Money Transfer Service Startup Costs: $147M First-Year Base

Key Takeaways

- Licensing and compliance costs start before launch.

- Technology spend includes salaries, software, hosting, and fees.

- Physical sites need rent, utilities, equipment, and controls.

- Banking delays and marketing need extra working capital.

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates startup CAPEX for capitalized assets only, across lean, base, and full rollout cases.

Exclusions apply This calculator covers capitalized startup assets only. It excludes licensing fees, legal fees, compliance payroll, SaaS subscriptions, bond premiums, marketing, settlement float, reserves, working capital, debt service, deposits, inventory, and other operating cash needs.

What should the Money Transfer Service model validate?

Model tab lists startup costs/CAPEX; open the Money Transfer Service Financial Model Template to validate timing, amounts, and depreciation/amortization.

Key validation inputs

- $610k Year 1 payroll

- $162.6k fixed overhead

- $700k marketing spend

- 12% processing/cloud COGS

- 8% marketing/fraud expense

How do you fund a money transfer business?

To fund a Money Transfer Service, raise against the Year 1 model, not just the idea: $500,000 for buyer marketing, $200,000 for seller marketing, plus compliance payroll, licensing rollout, and operating losses. Build projections for transaction volume, transfer size, fees, settlement timing, and cash reserves; keep reserves and float separate from expenses so the runway math stays clean.

Year 1 funding inputs

- $200 consumer average order value

- $1,500 small business average order value

- $10,000 corporate average order value

- $2 fixed commission per transfer

Cost and capital plan

- 300% variable commission in Year 1

- $500,000 buyer marketing budget

- $200,000 seller marketing budget

- Model compliance, licensing, and float separately

What hidden costs come with starting a money transfer service?

The biggest hidden cost in a Money Transfer Service is cash tied up in operations, not just launch spend. Working capital and reserves cover customer settlement float, reserve accounts, bank holds, chargebacks, failed transfers, fraud losses, compliance monitoring, and delayed settlement; for a quick benchmark, see How Much Does The Owner Of A Money Transfer Service Typically Make?. Settlement liquidity is not revenue, because customer funds move through the system before earned fees are recognized, and year 1 models should carry 100% transaction processing fees, 20% variable cloud and security, 20% fraud and risk management, plus $13,550 in monthly fixed overhead.

Liquidity costs

- Working capital funds settlement float

- Reserve accounts absorb transfer risk

- Bank holds slow cash access

- Volume delay needs extra cash

Year 1 drivers

- 100% transaction processing fees

- 20% cloud and security costs

- 20% fraud and risk management

- $13,550 monthly fixed overhead

How much money do you need to start a money transfer business?

You should plan on a documented $1,472,600 Year 1 operating base for a Money Transfer Service before CAPEX, licensing outcomes, reserves, and customer float; use What Is The Current Growth Rate Of Your Money Transfer Service? to pressure-test how fast that funding gets used. The hard anchors are $610,000 in Year 1 core payroll and $13,550 in monthly fixed overhead, before transaction volume risk.

Base funding anchors

- Plan from $1,472,600 Year 1 base

- Include $610,000 core payroll

- Carry $13,550 monthly fixed overhead

- Add CAPEX, reserves, float, licensing

Launch range drivers

- Go lean online-first for lower CAPEX

- Fund store equipment for one location

- Budget higher compliance for multi-state

- Model $2 fixed commission and 300% variable commission

Calculate Fuding Needs

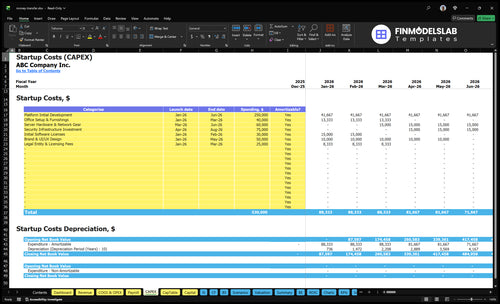

Startup cost summary

Startup cost summary for platform build, compliance, setup, and launch cash needs across low, base, and high scenarios.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Platform Initial Development | $250,000 | Core platform build, integrations, and testing | Yes |

| Security Infrastructure Investment | $75,000 | Security stack, controls, and reviews | Yes |

| Legal Entity & Licensing Fees | $25,000 | Licensing, legal filing, and compliance setup | Yes |

| Server Hardware & Network Gear | $60,000 | Servers, network gear, and setup | Yes |

| Office Setup & Furnishings | $40,000 | Office fit-out, furniture, and equipment | Yes |

| Operating Reserve and Working Capital | $685,000 | Payroll, overhead, and launch burn before breakeven | No |

