Owner incomeY1 $8.1M

Owner incomeY1 $8.1MPatient-Specific Implant Owner Income at $129M Year 1 Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeY1 $8.1M  Net margin62.7%

Net margin62.7% Revenue for target payY1 $12.9M

Revenue for target payY1 $12.9M Business difficultyHard

Business difficultyHard

You’re planning owner take-home in a regulated custom implant company, so the real question is how much cash survives after production, quality, sales, equipment, reserves, and reinvestment The provided five-year model shows $129M Year 1 revenue, 868% gross margin after listed direct and factory costs, and $18,500 monthly cleanroom lease cost This is income planning only, not clinical approval, reimbursement, tax, or device-specific compliance advice

Owner incomeY1 $8.1MNet margin62.7%Revenue for target payY1 $12.9MBusiness difficultyHardWant to test your own owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, labor, overhead, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

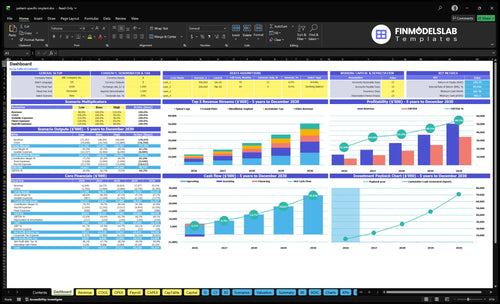

Need the full financial model view for Patient-Specific Implant Manufacturing?

This shows revenue, margin, costs, reserves, and owner take-home assumptions in the Patient-Specific Implant Manufacturing Financial Model Template. Open it.

Owner-income model highlights

- Owner take-home outputs

- Revenue by product

- Direct COGS and QC

- Test $1,289M / $5,054M

- Gross margin 868%-873%

- Scenario charts and runway

- Cleanroom lease burden

Is a patient-specific implant manufacturing business profitable?

Patient-Specific Implant Manufacturing can be profitable on the listed assumptions, with a Year 1 listed-cost profit pool of about $100M after direct costs, factory allocations, sales commissions, clinical support travel, and cleanroom lease scaling. But cash is not the same as accounting profit, so the model only scales cleanly when workflows, surgeon accounts, quality systems, and equipment use spread fixed costs over more units.

Profit drivers

- $100M Year 1 profit pool

- After direct and factory costs

- Includes sales and travel

- Scales with more units

Cash risks

- Slow onboarding hurts scale

- Rework raises cost fast

- Audits can eat staff time

- Receivables and reserves matter

How many patient-specific implant cases are needed to pay the owner?

For Patient-Specific Implant Manufacturing, owner pay starts with monthly approved units, not clinical demand promises. The Year 1 model shows 3,000 units, or 250 per month, at about $4,297 average revenue per unit, and listed gross profit is about $3,729 per unit after direct unit costs and 50% factory allocation. Here’s the quick math: the $18,500 monthly cleanroom lease alone needs about 5 units per month at that gross profit level, and full owner pay still has to cover payroll, QA, regulatory, debt, reserves, and target compensation.

Volume first

- 250 units monthly in Year 1

- $4,297 average revenue per unit

- $3,729 listed gross profit per unit

- Approved units drive owner pay

Cost stack

- $18,500 cleanroom lease monthly

- About 5 units cover lease

- Payroll and QA come next

- Regulatory, debt, reserves matter too

What profit margin can a patient-specific implant manufacturer make?

Using the provided assumptions, Patient-Specific Implant Manufacturing can show a gross margin of 868% in Year 1 and 873% in Year 5. That is before fixed overhead and reserves, which sit below COGS, so the real pressure point is direct unit cost. For the cost side, see What Are The Operating Costs Of Patient-Specific Implant Manufacturing?; direct costs run from $120 for surgical guides to $640 for cranial plates.

Direct cost base

- $120 to $640 per unit

- Materials and technician wages

- Post-processing and medical packaging

- Shipping and factory quality control

What moves margin

- 50% factory cost allocation is included

- Scrap and rework cut margin fast

- Machine time and inspection add cost

- Supplier pricing and product mix shift results

Want the six drivers behind owner income?

1

3K-11.6KCase Volume

More patient cases drive most of the revenue, with total units rising from 3,000 in Year 1 to 11,630 in Year 5.

2

$4.3KPricing Mix

The Year 1 blended selling price is about $4,297, and a bigger share of higher-priced implants lifts revenue per case.

3

$120-$640Unit Cost

Direct cost ranges from $120 for surgical guides to $640 for cranial plates, so scrap and yield hit margin fast.

4

3-15 FTEDesign Throughput

Faster review cycles and more cases per engineer let volume grow without payroll rising one-for-one.

5

5.0%+$6.7KQuality Overhead

Factory quality and sterilization add 5.0% of revenue, and ISO audit plus portal costs add $6.7K a month.

6

$981KCash Burden

The model needs a $981K minimum cash floor, plus an $18.5K monthly cleanroom lease, before taxes, approvals, or reimbursement lag.

