and packaging take 15%.

- That leaves $110.5M gross profit.

Profit

- Marketing and fees take 35%.

- That leaves $105.95M contribution.

- Fixed costs are $195k.

- Payroll adds $406k; profit is $4.585M.

How does staffing change owner-operated burger food truck income?

Owner-operated shifts can protect cash in a Mobile Burger Stand, but this is not passive income: payroll is $406k in Year 1 and rises to $582k by Year 5 as staffing expands. That extra labor can lift weekly covers from 1,110 to 2,310, but it also lowers margin per sale and pushes break-even higher. The owner’s choice is simple: work more shifts to hold cash, or hire more staff to open longer and sell more.

Cash first

- $406k payroll in Year 1

- Owner shifts protect cash flow

- Less staff means tighter hours

- Not passive income

Growth tradeoff

- $582k payroll by Year 5

- 1,110 to 2,310 weekly covers

- Staff supports events and longer hours

- Higher break-even volume follows

How many burgers per day to make a mobile burger stand profitable?

A Mobile Burger Stand needs about 90 average orders per day to break even, and about 105 per day to support a $100k owner draw before reserves; for the core KPI, see What Is The Most Important Indicator Of Success For Your Mobile Burger Stand?. Year 1 models 1,110 weekly covers, or about 159 per day, so the issue is capacity, not demand math.

Break-even math

- $601k annual payroll plus fixed costs

- $22.52 blended average order value

- 81.5% contribution margin after variable costs

- 90 orders/day covers the cost base

Profit target

- 105 orders/day supports owner draw

- 159 orders/day modeled in Year 1

- Weekend spikes can lift weekly volume

- Prep, staffing, weather, and waste cap output

Want to see the main income drivers?

1

$1.1K-$2.3K/wkSales Volume

More covers per week lift revenue fast, and Year 1 scales from 1,110 weekly covers to 2,310 by Year 5.

2

$18.5/$28Ticket Size

A higher check size on midweek and weekend sales turns the same foot traffic into more gross profit.

3

28 vs 18.5Location Mix

Weekend and event-heavy stops pay better, so shifting mix toward those runs lifts take-home on the same route.

4

15%-13%Food Cost

Keeping ingredients and packaging near 15% protects contribution margin on every burger sold.

5

$406KLabor Load

Year 1 payroll is about $406K, so staffing discipline has a bigger effect on take-home than small price moves.

6

$16.3K/moFixed Overhead

Fixed costs set the break-even floor, and these expenses do not fall just because sales slow down.

Mobile Burger Stand Core Six Income Drivers

Sales volume

Sales Volume

Sales volume is the number of covers served each day and week. For a mobile burger stand, it drives the whole income line: Year 1 ranges from 100 Monday covers to 250 Saturday covers, or 1,110 weekly covers. By Year 5, that rises to 2,310 weekly covers. More covers mean more revenue, but only if line speed, prep, and staffing keep up.

The risk is lumpy traffic. Weather, lunch routes, breweries, festivals, and repeat stops decide whether sales are steady or choppy. Here’s the quick math: if weekly covers jump from 1,110 to 2,310, volume is up 108%. That can lift cash flow fast, but waste, stockouts, and overtime can eat the gain if demand is not forecasted stop by stop.

Track Covers by Stop

Measure covers by day, site, and event type, then compare them with prep used, labor hours, and waste. The useful inputs are headcount served, service window, weather, repeat visits, and whether the stop is a lunch route, brewery, or festival. One strong stop can hide a weak one, so track each location separately.

Improve volume by matching staffing and prep to the forecast. If a Friday brewery run beats a weekday lunch route, shift inventory and crew there. Keep a simple log of covers sold, stockouts, and waste; that shows where extra sales become profit and where growth just creates overtime and spoilage.