Money Transfer Service Core Five Startup Costs

Regulatory Setup and Compliance Startup Expense

License Gate

Regulatory setup is a pre-opening cash cost, not CAPEX. Budget for state applications, legal counsel, AML and KYC policy design, compliance officer setup, audits, reporting tools, background checks, and a regulatory calendar. The model anchor is a $2,000 monthly legal and regulatory retainer from Month 1 to Month 60, or $120,000 total.

Cost Build

Use state count, filing fees, counsel hours, policy scope, and vendor quotes to price this line. Keep compliance-related payroll readiness separate from license and legal fees, so the startup budget stays clean. One line helps: if the state stack grows, this cost grows too. No state gives a guaranteed licensing outcome.

- Count each state filing

- Price outside counsel separately

- Book months of coverage

Control Spend

Keep the core program lean by reusing one policy set, one calendar, and one control framework across states, then customize only where rules force it. Start vendor quotes early for audit, screening, and reporting tools. The trap is hiring payroll too soon; that raises runway burn before the first approval lands.

- Reuse core policies

- Quote tools before signing

- Delay hires until needed

Approval Risk

What this estimate hides is timing risk. State-by-state review cycles can stretch launch dates, so cash must cover the $2,000 monthly retainer even if approvals take longer than planned. Build the budget for filings, not for certainty, because licensing can slip, change, or stall without warning.

Technology Platform and Transaction Infrastructure Startup Expense

Build Stack

This spend covers the app or web platform, transaction engine, customer onboarding, identity verification, fraud screening, API integrations, cybersecurity, hosting, data storage, monitoring, and SaaS tools. Split the budget into capitalized custom development and recurring software or processing costs. Here’s the quick math: core engineering payroll is $170,000 for the CTO and $140,000 for the lead engineer, before monthly tools and cloud.

Monthly Burn

Model recurring tech burn with $1,500 monthly software subscriptions and $2,500 base cloud hosting, then add 20% Year 1 variable cloud and security costs. Processing fees run 100% of revenue in Year 1, so the platform may show volume without net margin. Treat those fees as a pass-through line, not profit.

Lean Launch

Use off-the-shelf SaaS for onboarding, identity, and fraud first, then build only what changes unit economics or compliance. Defer custom extras until order volume proves demand. The big mistake is overbuilding the transaction stack before launch; that locks cash into code while subscriptions and hosting keep billing every month.

Runway Risk

What this estimate hides is timing. Custom development is front-loaded, but cloud, monitoring, and security start on day one, and revenue-linked processing fees can scale faster than software. If launch slips, burn rises without offsetting transactions, so the startup budget needs extra runway for pre-volume testing and integration delays.

Physical Location and Equipment Startup Expense

Location Base

A physical money transfer site starts with $5,000 monthly rent and $800 for utilities and internet from Month 1. Treat that as operating runway, not CAPEX. Add leasehold improvements, counters, and signage to the opening budget, then size cash needs by months of coverage.

Equipment List

Build the estimate from quotes for computers, receipt printers, scanners, security cameras, safes, network hardware, POS terminals, and customer-facing kiosks. Use units times vendor price, then add install and any leasehold work. Storefront and agent locations need more security and cash-handling controls than an online-only setup.

Lean Setup

Online-only operators can keep physical CAPEX much lower because they skip most buildout. If you need a storefront or agent site, standardize the layout and buy only the controls tied to real traffic and cash volume. The mistake is overbuilding before volume is clear.

Control Layer

A money transfer counter needs clear sightlines, safe storage, network uptime, and trained staff so cash and customer data stay protected. The physical layer should match transaction volume; if it doesn’t, rent, equipment, and support load rise fast.

Banking, Payment Rails, Bonding, and Reserves Startup Expense

Bank Setup

Bank onboarding and payment rails are launch costs, not assets. Budget for processor setup, ACH, card, and wire integration, plus correspondent relationships and testing. Use vendor quotes for onboarding fees, monthly minimums, and months of build time. If bank approval slips, the real cost is extra cash tied up in launch delay.