Patient-Specific Implant Manufacturing Core Six Income Drivers

Approved Case Volume

Approved Case Volume

Approved case volume is the main profit lever here because fixed engineering, QA, regulatory, and equipment costs get spread over more shipped implants. The model grows from 3,000 units in Year 1 to 11,630 units in Year 5, or about 250 to 969 units per month. That lowers cleanroom lease burden from $74 per unit to about $19 per unit, which directly helps gross margin and owner pay.

What this estimate hides is the difference between pipeline interest and real approvals. If you count surgeon interest as demand before cases are approved and ready to build, you’ll overstate revenue and cash. Approved cases are the units that actually clear design, QA, and production gates, so they are the number that drives income you can trust.

Track Approved-to-Shipped Cases

Measure approved cases per month, approval rate, and the gap between pipeline and released jobs. Here’s the quick math: $18,500 monthly cleanroom rent divided by 250 units is $74 per unit, but at 969 units it falls to about $19. That spread is why volume matters more than just lead count.

Use a simple control: forecast only cases that have passed surgeon review, imaging checks, and internal release. That keeps staffing, material buys, and cash draws tied to real output, not hopeful demand.

1

Average Selling Price And Procedure Mix

Average Selling Price and Case Mix

Year 1 blended ASP is about $4,297, with prices ranging from $1,200 for surgical guides to $8,500 for cranial plates. Owner income rises when the mix shifts toward higher-value cases without a matching jump in labor, material, inspection, or documentation cost.

Here’s the quick math: more high-price cases lift revenue per unit, so gross profit and cash for owner pay can improve even if volume holds steady. What this estimate hides is mix risk; if hospital purchasing pushes more low-price guides, revenue per case drops fast.

Track Price by Procedure Mix

Measure units by procedure, ASP by product line, and direct cost per case each month. That lets you see whether revenue growth is coming from better mix or just more low-value work.

Keep pricing tied to contracting and hospital buying behavior, not unsupported reimbursement rates. If higher-value cases grow, test whether inspection, documentation, and setup time stay flat; if they do, owner draw improves faster than revenue alone would suggest.

- Track guide, plate, and implant mix.

- Watch ASP against direct cost.

- Stress-test lower-price case shifts.

2

Gross Margin And Direct Manufacturing Cost

Direct unit cost and factory overhead

For patient-specific implants, gross margin starts with the unit build. Direct costs are $640 cranial plates, $575 mandibular implants, $380 spinal cages, $595 acetabular cups, and $120 surgical guides, then a 50% revenue-based factory allocation adds quality control, indirect labor, maintenance, utilities, and sterilization validation. The owner only gets paid if selling price clears those costs with room left for overhead and tax.

The model lists 868% gross margin in Year 1, but scrap and rework can shrink that fast. One bad batch, a remake, or a sterilization delay turns a high-margin case into tied-up cash and lower draw capacity.

Track scrap before it eats cash

Measure gross margin by product line, not just blended. Track material, machine time, technician work, finishing, inspection, packaging, shipping, and sterilization coordination for each case, then compare them to the 50% factory allocation. If rework rises, margin drops twice: you pay again to remake the unit and you delay billing.

Keep a tight control set: unit scrap rate, rework hours, release delays, and cost per shipped implant. Here’s the quick test: if cost moves up and shipment timing slips, the owner’s cash draw falls even when booked revenue looks strong.

3

Design And Engineering Productivity

Engineering Hours per Approved Case

If each implant takes too many design hours, the team becomes the bottleneck, not the factory. Owner income improves when engineering hours per approved case fall, because labor cost per unit drops and the same staff can push more cases to release without extra hires.

Track hours by product, design revision count, review cycle time, and output per engineer. A 20% cut in hours per case can lift throughput about 25% if surgeon review, clinical approval, and quality documentation still happen. Unclear scans and rework can erase that gain fast.

Tighten Scan-to-Release Flow

Map the work from image intake to final release, and measure where cases wait. Faster imaging-to-design work lowers payroll per implant and helps cash flow, but only if the scan is complete enough to avoid redesigns. One clean rule: no case moves without a complete imaging file and a logged review step.

- Track hours per case by product

- Count revisions before approval

- Measure scan-to-review days

- Watch output per engineer monthly

- Flag poor imaging before release

If revision count rises, margin falls and work-in-process builds up. That ties up cash and delays owner pay, even when sales are strong. Use the data to spot which product line, reviewer, or file type is slowing the handoff.

4

Quality-System And Regulatory Overhead

Quality And Regulatory Overhead

For patient-specific implants, this overhead hits owner pay fast because documentation, validation, audits, complaint handling, supplier controls, and regulatory support are required, not optional. The factory allocation already includes 12% quality control, 15% indirect labor, 8% maintenance, 5% utilities, and 10% sterilization validation, or 50% before separate compliance spend.

