Owner income$180k/yr salary, $0 dist.

Owner income$180k/yr salary, $0 dist.How Much Office Development Owners Make In A 60-Month Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k/yr salary, $0 dist.  Net margin17%

Net margin17% Revenue for target pay$282k/mo

Revenue for target pay$282k/mo Business difficultyHard

Business difficultyHard

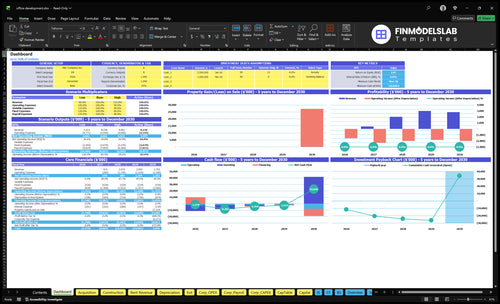

An office development owner should not plan on steady distributions under this model The researched assumptions show EBITDA, or operating profit before interest, taxes, depreciation, and amortization, ranging from -$1548M in Year 1 to -$2010M in Year 5 If the owner fills the Managing Director role, the model includes $180,000 in annual payroll compensation, but that is not the same as project profit The model’s payback lands in Month 60, with minimum cash of -$18801M in Month 59

Owner income$180k/yr salary, $0 dist.Net margin17%Revenue for target pay$282k/moBusiness difficultyHardWant to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will move with occupancy, margins, payroll, debt, reserves, and sale timing.

Want to see the Office Development model flow?

The Office Development Financial Model Template maps dashboard, assumptions, acquisition schedule, construction budget, leasing, payroll, costs, capex, financing, NOI, exit value, cash, and owner income. Open it.

Owner-income model highlights

- Owner income and cash flow

- EBITDA, NOI, exit value

- Breakeven Month 30 and payback Month 60

Why does office development owner income vary so much?

Office Development owner income swings because cash flow moves with occupancy, lease rates, lease-up speed, financing cost, construction delays, and exit valuation. Here’s the quick math: this model reaches breakeven in Month 30, but minimum cash is still -$18801M in Month 59, so owner pay can shift from salary-only to no payout. If leasing slips, debt costs rise, or sale proceeds miss plan, annual EBITDA stays negative from Year 1 through Year 5.

Income drivers

- Occupancy sets rent collected.

- Lease rates move revenue fast.

- Lease-up speed controls cash timing.

- Construction delays push income back.

Owner pay risk

- Breakeven lands in Month 30.

- Minimum cash hits -$18801M in Month 59.

- EBITDA stays negative Year 1-5.

- Exit value can erase payouts.

Which office development costs reduce owner profit most?

If you’re asking which Office Development costs hit owner profit the hardest, start with land and building buys: they use $120M in cash first, then construction adds $51M over 9 to 18 months. See How Much Does It Cost To Open Your Office Development Business? for the full cost stack. Every dollar spent before lease-up delays owner distributions and deepens the cash need.

Biggest cash drag

- Land and building purchases hit cash first.

- $120M is tied up across owned acquisitions.

- $51M more goes into construction budgets.

- 9 to 18 months means a long cash wait.

Ongoing profit pressure

- Active leased properties reach $56,000 monthly rent.

- Corporate fixed overhead still runs $44,500 per month.

- Payroll grows to $1,600M in Year 5.

- Lease-up timing shapes owner profit.

How many office projects are needed to make a living?

There isn’t a fixed project count that lets Office Development pay a living wage; the right target depends on pipeline size, equity share, fee %, overhead, and payout timing. In the base case, the model carries 7 projects, $120M in purchase costs, $51M in construction budgets, and $44,500 in monthly fixed overhead, so cash flow has to cover that before any owner draw. Managing Director pay is $180,000 per year, but owner distributions are not supported because EBITDA is negative in the base case.

Pay target

- 7 projects in the model

- $44,500 monthly overhead

- $180,000 MD pay

- No fixed living count

What drives payout

- $120M purchase costs

- $51M construction budgets

- Payroll rises from $708,000

- Base case has negative EBITDA

Want the six drivers that matter?

1

$282K/moLease Revenue

All seven assets can bring in about $282K a month in rent, so occupancy and rate mix drive owner cash fast.

2

Month 30Lease-Up Speed

Breakeven lands in Month 30, so faster lease-up cuts the cash drag before the Month 60 exit.

3

$5.1MBuild Budget

The $5.1M construction budget is the main margin gate, because overruns come straight out of equity.

