Owner incomeY1 ≈$5.3M

Owner incomeY1 ≈$5.3MHow Much Does A Money Transfer Service Owner Make? $136M Pre-Overhead

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeY1 ≈$5.3M  Net margin88%→92%

Net margin88%→92% Revenue for target payY1 ≈$6.1M

Revenue for target payY1 ≈$6.1M Business difficultyHard

Business difficultyHard

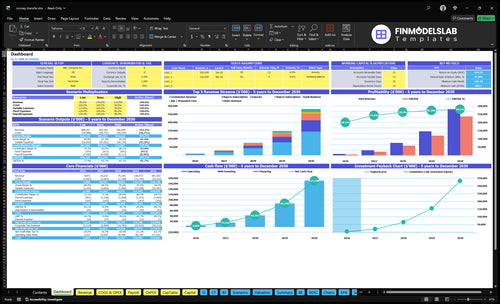

You’re not paid from transfer volume alone you’re paid from what’s left after processing, cloud security, marketing, compliance, fraud reserves, staffing, and reinvestment In the provided five-year planning assumptions, Year 1 shows about $234M in transfer commission revenue and about $136M before unprovided fixed overhead and owner distributions

Owner incomeY1 ≈$5.3MNet margin88%→92%Revenue for target payY1 ≈$6.1MBusiness difficultyHardWhat would your owner pay be?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to pressure-test owner pay in the model?

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions—open the Money Transfer Service Financial Model Template to test dashboard, income statement, cash flow, assumptions, scenarios, and owner-pay outputs. Year 1 charts show $234M transfer revenue, 88% gross margin after COGS, and about $136M pre-overhead contribution versus later-year cases.

Owner-income model highlights

- Owner pay after reserves

- 88% gross margin after COGS

- Scenario tabs change pay

How much profit can a money transfer service make?

A Money Transfer Service can show large accounting profit, but revenue is not owner take-home. In the Year 1 plan, 72,167 transfers at $3,245 revenue per transfer create about $234M in transfer commission revenue; track the growth side with What Is The Current Growth Rate Of Your Money Transfer Service? because profit depends on cost control, fraud losses, compliance, taxes, reinvestment, and payout policy.

Year 1 profit view

- 72,167 planned transfers

- $3,245 revenue per transfer

- $234M transfer commission revenue

- $136M before unprovided fixed costs

Year 5 upside

- 153M planned transfers

- $5,550 revenue per transfer

- $8,515M revenue before fixed costs

- 12% COGS plus $700K acquisition marketing

How do storefront, agent, and digital money transfer models affect income?

The Money Transfer Service model pays best when it moves more completed, compliant transfers with the lightest possible cost base. A storefront can build local trust, but rent, staffing, cash handling, and local marketing lift owner costs, while an agent model expands reach but cuts gross margin through agent commissions and payout partner fees. The digital-first path has the strongest income scale in the assumptions, rising from 6,014 monthly transfers in Year 1 to 127,847 in Year 5, but it needs more spend on software, security, acquisition, compliance workflows, and fraud controls.

Storefront and agent income

- Storefront builds trust fast.

- Rent and staffing raise fixed costs.

- Cash handling adds risk and work.

- Agent reach costs margin per transfer.

Digital-first income

- 6,014 transfers in Year 1.

- 127,847 transfers in Year 5.

- Software and security must scale.

- Fraud and compliance controls protect income.

How many transfers are needed to pay the owner?

For Money Transfer Service, the transfer count to pay the owner is (fixed overhead + target owner pay) / net contribution per transfer. With Year 1 gross revenue per transfer of $3,245 and 12% COGS, net is about $2,856 before fixed overhead, so $10,000 of monthly overhead needs about 350 transfers. There is no single break-even number, because compliance, fraud reserves, payroll, rent, software, marketing, and reinvestment all move the math.

Quick math

- Formula: overhead plus owner pay, divided by net

- Gross per transfer: $3,245

- 12% COGS: about $389

- Net per transfer: about $2,856

What moves the count

- $10,000 overhead needs about 350 transfers

- Compliance costs can lift the target

- Fraud reserves reduce owner pay room

- Rent, software, and payroll matter too

Want to see the six income levers?

1

72K-153MTransfer Volume

Marketing rises from $700K in Year 1 to $5M in Year 5, pushing transfers from 72,167 to 153M; more repeat use means more take-home.

2

$3.2K-$5.6KFee Spread

A wider fee and foreign exchange (FX) spread lifts revenue per transfer from about $3.2K to $5.6K, so pricing changes compound fast as volume grows.

3

$200-$12KCustomer Mix

A bigger share of small business and corporate senders lifts average order value (AOV) from $200 to $12K and adds subscription revenue, while individual-heavy traffic lowers take-home.

4

88%-92%Payout Costs

Payout partner fees and processing costs keep gross margin in the 88% to 92% range after direct costs, so every cut flows to owner cash.

5

2.0%-1.5%Compliance Cost

Fraud and risk spend runs from 2.0% to 1.5%, and tighter controls stop losses from eating the spread on high-value transfers.

