Owner income$307K

Owner income$307KHow Much Probate Assistance Owners Can Make: $307K Year 2 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$307K  Net margin24.4%

Net margin24.4% Revenue for target pay$1.26M

Revenue for target pay$1.26M Business difficultyHard

Business difficultyHard

You’re modeling owner pay from case work, not a guaranteed salary or attorney-fee income The researched model shows $603K revenue in Year 1, $1259M in Year 2, and $307K EBITDA in Year 2, with breakeven in Month 8 This covers revenue, costs, reserves, and owner take-home planning, not legal advice, tax advice, or estate outcome promises

Owner income$307KNet margin24.4%Revenue for target pay$1.26MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

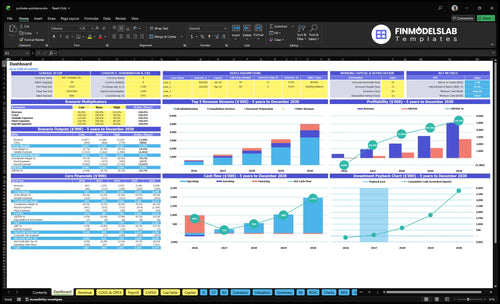

How do you check owner income in the financial model?

This screenshot in the Probate Assistance Service Financial Model Template shows revenue, margin, costs, reserves, and owner pay—open it.

Owner-income model highlights

- Year 1 revenue: $603K

- Year 2 EBITDA: $307K

- Cash, breakeven, payback

- Low/base/high cases

What affects probate assistance business profit margin?

Profit margin in a Probate Assistance Service is mostly set by case costs, referral and portal fees, payroll, and fixed overhead; in Year 1, direct COGS is 10% of revenue, variable referral and portal costs add 13%, and fixed overhead is $7,950 per month. If you want the KPI lens, see What Are The 5 Key KPIs For Probate Assistance Service?—and keep reimbursed client costs separate from business expenses, because owner take-home only comes after reserves and taxes.

Biggest drivers

- 10% direct COGS hits every case.

- 13% more goes to referral and portal costs.

- Payroll is $347K in Year 1.

- Payroll rises to $447K in Year 2.

Margin watchouts

- EBITDA margin is -128% in Year 1.

- It moves to 244% in Year 2.

- It reaches 542% in Year 5.

- Reimbursed client costs are not profit.

How many probate clients do I need to make a living?

If you want to make a living with Probate Assistance Service, plan on about 1,111 matters a year, or 93 matters a month, using a weighted fee of about $1,133 per matter. The math is simple: target monthly profit ÷ contribution per matter = required matters, and that contribution has to cover direct costs, referrals, portal costs, payroll, and overhead.

Volume math

- $1,133 weighted fee per matter

- 1,111 matters per year

- 93 matters per month

- Use profit target ÷ contribution per matter

Capacity check

- More full administration raises fees

- It also raises hours per matter

- Contribution must cover all direct costs

- Case volume is planning, not guaranteed demand

How much can I make owning a probate assistance service?

If you're asking How Do I Start A Probate Assistance Service Business?, the researched staffed model shows owner profit is negative in Year 1 at -$77K EBITDA, then about $307K in Year 2 and $783K in Year 3 before taxes, reserves, debt service, and distributions. This is not legal-fee income; it depends on paid matters, pricing, and capacity.

Profit path

- Year 1 EBITDA: -$77K

- Year 2 EBITDA: $307K

- Year 3 EBITDA: $783K

- Revenue grows: $603K to $2.070M

Staffed model

- Year 1 payroll: $347K

- Year 2 payroll: $447K

- Owner income needs paid matters

- Capacity sets the real ceiling

Want to see the six income drivers?

1

$603K-$5.0MPaid case volume

More paid probate cases drive most of the jump from $603K in Year 1 to $5.0M in Year 5, and that is what flips EBITDA from -$77K to $2.716M.

2

$195-$300/hrFee mix

The shift toward full administration, plus rates moving from $195 to $300 per hour, lifts revenue per file and protects margin.

3

4.5-5.5 hrsCase hours

Billable time per active customer rises from 4.5 to 5.5 hours a month, so each case bills more, but slower files also stretch cash.

4

4.5-13.5 FTEStaff leverage

FTE scale rises from 4.5 to 13.5, so the winner is staffing that grows slower than case load and keeps wages from eating profit.

5

$350-$450Referral CAC

CAC drops from $450 to $350 while marketing spend climbs from $45K to $140K, so better referral conversion buys growth without burning as much cash.

6

$95K+$767KOverhead reserve

Fixed overhead runs about $95K a year, and the cash trough hits $767K in Month 8, so reserve control decides whether early growth protects owner take-home.