- Track covers by location

- Watch weather and event mix

- Match prep to demand

- Protect line speed at peak

- Cut waste after slow days

1

Average ticket

Average Ticket

Average ticket is what each guest spends per visit. For a mobile burger stand, Year 1 tickets are $18.50 midweek and $28 on weekends, rising to $21.50 and $34 by Year 5. Higher ticket lifts revenue per cover and gross margin, but only if combos, sides, drinks, and premium toppings don’t push up ingredient, packaging, and payment fees.

Here’s the quick math: at 1,110 weekly covers, every $1 of AOV adds $57,720 a year before costs. That only helps owner pay if the extra dollar stays profitable after food and card fees. One clean line: a bigger tab is good only when the margin follows it.

Raise ticket, protect margin

Track average ticket by daypart, event, and payment type. Measure burger, add-on, and drink mix, then test combo pricing before changing core menu prices. Watch whether premium items really add gross profit, or just create more packaging and card fees.

- Guest count by daypart

- Attach rate for combos

- Card share and fees

- Food and packaging cost

If ticket rises but prep gets slower, owner income can fall from waste, overtime, and longer lines. Keep the menu tight, price add-ons clearly, and forecast cash weekly so higher revenue turns into usable profit.

2

Location and event mix

Location and Event Mix

Where the truck parks drives both volume and owner take-home. Street service and office lunches are usually steadier, while breweries, late-night stops, festivals, and private events can push weekend tickets to $28 in Year 1 versus $1850 midweek in the model. The real question is not just sales, but which stop leaves the most cash after fees and labor.

Track covers, average ticket, vendor fees, extra staff hours, prep waste, and weather loss by stop type. High-grossing events can still cut profit if service runs longer, food sits longer, or a rainout kills volume. Use contribution per event, not gross sales, to judge whether a location adds income or just adds work.

Measure Profit by Stop Type

Build a simple log for each stop: date, venue, covers, ticket, fees, labor hours, and waste. Then compare gross sales with net cash per hour; that shows whether a lunch route, brewery, or festival really earns more. If one event needs more staff or longer prep for the same take-home, price it higher or skip it.

Set a minimum target before you book. Count vendor fees, extra payroll, and spoiled product in the forecast, and test the mix monthly. A stop that lifts revenue but lowers margin can still hurt the owner’s draw, especially when weather or slow line speed cuts turns.

3

Food, packaging, and waste

Food, packaging, and waste

This is the first margin gate. Ingredients at 14% of revenue plus packaging at 1% put total COGS at 15%, or about $195k at the modeled Year 1 scale. Here’s the quick math: every 1-point cost swing changes Year 1 profit by about $13k.

This driver includes buns, beef, toppings, sauces, cups, wrappers, and spoilage. The inputs are covers, menu mix, portion size, prep yield, and packaging choice. If portions drift or waste rises, gross margin drops first, and owner draw shrinks right after. One bad prep day can matter.

Measure and cut waste

Track food cost by item, not just in total. Watch purchase price, portion specs, spoilage, and throwaway count each day. If one ingredient runs hot, fix the recipe card, weigh key items, and reset prep counts before service. That keeps margin from leaking into cash flow.

Use a simple menu, standard scoops, and tight prep sheets. Test packaging that protects food without overbuying it. A 1-point cost drop is about $13k of Year 1 profit, so small controls can protect labor capacity, debt service, and the owner’s pay.

4

Labor model

Labor Mix Drives Owner Pay

The labor model is the split between owner shifts and paid cooks, cashiers, and support staff. In Year 1, payroll is $406k, rising to $582k by Year 5, so wages decide how much gross profit reaches owner take-home. If the owner works more shifts, paid labor falls, but that is earned labor, not passive profit.

Hiring more staff can extend lunch, dinner, and event coverage, but it also raises the break-even sales floor. More labor means more scheduling, training, and quality control, so revenue has to grow fast enough to cover each added hour. If covers do not rise with staffing, owner draw shrinks even when top-line sales look better.