6

3-4moOperating Leverage

Fixed overhead and reserves decide what the owner keeps, and the model still reaches breakeven by Month 3 with payback in 4 months.

Money Transfer Service Core Six Income Drivers

Transaction Volume And Repeat Usage

Completed Transfers and Repeat Usage

Completed compliant transfers drive income here, not signups alone. In Year 1, the model supports about 33,333 buyers and 72,167 transfers, or roughly 6,014 per month. More repeat use spreads compliance, software, rent, and staffing across more transactions, so gross margin improves and there is more room for owner pay.

The key inputs are buyer count, transfers per buyer, and segment mix. Repeat rates rise from 250 to 350 for individuals, 150 to 200 for small businesses, and 80 to 120 for corporate buyers. If repeat use stalls, fixed costs stay heavy and cash flow stays thin.

Track Repeat Transfers by Segment

Measure completed transfers, not just accounts created. Split the forecast by segment and watch transfers per buyer, because that is what turns acquisition spend into revenue. The plan’s Year 5 scale, at 583,333 buyers and about 127,847 transfers per month, only works if customers keep sending again and again.

- Track completed transfers weekly.

- Split repeat rate by segment.

- Watch failed and blocked transfers.

- Forecast cost per transfer monthly.

1

Fee And FX Spread Economics

Fee and FX Spread Economics

This driver is the blended take from each completed transfer: the fixed fee, the percentage fee, and the FX spread. With a $2 fixed fee + 3% in Year 1, a $1,015 average transfer produces about $32.45 of revenue; at $3 fixed + 2% and $2,625 in Year 5, it rises to $55.50.

After 12% COGS in Year 1 and 8% COGS in Year 5, contribution per transfer is about $28.56 and $51.06. That directly changes owner pay because every extra transfer adds cash before fixed overhead, but pricing power is limited by competition and compliance rules, so hidden fees can backfire fast.

Track Blended Fee Take

Track transfer count, average transfer value, fixed fee, percentage fee, FX spread, and COGS on every corridor. Here’s the quick math: if order size rises, the percent fee does more of the work; if mix shifts to larger transfers, revenue per transfer climbs without the same rise in fixed cost.

Keep pricing clean and upfront. Test changes against volume, approval rates, and churn, because a higher sticker price can cut completed transfers and lower owner take-home income. The goal is steady contribution per transfer, not the biggest fee on paper.

2

Corridor Mix And Average Transfer Size

Corridor Mix and Transfer Size

Weighted AOV drives revenue quality here: it rises from $1,015 in Year 1 to $2,625 in Year 5, as corporate buyers grow from 5% to 15% and average corporate tickets sit at $10,000–$12,000. Bigger tickets lift commission dollars per transfer, but they also add payout, monitoring, and fraud-control work, so owner pay only improves if those variable costs stay below the extra fee revenue.

The mix matters as much as the size. Individuals start at 70% of buyers with $200 AOV, so a corridor heavy in small transfers can look busy but still generate weak contribution. Here’s the quick math: if higher-value corridors raise revenue faster than payout and support costs, gross profit expands; if not, cash flow gets tied up in more checks and exception handling.

Track Mix, Margin, and Exception Load

Measure AOV by corridor, buyer type, payout cost, fraud flags, and manual review time. Forecast owner income by segment, because a transfer book with more corporate traffic behaves very differently from one with mostly $200 consumer sends.

Test pricing and ops by cohort. Keep a dashboard for mix, margin per transfer, and exception rate; if larger transfers push more reviews or payout delays, the extra revenue can disappear fast. What this estimate hides is the real cost of handling high-value cases end to end.

3

Payout Partner, Agent, And Processing Costs

Payout and Processing Costs

Money transfer payouts, agent commissions, and card or network fees hit gross margin before owner pay. In the model, COGS (direct costs) are 12% in Year 1 and 8% in Year 5, so gross margin rises from 88% to 92%. That 4-point lift matters because every extra fee dollar comes out of cash available for payroll, reserves, and distributions.

Here’s the quick math: on $100 of revenue, direct cost drops from $12 to $8. What this hides is the extra cost from cash pickup networks, correspondent partners, and agents, which is not quantified here. If those fees rise, the business can still grow on paper but owner draws shrink in cash.

Track Fee Mix Before You Promise Draws

Measure cost by payout method, corridor, and funding type. Track transaction processing, cloud and security, agent commission, and partner fee as separate lines, then compare them to transfer count and average transfer size. If one corridor uses more cash pickup or card funding, its margin can lag the blended model even when revenue grows.

- Track fees per transfer.

- Separate card and cash costs.

- Test partner pricing monthly.

- Forecast owner pay after COGS.

Do not set distributions from gross revenue. Set them after modeled COGS and reserve needs, because a 1-point fee swing on large volume can erase a lot of take-home cash fast.