Probate Assistance Service Core Six Income Drivers

Qualified Probate Case Volume

Qualified Probate Case Volume

This driver is the count of paid, completed matters, not raw inquiries. At about 50 matters/month in Year 1, rising to 93 in Year 2 and 250 in Year 5, volume is the biggest revenue swing when capacity exists. More cases spread the $7,950/month fixed overhead and can lift EBITDA, which is what funds owner pay.

It includes executor intake, document collection, and status coordination. The catch is simple: if screening is weak, follow-up time and CAC rise, and inquiries do not count until they become paid matters. More lead flow without qualification just burns staff time.

Track Paid Matters, Not Leads

Measure inquiry-to-paid conversion, paid matters per month, and follow-up hours per case. Use the formula paid matters × weighted fee—the blended average across service types—to test whether volume can cover fixed overhead before hiring or spending more on marketing. If the team cannot absorb the jump from 50 to 93 to 250 matters, margin will slip even if revenue grows.

- Track paid matters by source.

- Cap unpaid intake follow-up.

- Cut weak-fit cases fast.

1

Average Fee And Package Mix

Average Fee And Package Mix

Average fee and package mix set revenue per matter. In Year 1, the mix is 45% full administration, 30% consultation, and 25% document preparation, which produces a weighted fee of about $1,005. By Year 5, that weighted fee rises to about $1,670, so each matter brings in $665 more before any cost change.

That helps owner income only if price rises faster than labor time. Higher-value coordination usually takes more hours and tighter scope, so margin can shrink if the team spends more time on each case. One clean rule: the fee increase has to cover staff time, overhead, and still leave profit for the owner.

Price the mix, then protect the hours

Track package count, average fee, and hours per matter. Also watch how many cases move into full administration versus lower-fee consultation. If the mix shifts toward higher-value work and hours stay controlled, take-home income improves; if hours rise faster than price, the extra revenue gets eaten by labor.

- Track fee by package type.

- Measure hours per matter.

- Flag scope creep fast.

- Forecast monthly mix changes.

The key inputs are package mix, price per package, staff hours, and fixed overhead. The main swing here is the move from $1,005 to $1,670 weighted fee, not just more cases. That is the part that can lift profit and owner pay even when volume stays flat.

2

Case Complexity And Cycle Time

Case Complexity And Cycle Time

More complex estates can raise revenue, but they also push labor, follow-up, and cash timing in the wrong direction. A full administration case grows from 80 hours in Year 1 to 95 hours in Year 5, consultation from 20 to 30, and document prep from 35 to 45. That is higher billable value only if fees rise faster than time.

What this hides: unclear scope creates unpaid coordination, and longer cycle time delays cash. If a matter sits open longer, the team can handle fewer active cases per staff member, so owner pay depends on tighter workflow, cleaner handoffs, and faster completion.

Track Hours And Close Time

Measure hours per matter, days to completion, and open matters per staff member. Here’s the quick math: a case that moves from 80 to 95 hours is a 19% jump in labor before any fee increase, and consultation time rising from 20 to 30 hours is a 50% jump. If those hours are unpaid or delayed, margin and cash both slip.

- Set scope before work starts.

- Price for follow-up, not hope.

- Cap open cases per team member.

- Review stalled matters weekly.

Cleaner workflow protects capacity and cash, which is what lets the owner take money out without starving the operation.

3

Staffing Leverage And Delegation

Staffing Leverage

Delegation can lift case capacity, but payroll has to be matched to paid matters. Source payroll runs $347K in Year 1, $447K in Year 2, and about $1004M in Year 5 across a licensed legal lead, senior paralegal, case manager, intake coordinator, and administrative assistant. If hiring comes before volume, revenue lags payroll and owner pay gets squeezed.

The key is to separate owner replacement labor from direct case labor and fixed overhead. If a role does not speed a paid probate matter or protect compliance, it should stay off the payroll. When staffing is tied to clear service boundaries, labor turns into margin instead of a Year 1 EBITDA loss.

Track Utilization Before You Hire

Measure utilization as how fully each role is used on paid work, not just busy work. Track paid matters per staff member, hours per matter, days to completion, and unpaid follow-up time. Here’s the quick math: if payroll rises before load builds, operating profit drops even when inquiries look strong.

- Track paid matters, not inquiries.

- Cap each role’s job scope.

- Freeze hiring if utilization slips.

Use a simple handoff chain: intake qualifies, case manager coordinates, paralegal executes, and the legal lead reviews. That keeps work from sliding back to the owner. Staffing helps when cycle time falls and service boundaries hold; if a role stays underused for several months, delay the next hire.