Track Labor Per Cover

Measure labor cost per cover, labor as a percent of sales, and owner hours worked. Those three inputs show whether payroll is creating profit or just adding volume. A burger stand should staff to the rush, not to a fixed headcount, because slow shifts can turn paid labor into dead cost.

- Track sales per labor hour.

- Compare staffed hours to covers.

- Test owner shifts against payroll.

- Cut labor that does not lift throughput.

Use extra staff only when they lift line speed, event coverage, or order accuracy enough to pay for themselves. If a new cashier or cook does not increase output, the added payroll hits cash flow first and owner pay second.

<

/div>

5

Fixed operating costs

Fixed operating costs

Fixed operating costs are the monthly bills that hit even when sales are weak: rent, utilities, insurance, certification fees, POS subscription, accounting and legal, repairs, and cleaning. In this model they total about $16.25k per month, or $195k a year before payroll. That is the minimum cash base you must cover, so rainouts, slow weeks, and off-season gaps can cut owner pay fast.

Track the monthly burn

Measure fixed cost per open day and compare it with daily gross profit. If the stand opens 20 days a month, fixed overhead is about $812.50 per day before payroll. Keep a weekly cash view, and flag spikes in rent, repairs, and cleaning before they squeeze owner draw.

- $16.25k monthly fixed cost

- $195k annual overhead

- Rainouts still burn cash

6

Compare low, base, and mature owner income scenarios

Owner income scenarios

Owner income changes fast with traffic, ticket size, payroll, and fixed rent. The low case protects cash, while the high case shows what fuller demand does to draw capacity.

| Scenario | Low CaseCash-preserve case | Base CaseModel case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the thin-demand case where the stand reaches operating break-even but leaves no owner draw before reserves. | This is the modeled case where owner income follows the Year 1 plan and turns into positive EBITDA after launch. | This is the stronger-demand case where owner income rises as traffic and ticket size hold up through Year 5. |

| Typical setup | Volume sits near 90 orders a day, fixed rent and payroll stay high, and cash needs stay tight while the model gets to break-even. | Year 1 averages about 159 covers a day, with $406k payroll and $195k fixed costs, so draws depend on keeping traffic steady. | Year 5 reaches about 330 covers a day, with $582k payroll and $195k fixed costs, and EBITDA climbs to $1.776M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0Break-even guardrail | $317kYear 1 profit | $1.776MYear 5 upside |

| Best fit | Use this to test slow ramp and weak location traffic. | Use this for lender talks, staffing plans, and reserve sizing. | Use this to test the upper end of draw, hiring, and cash strain if demand stays strong. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Mobile Burger Stand Porter's Five Forces Analysis

- Mobile Burger Stand BCG Matrix

- Mobile Burger Stand Business Model Canvas

- 7 Critical KPIs for Your Mobile Burger Stand

- Mobile Burger Stand Business Plan Template in Pre-Written Word

- Increase Mobile Burger Stand Profitability: 7 Essential Strategies

- Running Costs: How Much Does It Cost To Operate A Mobile Burger Stand Monthly?

- Mobile Burger Stand Startup Costs: $630K Planning Need

- Mobile Burger Stand Financial Model Template in Excel

- How To Open A Mobile Burger Stand In 8 To 16 Weeks

- How to Write a Mobile Burger Stand Business Plan in 7 Steps

- Mobile Burger Stand Marketing Mix

- Mobile Burger Stand Marketing Plan

- Mobile Burger Stand Business Proposal

- Mobile Burger Stand PESTEL Analysis

- Mobile Burger Stand Pitch Deck Example Editable PPTX

- Mobile Burger Stand Business SWOT Analysis

- Mobile Burger Stand Value Proposition Canvas

Frequently Asked Questions

The model shows $4585k in Year 1 operating profit before personal taxes, reserves, debt service, and owner draw decisions That comes from $130M in revenue, 85% gross margin after food and packaging, $195k in fixed costs, and $406k in payroll It is a planning case, not guaranteed take-home pay