4

Compliance, Licensing, Fraud, And Risk Control

Compliance, Fraud, And Licensing Cost Load

This driver includes AML work, KYC checks, transaction monitoring, reporting support, audits, chargebacks, fraud reserves, and licensing support. On a money transfer platform, these costs sit above gross profit, so a strong transfer margin does not become owner income until this layer is funded. The provided model shows about $136M of Year 1 pre-overhead contribution, but that is not take-home pay yet.

What you need to track is simple: completed transfers, average transfer size, screening volume, fraud loss rate, chargeback volume, reserve balance, and license count. Here’s the quick math: more volume usually raises both fee revenue and control work, so a bigger top line can still leave less cash for the owner if fraud or review costs climb faster than expected.

Track The Cost Per Clean Transfer

Measure compliance and fraud cost per completed transfer, not just total spend. If transfer volume rises from 6,014 per month in Year 1 toward 127,847 per month in Year 5, the team, tools, and reserve policy must scale with it or margin gets squeezed. The model already shows processing and cloud security, but it does not include compliance payroll, legal support, fraud losses, or reserves.

- Track KYC pass and fail rates.

- Watch chargebacks and fraud losses.

- Separate reserve funding from profit.

- Test staffing against transfer growth.

One clean rule: if control costs rise faster than contribution, owner pay falls even when revenue grows. So forecast these costs before you promise distributions, and keep a cash buffer for audits, reporting, and sudden fraud spikes.

5

Operating Model Efficiency And Overhead Leverage

Overhead Leverage

This driver is the gap between fixed overhead and transaction growth. In a digital money transfer model, costs move away from rent and frontline labor toward software, security, support, paid acquisition, and compliance tools. With $700K in Year 1 acquisition marketing and $5M in Year 5, the key test is whether each added transfer absorbs more overhead or just adds more support cost.

Owner-run workflows can keep payroll low early, but they also cap scale and raise key-person risk. So more margin reaches the owner only until hiring, reserve funding, and control work catch up. If reserves do not grow with volume, one fraud spike, outage, or support surge can cut the owner’s draw fast.

Track Cost Per Transfer

Measure overhead per completed transfer, not just total spend. Split it into rent, payroll, software, support, compliance tooling, and paid acquisition. The goal is simple: tie each added dollar of fixed cost to more compliant transfers, so owner pay rises faster than headcount.

- Transfers per employee

- Support tickets per 1,000 transfers

- Reserve balance vs volume

Test a storefront-led setup against a digital-led setup. A physical shop brings rent and frontline labor; a digital model shifts spend into software and controls. If volume grows but payroll and support grow at the same pace, overhead leverage stays weak and the owner has less cash to pay themselves.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts fast in this model because transfer volume, fee mix, and acquisition spend move together. These scenarios show how Year 1, Year 3, and Year 5 assumptions change the payout path.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the lower earnings path with Year 1 assumptions and tighter scale. | This is the modeled earnings path using the Year 3 operating case. | This is the stronger earnings path with Year 5 scale and better unit economics. |

| Typical setup | About 72,167 transfers, $1,015 weighted AOV, about $3,245 revenue per transfer, 88% gross margin after COGS, and $700K acquisition marketing before fixed overhead and owner pay. | About 439,200 transfers, $1,772 weighted AOV, about $4,680 revenue per transfer, 90.5% gross margin after COGS, and $2.5M acquisition marketing before fixed overhead and owner pay. | About 153M transfers, $2,625 weighted AOV, about $5,550 revenue per transfer, 92% gross margin after COGS, and $5M acquisition marketing before fixed overhead and owner pay. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $136MLow income case | $1.61BBase income case | $7.33BHigh income case |

| Best fit | Use this to stress-test the model if transfer volume stays near Year 1 and marketing efficiency lags. | Use this as the core planning case for a Year 3 operating run with a more balanced mix. | Use this to test upside if volume scales fast and enterprise mix rises in Year 5. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Money Transfer Service Porter's Five Forces Analysis

- Money Transfer Service BCG Matrix

- Money Transfer Service Business Model Canvas

- 7 Essential KPIs to Monitor for Money Transfer Service Growth

- Money Transfer Service Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Money Transfer Service Profit Margins

- Estimating Monthly Running Costs for a Money Transfer Service

- Money Transfer Service Startup Costs: $147M First-Year Base

- Money Transfer Service Financial Model Template in Excel

- How To Open A Money Transfer Service In 6–18 Months

- How to Write a Money Transfer Service Business Plan: 7 Action Steps

- Money Transfer Service Marketing Mix

- Money Transfer Service Marketing Plan

- Money Transfer Service Business Proposal

- Money Transfer Service PESTEL Analysis

- Money Transfer Service Pitch Deck Example Editable PPTX

- Money Transfer Service Business SWOT Analysis

- Money Transfer Service Value Proposition Canvas

Frequently Asked Questions

The provided data supports contribution estimates, not a guaranteed owner salary Year 1 shows about $234M in transfer commission revenue, 88% gross margin after COGS, and about $136M left after $700K acquisition marketing Owner take-home comes after compliance, payroll, rent, fraud reserves, taxes, reinvestment, and debt service