4

$44.5K/moFixed Burn

Monthly overhead is $44.5K, so the business keeps burning cash until rent fills the pipeline.

5

-$18.8MFinancing Terms

Minimum cash falls to about -$18.8M, so debt mix and draw timing decide how much equity the owner must fund.

6

0.01%Exit Return

IRR is only 0.01%, so the Month 60 sale needs a better price or the deal stays thin.

Office Development Core Six Income Drivers

Lease revenue

Lease Revenue

Lease revenue is the rent collected after lease incentives. In this model, all seven projects active point to $282,000 in monthly rental fee potential, or $3.384 million a year before free rent, tenant allowances, and concessions. Net effective rent, not headline rent, is what drives NOI, owner distributions, and sale value.

Weak lease rates can still leave EBITDA negative after lease-up. So the owner’s take-home income depends on both price and lease quality, not just occupancy.

Price for Net Rent

Track headline rent, net effective rent, concessions, free rent, and tenant allowances on every deal. If $282,000 is the gross monthly target, any incentive package cuts actual cash collected and trims NOI. Stronger lease terms help monthly distributions and can raise exit value by locking in steadier cash flow.

- Price to net effective rent.

- Test incentives by tenant.

- Watch lease term and escalators.

1

Occupancy and lease-up

Lease-Up Speed

Occupancy and lease-up decide when projected rent becomes real cash. If space stays vacant, cash timing slips, lender confidence can soften, and owner distributions get delayed even when headline rents look strong.

This model does not give an occupancy rate, so you need to test vacancy, preleasing, absorption (how fast space fills), and stabilization (when occupancy settles). With annual EBITDA still negative, even a small delay can push the cash low beyond -$18,801M.

Track Vacancy and Absorption

Model lease-up by month, not just by year. Here’s the quick math: more vacant square feet means less rent collected now, more burn, and slower owner pay. Faster lease-up improves cash flow before the project reaches stabilization.

- Vacancy rate by month

- Preleased square feet

- Monthly absorption pace

- Stabilization date

- Signed leases versus available space

Use base, slow, and fast lease-up cases. If onboarding tenants takes longer than planned, distributions wait, and the owner may need more cash support before the building starts throwing off income.

2

Construction budget control

Construction Budget Control

When a project is still under construction, budget control is really cash control. With $51M in source construction budgets and project timelines of 9 to 18 months, overruns mean more equity has to go in before rent starts, which delays owner distributions and can shrink take-home after reserves and debt.

Here’s the quick math: that budget ties up about $2.8M to $5.7M per month before any lease income arrives. Track hard costs, soft costs, contingency, and build-out costs separately, or you can miss where margin is leaking and think the project is healthier than it is.

Track Cost Drift Weekly

Measure committed cost, paid cost, and remaining budget by bucket. That gives you an early warning when change orders or tenant build-outs start eating contingency, which is the point where owner cash gets squeezed.

- Hard costs by trade

- Soft costs by invoice

- Contingency used to date

- Build-out costs per tenant

If one line runs hot, fix scope fast, not after the draw request. That protects the cash reserve and keeps the project from needing extra owner money before stabilization.

3

Financing terms

Debt terms

Financing terms decide how much cash the owner actually keeps. Debt cost, leverage, interest reserve, loan-to-cost, and refinancing terms can turn a good lease-up into weak distributions if the asset is late, under-rented, or hard to refinance.

Here’s the quick math: higher leverage lowers upfront equity, but it raises interest drag and the cash cushion needed before rent stabilizes. The source case already shows minimum cash at -$18,801M, so debt structure is not a side issue; it can decide whether owners get paid at all.

Track the debt stack

Model the loan with four inputs: rate, LTC, interest reserve months, and refi date. Then test what happens if lease-up slips, value comes in low, or the new lender trims proceeds. If the reserve runs out before cash flow turns positive, owner pay stops even if the project looks fine on paper.

Use a worst-case cash plan, not the base case. One clean rule: if refinancing is needed to return capital, underwrite the exit as a financing event, not just a sale. That keeps distributions tied to real cash, not optimistic exit pricing.

- Track monthly interest burn.

- Set reserve to slow lease-up.

- Stress refinance proceeds.

4

Developer fee and sponsor economics

Developer Fees and Sponsor Economics

Developer fees, asset management fees, acquisition fees, disposition fees, and sponsor promote can pay the owner before rent is fully stabilized or a sale closes. In this model, those fee lines are not separately included, and the only explicit executive pay is the $180,000 annual Managing Director salary, or about $15,000 per month.