Here’s the quick math: the more fixed and semi-fixed this cost stack is, the less it flexes with volume, so weak case flow pushes it straight into lower gross margin and smaller owner distributions. Track it per shipped case, not just as one monthly lump. If audit load, complaint volume, or supplier issues rise, cash gets tied up in overhead instead of take-home profit.

Track Compliance Cost Per Case

Measure compliance cost per approved case and split it into fixed and variable parts. Keep a simple monthly view for QA hours, validation runs, audit findings, complaints, and supplier reviews so you can see what scales with volume and what does not. One clean metric is better than a pile of reports.

Then test price and volume against that load. If case volume grows but compliance hours stay flat, owner income improves; if reviews, rework, or supplier resets climb, margin drops even when sales rise. The practical target is to keep quality work from growing faster than shipped cases, because that is where owner pay starts to leak.

5

Equipment, Working Capital, And Reserves

Equipment, Working Capital, And Reserves

When you add additive manufacturing or CNC payments, validation costs, inventory, supplier deposits, receivables, service contracts, and growth reserves, the business can show profit but still have little cash left for the owner. The cleanroom lease alone is $18,500 per month, or $222,000 per year, before equipment payments.

That gap matters most during ramp-up and capacity expansion. Here’s the quick math: accounting profit is not the same as cash available to distribute. If cash gets tied up in machines, stock, and patient-specific jobs in process, owner draws stay lower even when the income statement looks healthy. Profit does not pay the owner unless cash is free.

Track cash, not just profit

Build a monthly cash plan that separates operating profit from cash used for equipment, inventory, deposits, and reserves. Track equipment payments, validation spend, inventory on hand, receivables, and service contracts before setting owner pay. If receivables grow faster than shipments, distributions should slow.

- Set a reserve floor before owner draws.

- Forecast cash by month, not year.

- Match equipment buys to firm demand.

- Watch supplier deposits and validation timing.

For this model, the key test is simple: after the $18,500 lease and equipment obligations, how much cash is left after working capital needs? If that number is thin, owner income should stay conservative until volumes and collections are stable.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with unit volume, ASP, and how fast fixed cleanroom and compliance costs get spread. Stronger scale lifts EBITDA, but reserves and capex still shape what can be paid out.

| Scenario | Low CaseLow | Base CaseBase | High CaseHigh |

|---|---|---|---|

| Launch model | This case assumes slower monthly volume and tighter cash retention, so owner income stays editable. | This case uses Year 1 assumptions, with 250 units per month at a $4,297 ASP and an $8.1M EBITDA pool before unprovided items. | This case uses Year 5 scale, with 969 units per month at a $4,345 ASP and a $34.4M EBITDA pool before unprovided items. |

| Typical setup | The plant stays below Year 1 volume, so the fixed cleanroom lease, compliance audit, cloud portal, insurance, and admin costs take a bigger share of cash. | The model runs at 250 units per month, $12.89M revenue, 86.8% listed gross margin, and an $18,500 monthly cleanroom lease plus compliance and admin overhead. | The model runs at 969 units per month, $50.5M revenue, 87.3% listed gross margin, and the same fixed overhead spread across a much larger output base. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | EditableEditable low | $8.1MYear 1 base | $34.4MYear 5 scale |

| Best fit | Use this for a slow start, delayed referrals, or tighter reserve needs. | Use this as the core planning case for Year 1 operating assumptions. | Use this to test full-scale throughput and owner draw capacity. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Patient-Specific Implant Manufacturing Porter's Five Forces Analysis

- Patient-Specific Implant Manufacturing BCG Matrix

- Patient-Specific Implant Manufacturing Business Model Canvas

- What Are The 5 Core KPIs For Patient-Specific Implant Manufacturing Business?

- Patient-Specific Implant Manufacturing Business Plan Template in Pre-Written Word

- How Increase Patient-Specific Implant Manufacturing Profits?

- What Are The Operating Costs Of Patient-Specific Implant Manufacturing?

- Patient-Specific Implant Manufacturing Startup Costs With $49k Monthly Overhead

- Patient-Specific Implant Manufacturing Financial Model Template in Excel

- How to Open a Patient-Specific Implant Company in 12–24+ Months

- How To Write A Business Plan For Patient-Specific Implant Manufacturing?

- Patient-Specific Implant Manufacturing Marketing Mix

- Patient-Specific Implant Manufacturing Marketing Plan

- Patient-Specific Implant Manufacturing Business Proposal

- Patient-Specific Implant Manufacturing PESTEL Analysis

- Patient-Specific Implant Manufacturing Pitch Deck Example Editable PPTX

- Patient-Specific Implant Manufacturing Business SWOT Analysis

- Patient-Specific Implant Manufacturing Value Proposition Canvas

Frequently Asked Questions

The provided data does not give a final owner take-home number It supports a listed-cost profit pool of about $100M in Year 1 from $1289M revenue and about $411M in Year 5 from $5054M revenue Actual take-home comes after payroll, debt service, taxes, reserves, reinvestment, and approved owner distributions