Cash Rules

Do not expense reserve or settlement deposits. They are balance sheet cash, along with customer float and required reserves. Separate them from burned cash like legal fees, screening tools, and integration work. For modeling, set transaction processing fees at 100% of Year 1 revenue, plus a $2 fixed commission per order and 300% variable commission.

Bond Cost

Money transmitter surety bond costs come as premiums or posted collateral, depending on the issuer. Model the bond amount, quote, term length, and any cash tied up. Treat collateral as restricted cash, not expense. State rules vary, so licensing timing and bond terms can change the opening cash need fast.

Working Capital

Bank delays raise working capital needs because you still pay vendors, staff, and setup costs before funds settle. Keep a separate settlement account and a reserve plan for chargebacks and holds. The faster the bank approves the rails, the less cash you need to bridge the first transfer cycle.

Staffing, Training, Insurance, and Launch Readiness Startup Expense

Launch Cash

Pre-opening cash should cover compliance officer readiness, customer support setup, cash-handling rules, employee training, insurance, launch marketing, and agent onboarding before revenue starts. With $610,000 in Year 1 core payroll, the monthly payroll run is about $50.8k ($610,000 / 12), so the first payroll buffer should be funded separately from the long runway.

Cost Build

The launch budget also needs $750 monthly business insurance and $1,000 monthly general administrative cost, or $21,000 over Year 1 before payroll. Marketing is the big swing: $500,000 for buyers at $15 CAC implies about 33,333 buyers, and $200,000 for sellers at $400 CAC implies 500 sellers.

Trim Burn

Keep pre-opening payroll separate from the operating runway, and do not mix it with post-launch headcount. The safest trim is phased hiring: train the compliance and support team first, then add sales and agent onboarding only when controls, scripts, and reporting are live.

Ready Check

One clean rule: fund launch readiness before growth spend. If insurance, admin, and training are not in place on day one, the platform can burn cash fast and still miss the launch gate.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Scenario size matters here because compliance, reserves, and launch spend stay heavy even when the physical footprint stays light. The main swing factors are state coverage, staffing, and acquisition.

| Scenario | Lean LaunchBest for pilot | Base LaunchBest for local launch | Full LaunchBest for funded rollout |

|---|---|---|---|

| Launch model | Digital-first launch with one state, a small team, and a light physical footprint. | Single-location or limited-state launch with a full core team and standard operating setup. | Multi-state rollout with more agents, more integrations, and a heavier launch team. |

| Typical setup | Keeps setup lean but still funds compliance, technology, banking, reserves, and customer acquisition. | Uses the model's first-year payroll anchor, fixed overhead, and launch marketing before CAPEX, licenses, and reserves. | Adds broader state coverage, larger onboarding, higher reserves, and more support and operations staff. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $500,000 - $900,000Pilot budget | $1,500,000 - $2,500,000Core launch | $3,000,000 - $5,000,000Rollout budget |

| Best fit | Best for founders testing a narrow market before adding locations or states. | Best for an operator funding a controlled launch with room for compliance and staffing. | Best for a funded team that wants to expand fast across multiple markets. |

Planning note: These scenario ranges are researched planning assumptions, not exact vendor, banking, or licensing quotes.

Related Products

- Money Transfer Service Porter's Five Forces Analysis

- Money Transfer Service BCG Matrix

- Money Transfer Service Business Model Canvas

- 7 Essential KPIs to Monitor for Money Transfer Service Growth

- Money Transfer Service Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Money Transfer Service Profit Margins

- Estimating Monthly Running Costs for a Money Transfer Service

- Money Transfer Service Financial Model Template in Excel

- How Much Does A Money Transfer Service Owner Make? $136M Pre-Overhead

- How To Open A Money Transfer Service In 6–18 Months

- How to Write a Money Transfer Service Business Plan: 7 Action Steps

- Money Transfer Service Marketing Mix

- Money Transfer Service Marketing Plan

- Money Transfer Service Business Proposal

- Money Transfer Service PESTEL Analysis

- Money Transfer Service Pitch Deck Example Editable PPTX

- Money Transfer Service Business SWOT Analysis

- Money Transfer Service Value Proposition Canvas

Frequently Asked Questions

In this model, the first-year baseline is $1,472,600 before CAPEX, licensing outcomes, reserves, settlement float, and operating losses That base includes $610,000 in core payroll, $162,600 in fixed overhead, and $700,000 in marketing Storefront equipment, state-by-state licensing, banking collateral, and platform build can materially change the final funding need