That matters because fee cash can support early payroll and overhead while lease-up is still weak. But if the fees are delayed, waived, or netted against project costs, the owner’s take-home income stays tied to rent and exit profit instead of current cash. The key risk is mixing company fee revenue with investor distributions and taxable owner income.

Track Fee Cash, Not Just Project Profit

Build a separate fee schedule for each deal and tie it to a trigger: closing, monthly management, stabilization, or sale. Track cash collected, not just accrued fees, so you can see whether fees can cover the $15,000 monthly salary and other overhead before NOI turns positive.

- Map each fee to a date.

- Separate sponsor promote from distributions.

- Reconcile fee revenue to bank cash.

If fees are paid at closing or monthly, they can smooth owner pay. If they depend on a later sale or hurdle, then the business needs enough working capital to carry the gap, and the owner should not count them as available cash until they hit the bank.

5

Exit valuation

Exit Valuation

Office sale value is the last big cash event, and it depends on NOI, the exit cap rate, buyer demand, financing markets, and lease quality. In plain English, the market pays more when the building has steady rent, strong tenants, and clean docs. If NOI slips or cap rates move up, the owner’s sale proceeds fall fast.

Here’s the quick math: value is usually NOI ÷ exit cap rate. The source model puts all sales in Month 60, and payback is also in Month 60, so the deal has little room for error. With IRR 001% and ROE 201 shown in the model, upside from sale is uncertain and usually comes later than operating income.

How to Protect Exit Value

Track the inputs that buyers actually price: in-place NOI, lease term left, tenant credit, rollover risk, and recent cap rate comps. If leases are short or weak, the exit cap rate usually gets worse and the owner keeps less cash at sale. That can also delay distributions if the building needs more time to stabilize.

- Model sale at multiple cap rates.

- Stress test Month 60 proceeds.

- Document leases and rent rolls.

- Watch lender pricing and buyer demand.

Do not treat the exit like guaranteed profit. A clean lease profile and stable NOI can support a stronger sale, but financing tightness or weak occupancy can cut value fast. If the exit is the main path to owner pay, build the forecast around a lower sale price too, not just the best case.

6

Compare low, base, and upside owner-income scenarios

Owner income scenarios

Lease timing and exit timing drive owner income here. The base case still shows negative EBITDA, so salary is the only modeled pay unless operations improve.

| Scenario | Low CaseDownside | Base CaseModel case | High CaseUpside |

|---|---|---|---|

| Launch model | Owner income stays at zero if lease-up or sale timing slips. | Owner income equals the Managing Director salary, with no modeled distributions. | Higher occupancy and faster lease-up can add distributions on top of salary. |

| Typical setup | Lease-up is late, sale timing moves out, and the owner may defer pay to protect cash. | The owner fills the Managing Director role at $180,000, while EBITDA stays negative each year, breakeven lands in Month 30, payback lands in Month 60, and minimum cash falls to -$18.801M. | Projects fill sooner, costs come in lower, financing is cleaner, and the exit uses a stronger cap rate. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0No payout | $180,000Salary only | Salary plus distributionsUpside path |

| Best fit | Use this to stress test slower occupancy and delayed exits. | Use this as the source case for budgeting and lender talks. | Use this to test the strongest realistic operating path without guessing. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Office Development Porter's Five Forces Analysis

- Office Development BCG Matrix

- Office Development Business Model Canvas

- 7 Critical KPIs for Office Development Success

- Office Development Business Plan Template in Pre-Written Word

- Increase Office Development Profitability: 7 Actionable Strategies

- How Much Does It Cost To Run Office Development Monthly?

- Office Development Startup Costs: Plan for $188M Funding Need

- Office Development Financial Model Template in Excel

- How to Open an Office Development Business: 12 to 36+ Month Launch Roadmap

- How to Write an Office Development Business Plan in 7 Steps

- Office Development Marketing Mix

- Office Development Marketing Plan

- Office Development Business Proposal

- Office Development PESTEL Analysis

- Office Development Pitch Deck Example Editable PPTX

- Office Development Business SWOT Analysis

- Office Development Value Proposition Canvas

Frequently Asked Questions

Under this model, the owner should plan for salary-only income unless the project outperforms The model includes a $180,000 Managing Director salary, but annual EBITDA is negative in every year, from -$1548M to -$2307M Payback lands in Month 60, so distributions are back-ended and not guaranteed