4

Referral Conversion And Acquisition Cost

Referral Conversion and CAC

When referral conversion improves, more inquiries turn into paid matters, so each case carries more contribution after acquisition costs. Here the inputs are marketing spend, CAC (customer acquisition cost), referral commission rate, lead-to-paid conversion, and intake time. Marketing budget rises from $45K in Year 1 to $140K in Year 5, while CAC falls from $450 to $ 350.

That matters because referral partner commissions also drop from 10% to 8% of revenue. If paid leads are screened well, the owner wastes less intake time and keeps more EBITDA. If screening is weak, low-fit leads can eat staff time fast, so take-home income slips even when top-line volume looks fine.

Track Paid Matters, Not Just Leads

Here’s the quick math: CAC = marketing spend / paid matters. So the owner should track paid cases by source, referral commission paid, and intake minutes per lead. A compliant professional referral or trusted community channel is only good if it closes into a billable matter at a lower cost than other sources.

- Count paid matters by channel.

- Measure screen-to-close conversion.

- Watch intake time per bad lead.

- Review commission rate monthly.

What this hides: if conversion rises but case quality falls, support hours can spike and erase the savings. So the goal is not just more leads. It’s better-fit leads that convert into paid work with less follow-up, lower CAC, and cleaner margin for owner pay.

5

Overhead, Compliance, And Reserves

Overhead, Compliance, And Reserves

This driver is the cash you must keep in the business before owner pay. Fixed overhead is $7,950/month from rent, insurance, utilities, legal/accounting, IT, and marketing tools. Add $75,500 in early setup capex, and the planning cash need reaches $767K in Month 8. So even with positive EBITDA, distributable owner cash can stay tight.

Protect Cash Before Taking Draws

Track overhead, compliance spend, and reserve balance as separate lines. A clean rule: EBITDA is not spendable cash. Use a reserve floor that covers fixed costs and timing gaps, then pause owner draws if cash dips below that floor. That keeps payroll, filings, and client service funded during slower months.

- Track each fixed cost monthly.

- Review reserve balance weekly.

- Block owner draws below floor.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income changes fast here because case volume, staffing, and acquisition cost move together. The low case shows ramp-up risk, and the high case shows what a mature, staffed practice can support.

| Scenario | Lean CaseRamp-up risk | Base CaseStaffed growth | High CaseMature scale |

|---|---|---|---|

| Launch model | The lean case assumes a slow start, so owner income stays under pressure in Year 1. | The base case assumes a normal growth path, with income turning positive once the team is fully working. | The high case assumes a strong scale-up, with owner income rising as volume and staffing expand. |

| Typical setup | Year 1 revenue is about $603K, EBITDA is -$77K, volume is about 50 matters per month, direct COGS run near 10%, variable costs near 13%, and payroll is about $347K. | Year 2 revenue reaches about $1.259M, EBITDA is $307K, volume is about 93 matters per month, CAC is $425, and payroll is about $447K. | Year 5 revenue reaches about $5.008M, EBITDA is $2.716M, volume is about 250 matters per month, CAC falls to $350, and payroll is about $1.004M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$77KRamp-up risk | $307KBase case | $2.7MMature scale |

| Best fit | Use this to stress-test the opening ramp and cash burn before volume stabilizes. | Use this as the mid-case for planning hiring, ads, and cash needs. | Use this to test upside if the firm builds a larger, staffed practice and keeps acquisition costs down. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Probate Assistance Service Porter's Five Forces Analysis

- Probate Assistance Service BCG Matrix

- Probate Assistance Service Business Model Canvas

- What Are The 5 Key KPIs For Probate Assistance Service?

- Probate Assistance Service Business Plan Template in Pre-Written Word

- How Increase Probate Assistance Service Profits?

- What Are Operating Costs For Probate Assistance Service?

- Probate Assistance Service Startup Costs: $767K Cash Need

- Probate Assistance Service Financial Model Template in Excel

- How To Open A Probate Assistance Service In 6 To 12 Weeks

- How To Write A Business Plan For Probate Assistance Service?

- Probate Assistance Service Marketing Mix

- Probate Assistance Service Marketing Plan

- Probate Assistance Service Business Proposal

- Probate Assistance Service PESTEL Analysis

- Probate Assistance Service Pitch Deck Example Editable PPTX

- Probate Assistance Service Business SWOT Analysis

- Probate Assistance Service Value Proposition Canvas

Frequently Asked Questions

The researched model shows $603K in Year 1 revenue, $1259M in Year 2, and $5008M in Year 5 That is revenue, not owner pay Owner take-home depends on payroll, direct case costs, marketing, reserves, taxes, and whether cash is reinvested for growth